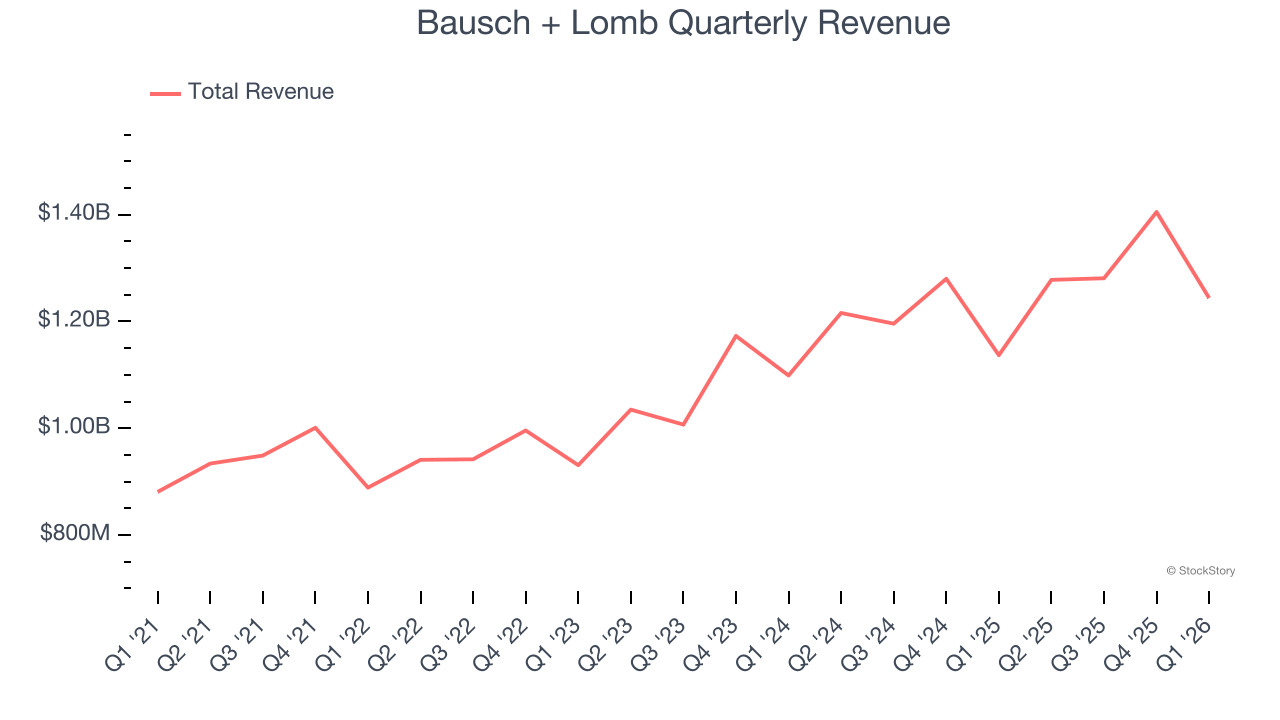

Eyecare company Bausch + Lomb (NYSE: BLCO) announced better-than-expected revenue in Q1 CY2026, with sales up 9.4% year on year to $1.24 billion. The company’s full-year revenue guidance of $5.47 billion at the midpoint came in 0.6% above analysts’ estimates. Its non-GAAP profit of $0.08 per share was 49.2% above analysts’ consensus estimates.

Is now the time to buy Bausch + Lomb? Find out by accessing our full research report, it’s free.

Bausch + Lomb (BLCO) Q1 CY2026 Highlights:

- Revenue: $1.24 billion vs analyst estimates of $1.22 billion (9.4% year-on-year growth, 2.2% beat)

- Adjusted EPS: $0.08 vs analyst estimates of $0.05 (49.2% beat)

- Adjusted EBITDA: $189 million vs analyst estimates of $188.3 million (15.2% margin, in line)

- The company slightly lifted its revenue guidance for the full year to $5.47 billion at the midpoint from $5.43 billion

- EBITDA guidance for the full year is $1.04 billion at the midpoint, in line with analyst expectations

