The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Flex (NASDAQ: FLEX) and the rest of the electronic components & manufacturing stocks fared in Q4.

The sector could see higher demand as the prevalence of advanced electronics increases in industries such as automotive, healthcare, aerospace, and computing. The high-performance components and contract manufacturing expertise required for autonomous vehicles and cloud computing datacenters, for instance, will benefit companies in the space. However, headwinds include geopolitical risks, particularly U.S.-China trade tensions that could disrupt component sourcing and production as the Trump administration takes an increasingly antagonizing stance on foreign relations. Additionally, stringent environmental regulations on e-waste and emissions could force the industry to pivot in potentially costly ways.

The 10 electronic components & manufacturing stocks we track reported a very strong Q4. As a group, revenues beat analysts’ consensus estimates by 2.8% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.7% on average since the latest earnings results.

Flex (NASDAQ: FLEX)

Originally known as Flextronics until its 2016 rebranding, Flex (NASDAQ: FLEX) is a global manufacturing partner that designs, engineers, and builds products for companies across industries from medical devices to solar trackers.

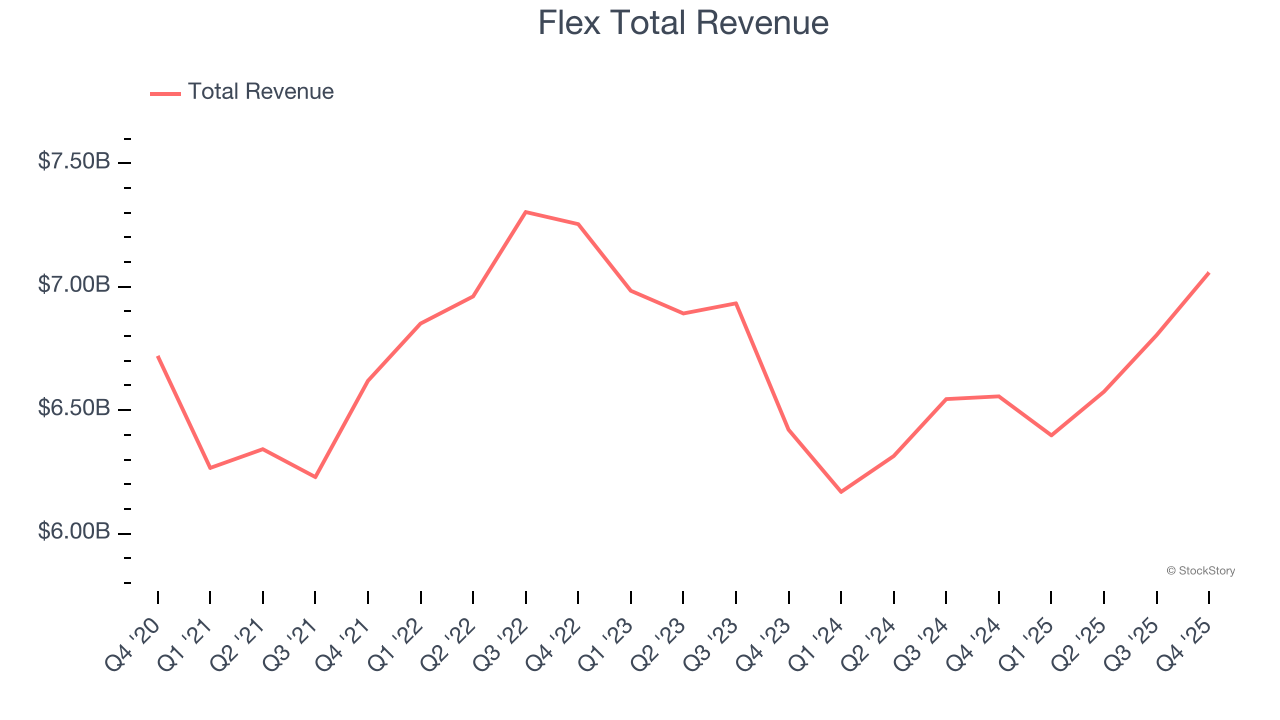

Flex reported revenues of $7.06 billion, up 7.7% year on year. This print exceeded analysts’ expectations by 3.6%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ full-year EPS guidance estimates and a solid beat of analysts’ revenue estimates.

Revathi Advaithi, CEO of Flex, stated: "Our strong performance continued in the third quarter, with results exceeding our guidance across all metrics. This performance reflects the strength of our diversified business model across industries, including Data Center. As we look ahead, we are confident in our ability to serve as a strategic enabler for our customers as they navigate an increasingly complex and dynamic world."

Interestingly, the stock is up 1.5% since reporting and currently trades at $67.

Is now the time to buy Flex? Access our full analysis of the earnings results here, it’s free.

Best Q4: Jabil (NYSE: JBL)

With manufacturing facilities spanning the globe from China to Mexico to the United States, Jabil (NYSE: JBL) provides electronics design, manufacturing, and supply chain solutions to companies across various industries, from healthcare to automotive to cloud computing.

