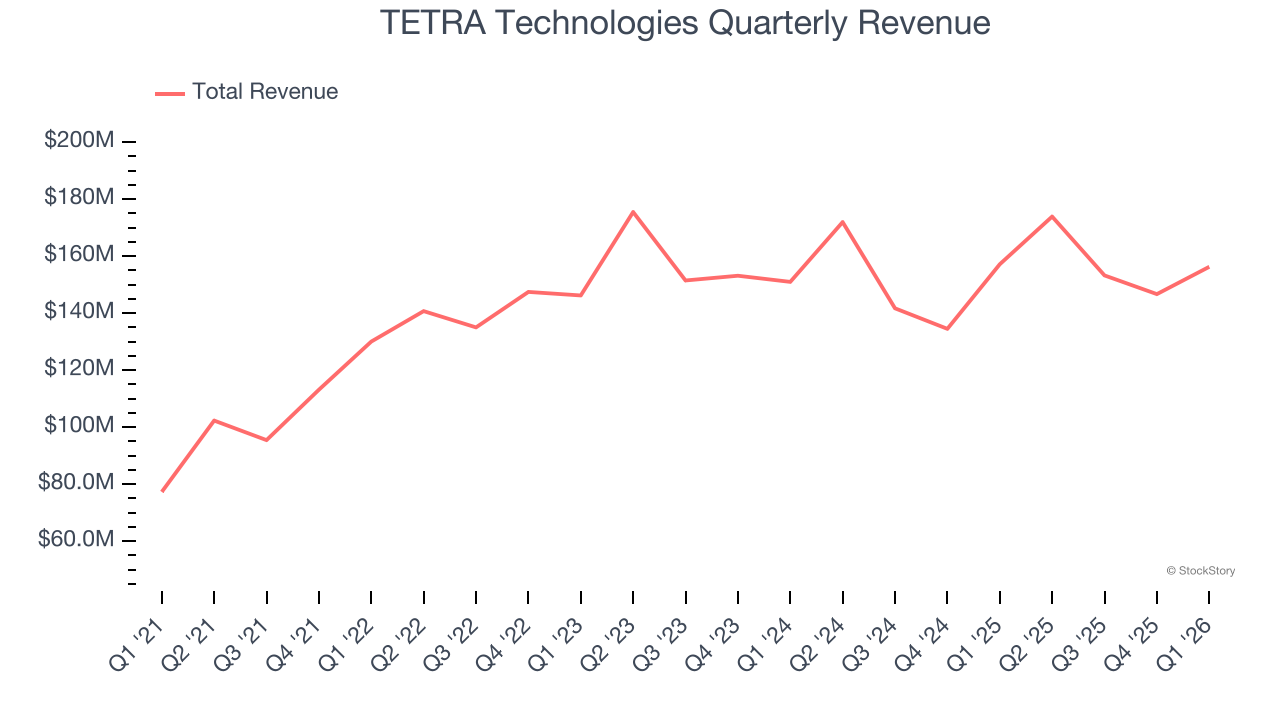

Oilfield services company TETRA Technologies (NYSE: TTI) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, but sales were flat year on year at $156.3 million. Its non-GAAP profit of $0.06 per share was significantly above analysts’ consensus estimates.

Is now the time to buy TETRA Technologies? Find out by accessing our full research report, it’s free.

TETRA Technologies (TTI) Q1 CY2026 Highlights:

- Revenue: $156.3 million vs analyst estimates of $151.2 million (flat year on year, 3.4% beat)

- Adjusted EPS: $0.06 vs analyst estimates of $0.03 (significant beat)