- Operating Margin: 2.7%, up from -7.3% in the same quarter last year

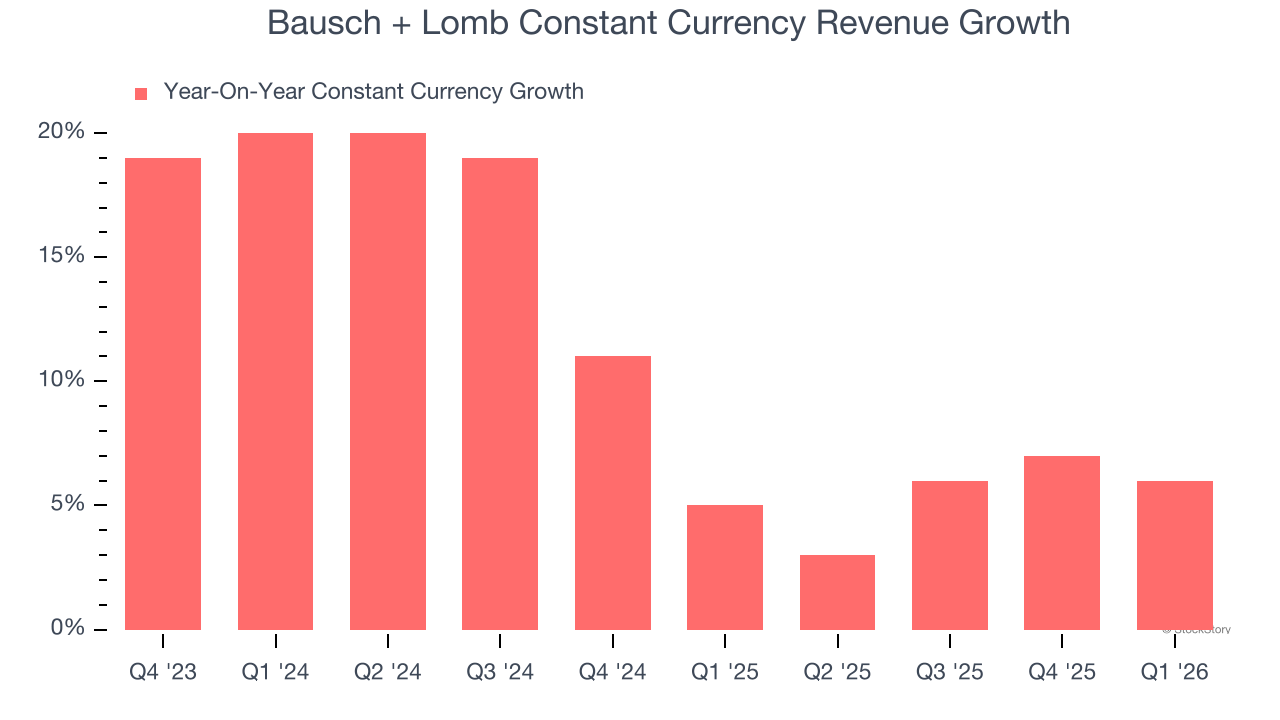

- Constant Currency Revenue rose 6% year on year, in line with the same quarter last year

- Market Capitalization: $5.60 billion

Company Overview

With a nearly 170-year history dedicated to vision care and eye health innovation, Bausch + Lomb (NYSE: BLCO) develops and manufactures a comprehensive range of eye health products including contact lenses, pharmaceuticals, surgical devices, and consumer eye care solutions.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Bausch + Lomb’s 8.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Bausch + Lomb’s annualized revenue growth of 9.9% over the last two years is above its five-year trend, suggesting some bright spots.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 9.6% year-on-year growth. Because this number aligns with its reported revenue growth, we can see that foreign exchange has not had a meaningful impact on topline.

