Outerwear manufacturer Columbia Sportswear (NASDAQ: COLM) reported Q1 CY2026 results topping the market’s revenue expectations, but sales were flat year on year at $779 million. The company expects next quarter’s revenue to be around $605 million, close to analysts’ estimates. Its GAAP profit of $0.65 per share was 85.2% above analysts’ consensus estimates.

Is now the time to buy Columbia Sportswear? Find out by accessing our full research report, it’s free.

Columbia Sportswear (COLM) Q1 CY2026 Highlights:

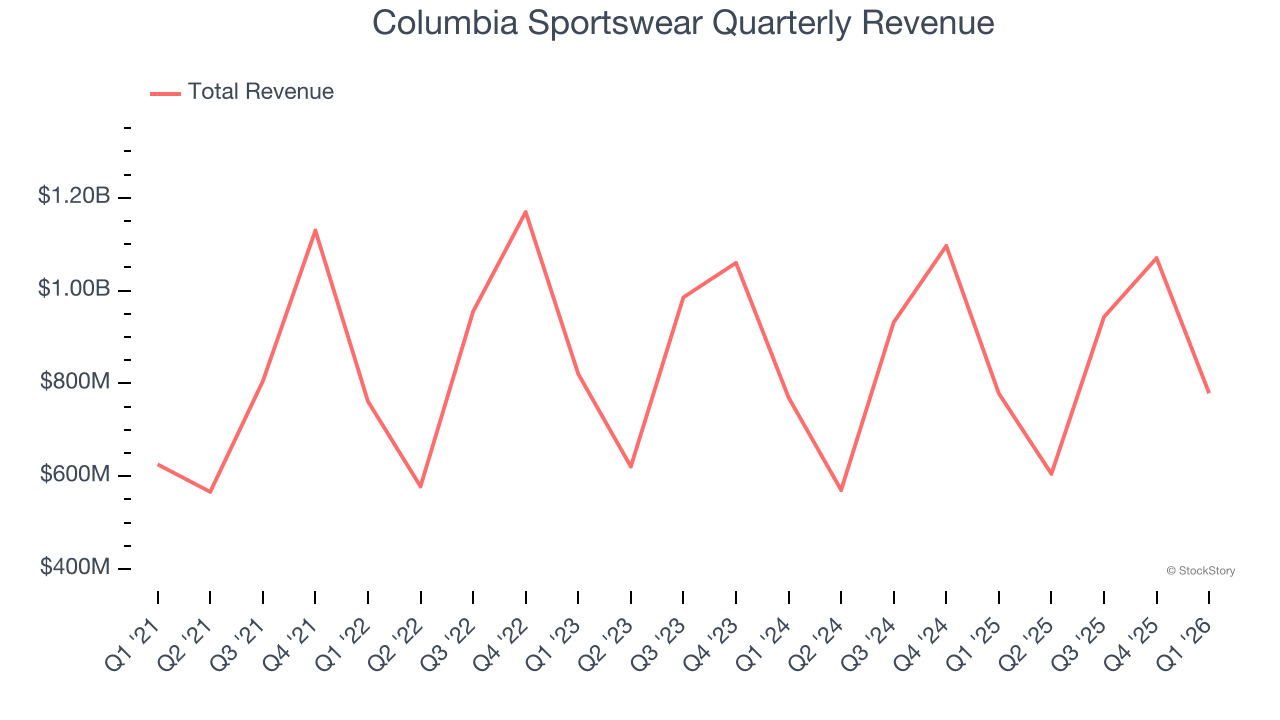

- Revenue: $779 million vs analyst estimates of $759.2 million (flat year on year, 2.6% beat)

- EPS (GAAP): $0.65 vs analyst estimates of $0.35 (85.2% beat)

- Adjusted EBITDA: $62.34 million vs analyst estimates of $45.9 million (8% margin, 35.8% beat)

- The company reconfirmed its revenue guidance for the full year of $3.47 billion at the midpoint

- EPS (GAAP) guidance for the full year is $3.78 at the midpoint, beating analyst estimates by 9.6%

- Operating Margin: 5.4%, in line with the same quarter last year

- Free Cash Flow was -$89.99 million compared to -$47.6 million in the same quarter last year

- Constant Currency Revenue was down 3% year on year

- Market Capitalization: $3.14 billion

Chairman and Chief Executive Officer Tim Boyle commented, “We’re pleased to have delivered net sales and profitability exceeding our guidance for the first quarter, driven by early Spring 2026 wholesale shipments and better-than-expected demand in Europe and the U.S. The strength of our international business continues to lead our growth. Our U.S. business declined, which was largely expected due to a lower Spring 2026 wholesale order book, and our decisions taken last year to reduce supply of winter season products as a precautionary measure in response to U.S. tariff announcements.

Company Overview

Originally founded as a hat store in 1938, Columbia Sportswear (NASDAQ: COLM) is a manufacturer of outerwear, sportswear, and footwear designed for outdoor enthusiasts.