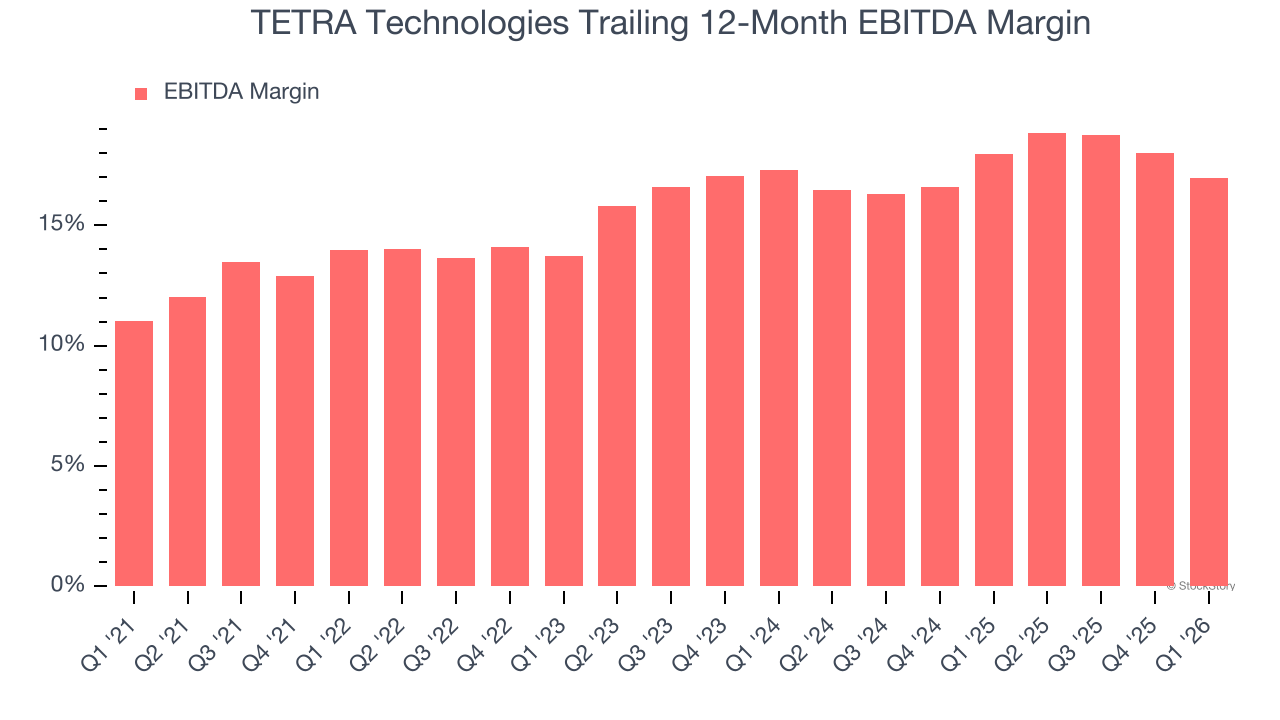

- Adjusted EBITDA: $25.61 million vs analyst estimates of $21.4 million (16.4% margin, 19.7% beat)