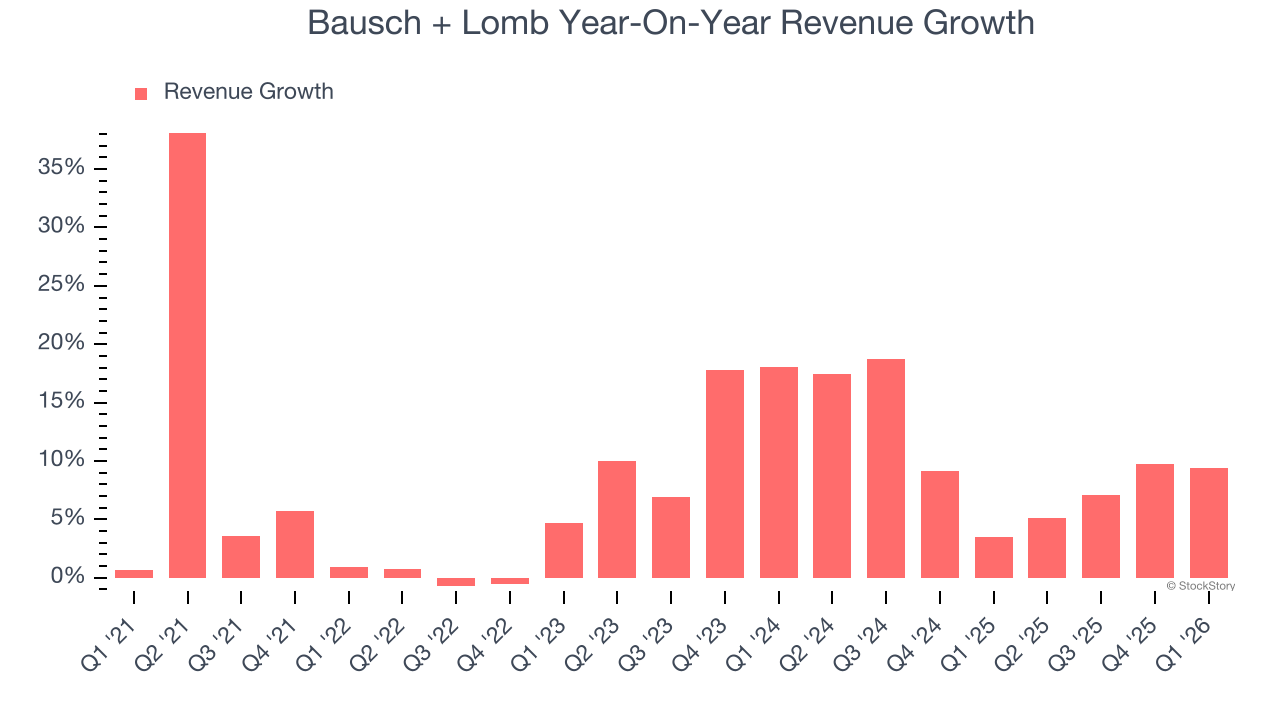

This quarter, Bausch + Lomb reported year-on-year revenue growth of 9.4%, and its $1.24 billion of revenue exceeded Wall Street’s estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and indicates the market sees some success for its newer products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