Revenue Growth

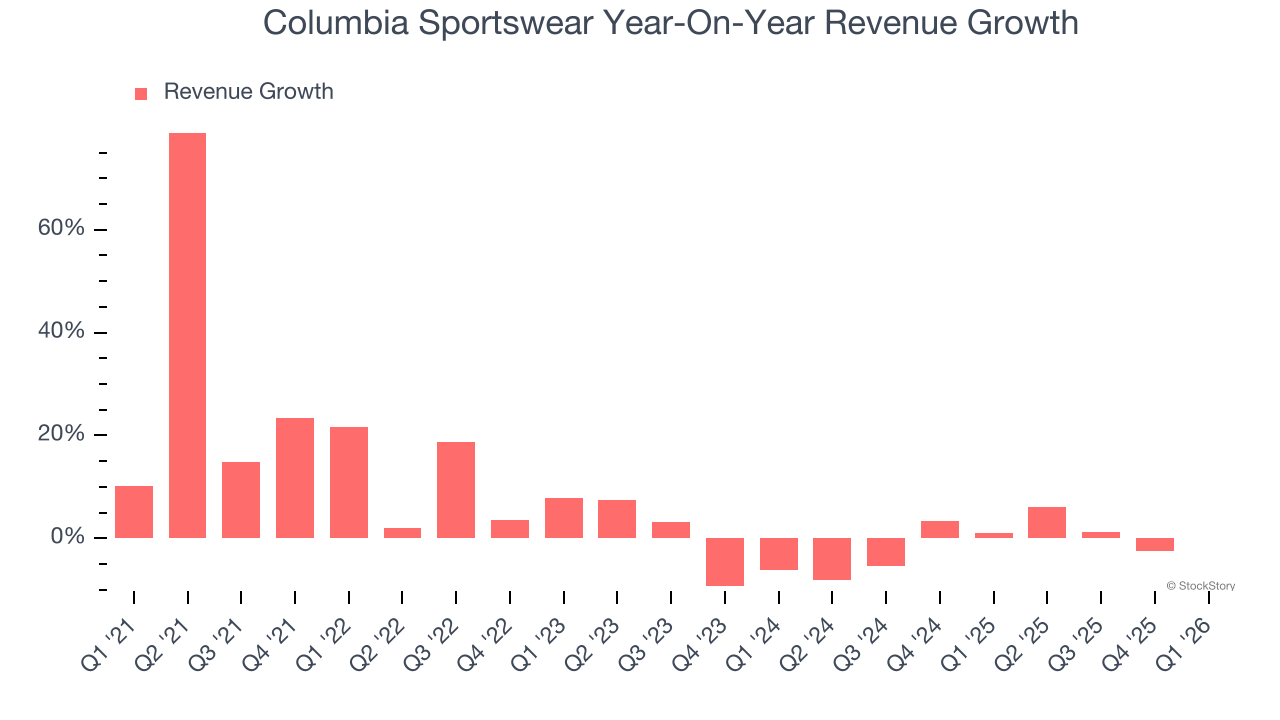

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Columbia Sportswear grew its sales at a weak 5.8% compounded annual growth rate. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Columbia Sportswear’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Columbia Sportswear’s $779 million of revenue was flat year on year but beat Wall Street’s estimates by 2.6%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

