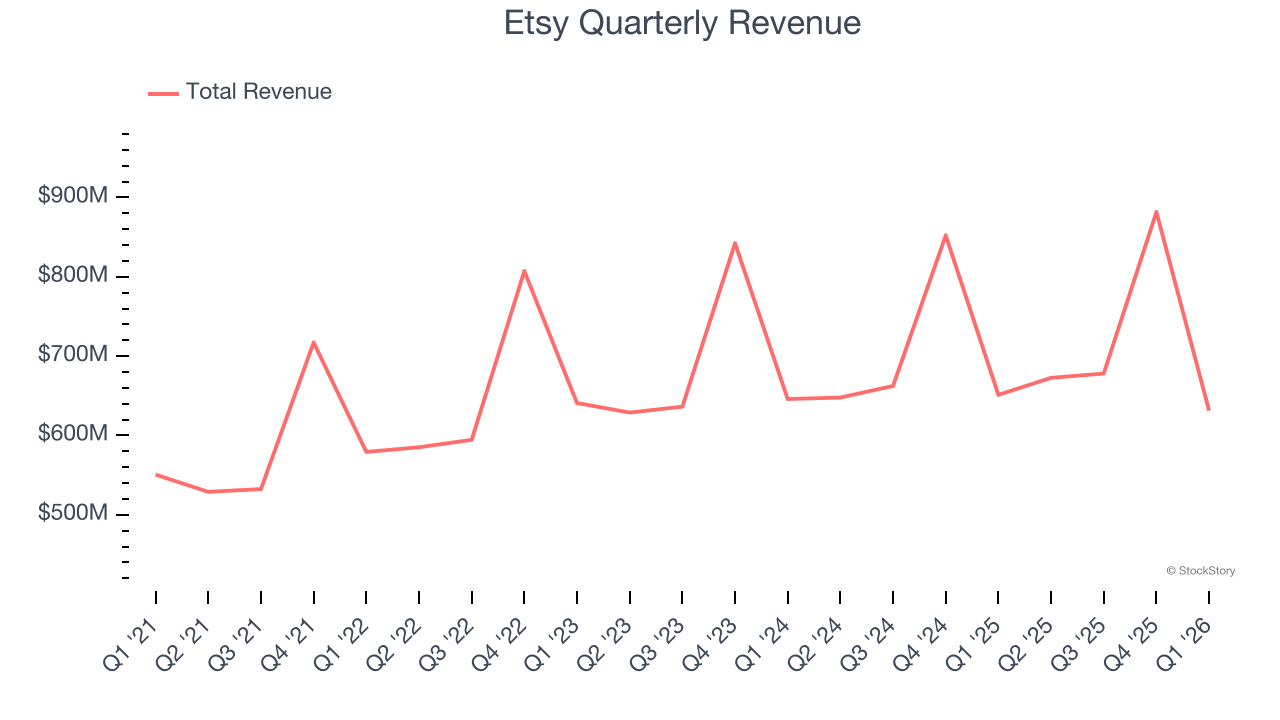

Online marketplace Etsy (NYSE: ETSY) beat Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 3.1% year on year to $631.3 million. Its GAAP profit of $0.60 per share was 3.5% below analysts’ consensus estimates.

Is now the time to buy Etsy? Find out by accessing our full research report, it’s free.

Etsy (ETSY) Q1 CY2026 Highlights:

- Revenue: $631.3 million vs analyst estimates of $616.7 million (3.1% year-on-year decline, 2.4% beat)

- EPS (GAAP): $0.60 vs analyst expectations of $0.62 (3.5% miss)

- Adjusted EBITDA: $184.7 million vs analyst estimates of $177.2 million (29.3% margin, 4.2% beat)

- Operating Margin: 19%, up from -3.4% in the same quarter last year

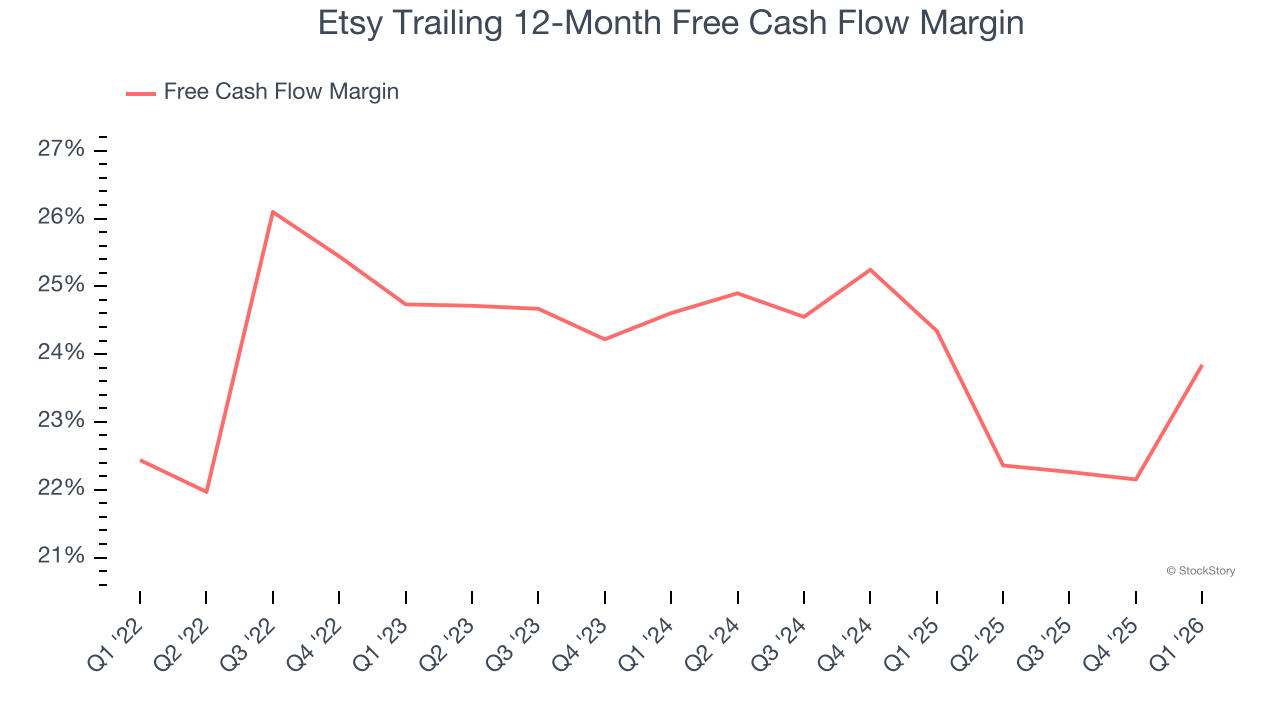

- Free Cash Flow Margin: 12.6%, down from 34.9% in the previous quarter

- Market Capitalization: $6.01 billion

Company Overview

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NYSE: ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, Etsy grew its sales at a sluggish 2.9% compounded annual growth rate. This was below our standards and is a rough starting point for our analysis.

This quarter, Etsy’s revenue fell by 3.1% year on year to $631.3 million but beat Wall Street’s estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to decline by 3.7% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products and services will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Etsy has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 24.1% over the last two years.

Etsy’s free cash flow clocked in at $79.26 million in Q1, equivalent to a 12.6% margin. This result was good as its margin was 7.1 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Key Takeaways from Etsy’s Q1 Results

We enjoyed seeing Etsy beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 6.2% to $68.14 immediately after reporting.

Indeed, Etsy had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).