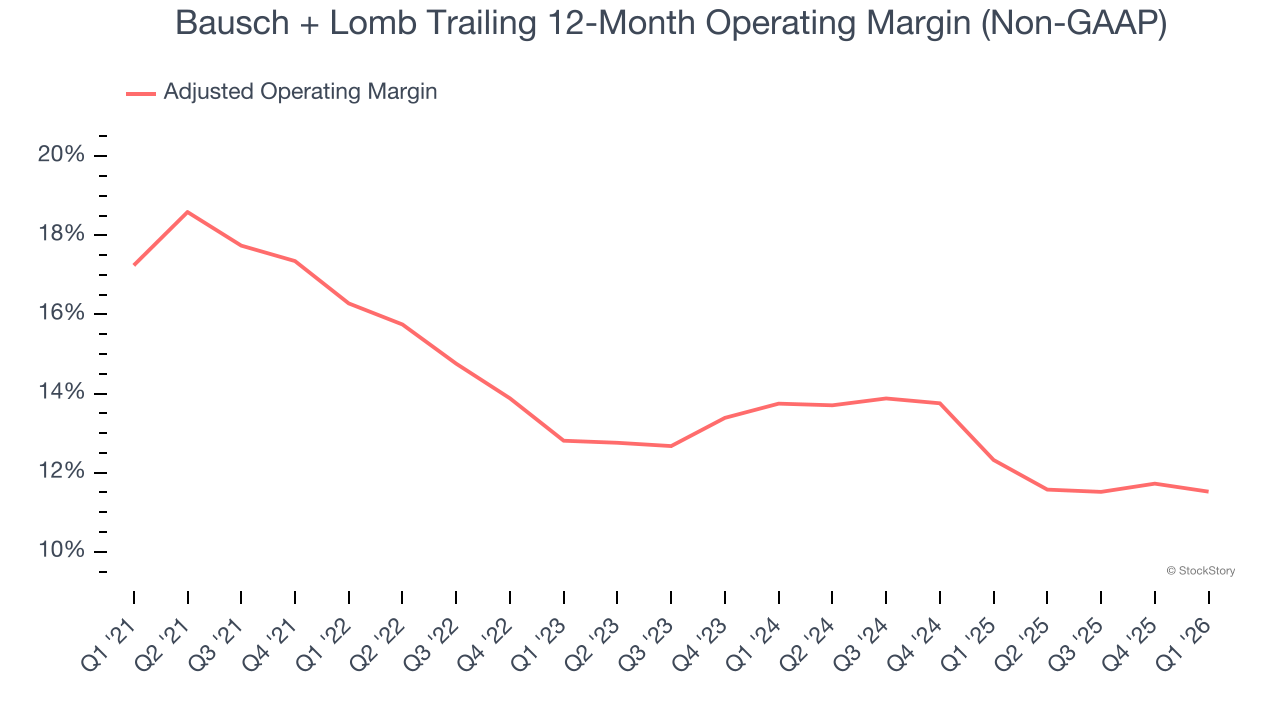

Adjusted Operating Margin

Bausch + Lomb has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 13.2%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Bausch + Lomb’s adjusted operating margin decreased by 4.8 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 2.2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Bausch + Lomb generated an adjusted operating margin profit margin of 5.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

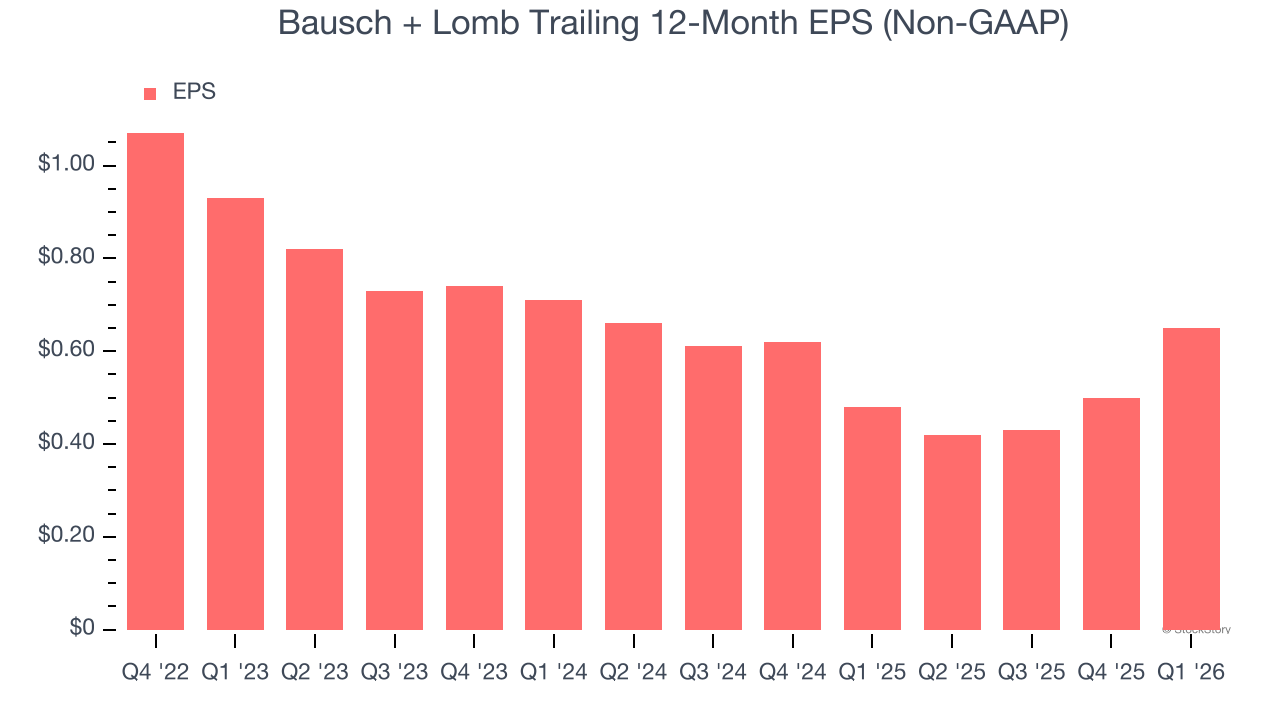

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Bausch + Lomb’s full-year EPS dropped 96.8%, or 25.3% annually, over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Bausch + Lomb’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, Bausch + Lomb reported adjusted EPS of $0.08, up from negative $0.07 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Bausch + Lomb’s Q1 Results

It was good to see Bausch + Lomb beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $15.72 immediately after reporting.

Bausch + Lomb may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).