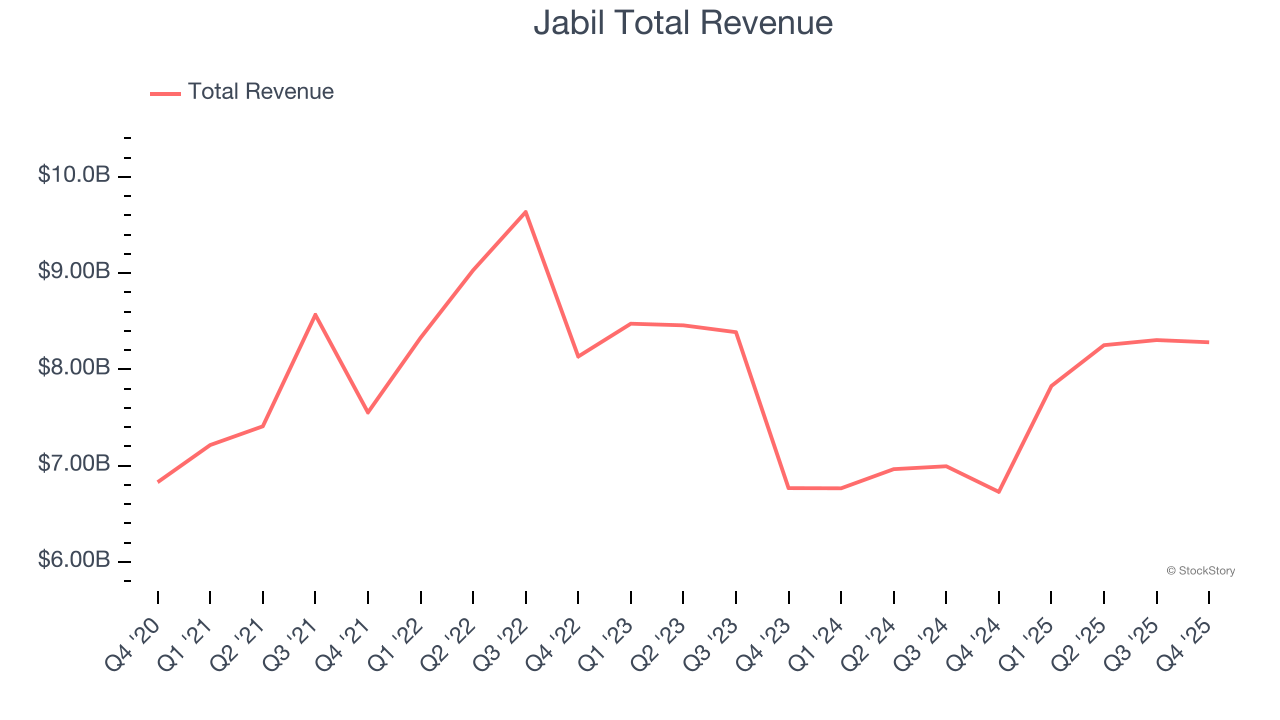

Jabil reported revenues of $8.28 billion, up 23.1% year on year, outperforming analysts’ expectations by 6.8%. The business had a stunning quarter with a solid beat of analysts’ revenue estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Jabil achieved the biggest analyst estimates beat among its peers. The market seems content with the results as the stock is up 4.1% since reporting. It currently trades at $273.

Is now the time to buy Jabil? Access our full analysis of the earnings results here, it’s free.

Slowest Q4: Rogers (NYSE: ROG)

With roots dating back to 1832, making it one of America's oldest continuously operating companies, Rogers (NYSE: ROG) designs and manufactures specialized engineered materials and components used in electric vehicles, telecommunications, renewable energy, and other high-performance applications.

Rogers reported revenues of $201.5 million, up 4.8% year on year, exceeding analysts’ expectations by 2.5%. Still, it was a slower quarter as it posted revenue guidance for next quarter missing analysts’ expectations significantly and a significant miss of analysts’ EPS guidance for next quarter estimates.

Rogers delivered the slowest revenue growth in the group. Interestingly, the stock is up 2.3% since the results and currently trades at $105.50.

Read our full analysis of Rogers’s results here.

Coherent (NYSE: COHR)

Created through the 2022 rebranding of II-VI Incorporated, a company with roots dating back to 1971, Coherent (NYSE: COHR) develops and manufactures advanced materials, lasers, and optical components for applications ranging from telecommunications to industrial manufacturing.

Coherent reported revenues of $1.69 billion, up 17.5% year on year. This number surpassed analysts’ expectations by 2.9%. Overall, it was an exceptional quarter as it also put up revenue guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EPS guidance for next quarter estimates.

The stock is up 22.2% since reporting and currently trades at $257.77.

Read our full, actionable report on Coherent here, it’s free.

CTS (NYSE: CTS)

With roots dating back to 1896 and a global manufacturing footprint, CTS (NYSE: CTS) designs and manufactures sensors, connectivity components, and actuators for aerospace, defense, industrial, medical, and transportation markets.

CTS reported revenues of $137.3 million, up 8.5% year on year. This result beat analysts’ expectations by 1%. Zooming out, it was a mixed quarter as it also recorded a beat of analysts’ EPS estimates but a slight miss of analysts’ full-year EPS guidance estimates.

CTS delivered the highest full-year guidance raise among its peers. The stock is down 12.9% since reporting and currently trades at $48.39.

Read our full, actionable report on CTS here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.