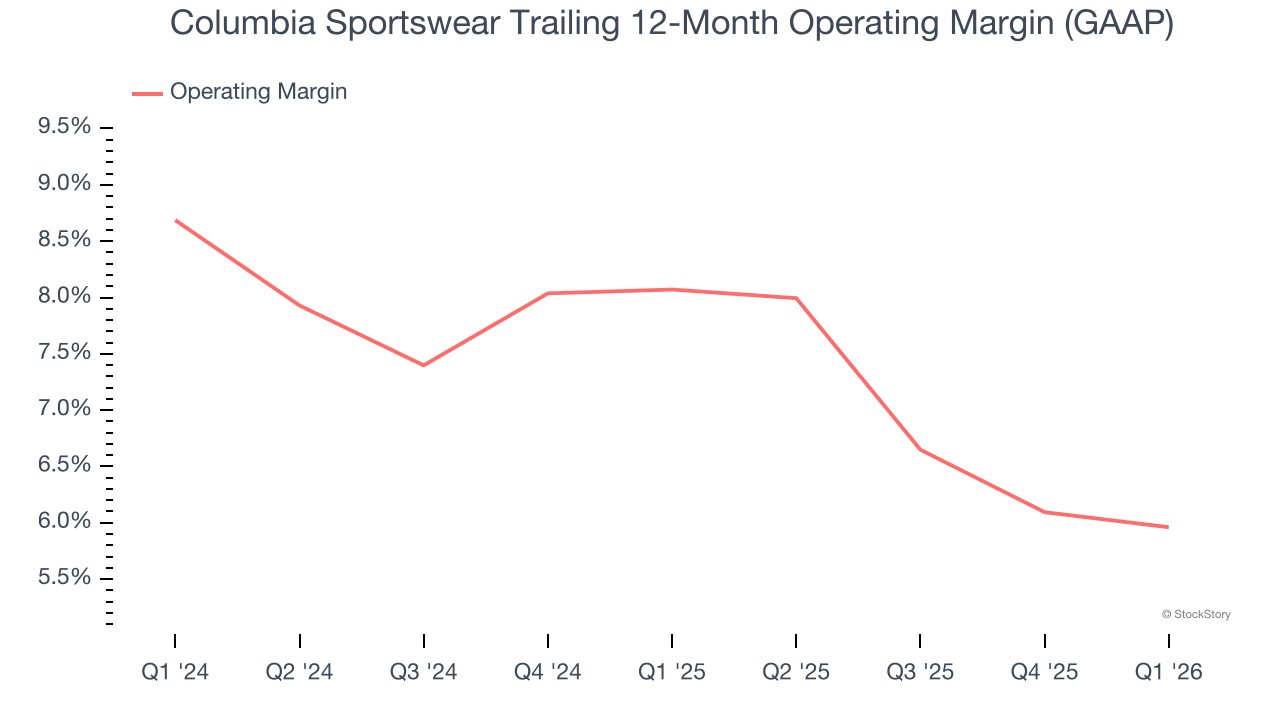

Columbia Sportswear’s operating margin has been trending down over the last 12 months and averaged 7% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q1, Columbia Sportswear generated an operating margin profit margin of 5.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

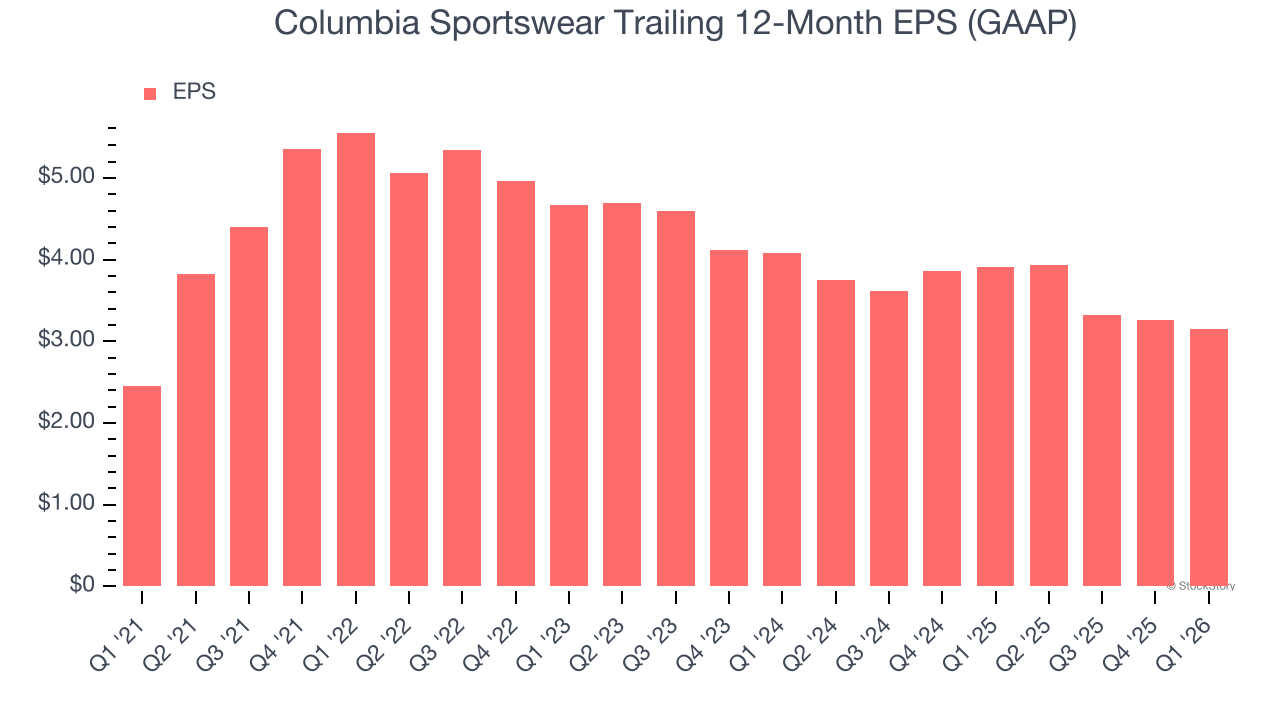

Columbia Sportswear’s weak 5.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Columbia Sportswear reported EPS of $0.65, down from $0.75 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Columbia Sportswear’s full-year EPS of $3.15 to grow 13.9%.

Key Takeaways from Columbia Sportswear’s Q1 Results

We were impressed by Columbia Sportswear’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue and EPS in the quarter outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 2.5% to $62.41 immediately after reporting.

Sure, Columbia Sportswear had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).