- Operating Margin: 8.2%, up from -19.7% in the same quarter last year

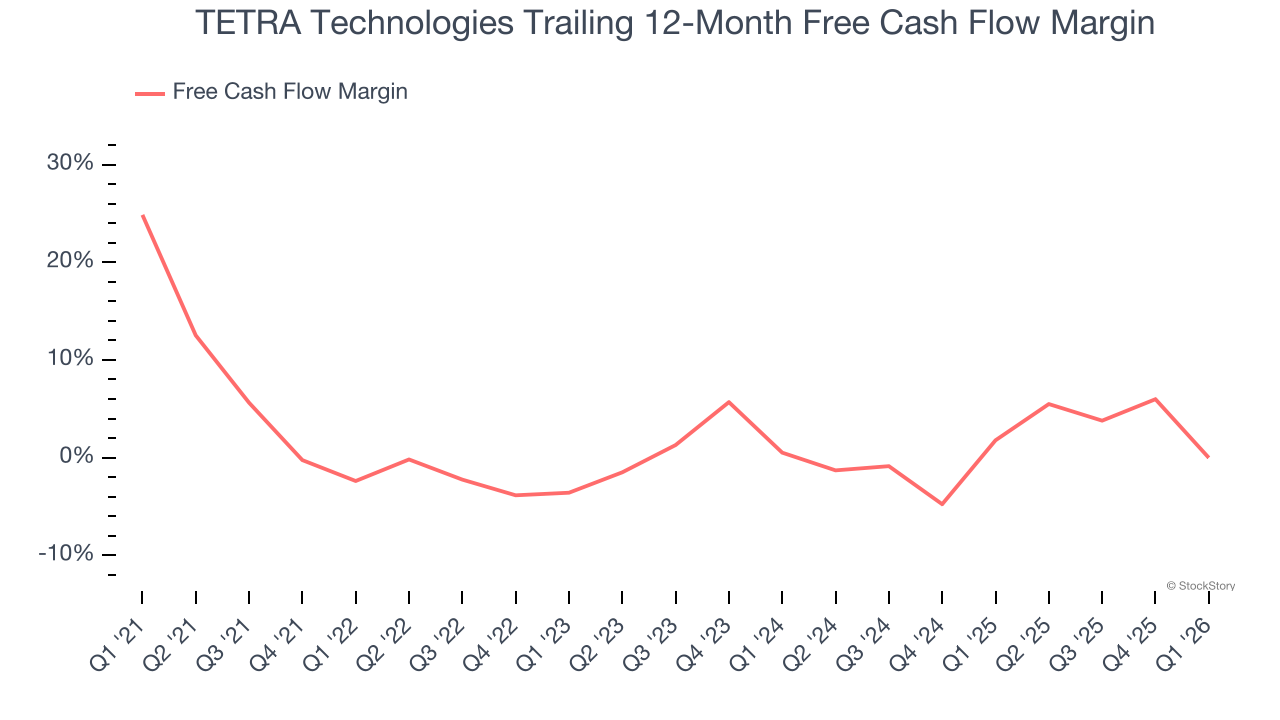

- Free Cash Flow was -$31.91 million, down from $5.89 million in the same quarter last year

- Market Capitalization: $1.32 billion

Brady Murphy, TETRA's President and Chief Executive Officer, stated, "We are pleased to start 2026 with one of the strongest first quarter performances in the company's past ten years. Excluding the benefit of TETRA Neptune in the prior-year period, consolidated first-quarter revenue of $156 million and Adjusted EBITDA of $26 million were ten-year highs for a first quarter, as were both Brazil and Gulf of America. In addition, the Industrial Chemicals and Production Testing subsegments each delivered ten-year-high revenues with strong margin contributions. High-pressure gas plays in Haynesville and South Texas, supporting Gulf Coast LNG, are areas that should experience rapid growth in the coming years."

Company Overview

Operating across six continents with approximately 40,000 acres of mineral-rich brine leases in Arkansas, TETRA Technologies (NYSE: TTI) provides well completion fluids and water management services to oil and gas operators.

Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Thankfully, TETRA Technologies’s 14.3% annualized revenue growth over the last five years was solid. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. TETRA Technologies’s ten year performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 4.7% over the last ten years.

This quarter, TETRA Technologies’s $156.3 million of revenue was flat year on year but beat Wall Street’s estimates by 3.4%.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted EBITDA Margin

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

TETRA Technologies was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 16.2% was among the worst in the energy upstream and integrated energy sector.

On the plus side, TETRA Technologies’s EBITDA margin rose by 3 percentage points over the last year.

In Q1, TETRA Technologies generated an EBITDA margin profit margin of 16.4%, down 4.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA beat Wall Street’s estimates by 19.7%.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

TETRA Technologies broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

While the level of free cash flow margins is important, their consistency matters just as much.

TETRA Technologies’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 115.4 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of TETRA Technologies? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

TETRA Technologies burned through $31.91 million of cash in Q1, equivalent to a negative 20.4% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from TETRA Technologies’s Q1 Results

It was good to see TETRA Technologies beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 6% to $10.30 immediately after reporting.

TETRA Technologies put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).