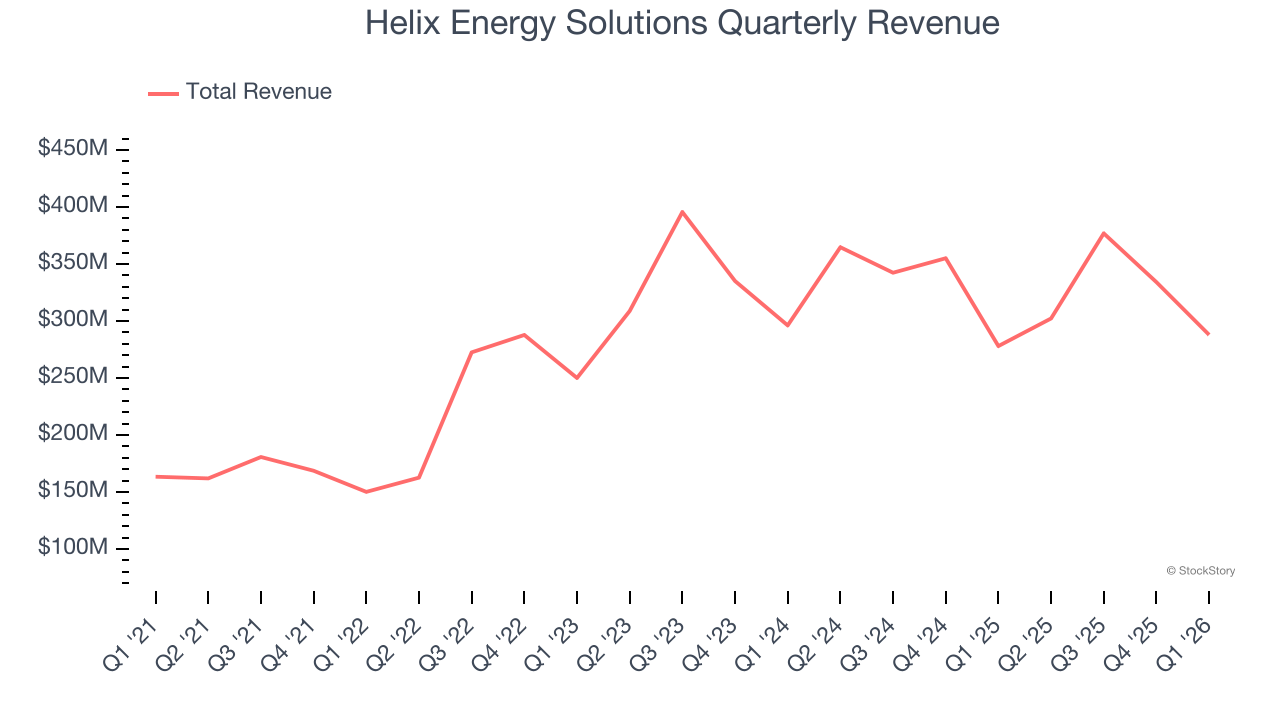

Offshore energy services company Helix Energy Solutions (NYSE: HLX) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 3.6% year on year to $287.9 million. Its GAAP loss of $0.09 per share was in line with analysts’ consensus estimates.

Is now the time to buy Helix Energy Solutions? Find out by accessing our full research report, it’s free.

Helix Energy Solutions (HLX) Q1 CY2026 Highlights:

- Revenue: $287.9 million vs analyst estimates of $265.7 million (3.6% year-on-year growth, 8.4% beat)

- EPS (GAAP): -$0.09 vs analyst estimates of -$0.09 (in line)

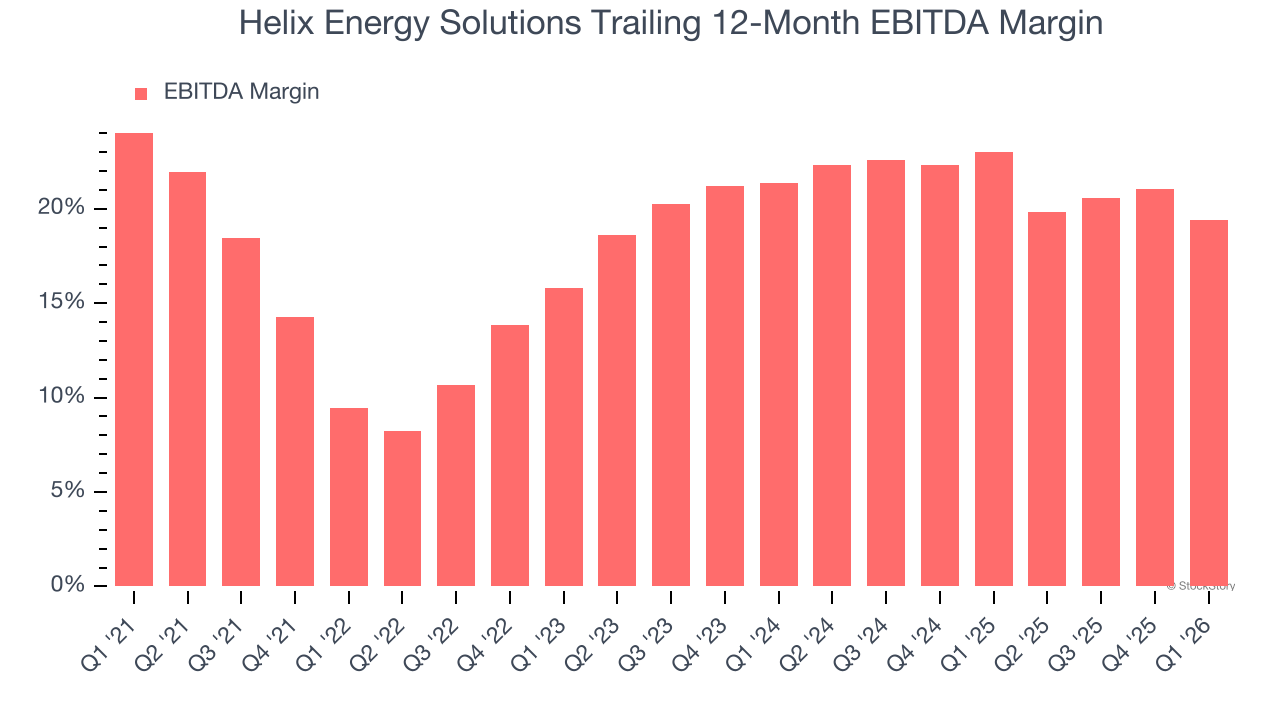

- Adjusted EBITDA: $32.26 million vs analyst estimates of $36.28 million (11.2% margin, 11.1% miss)

- Operating Margin: -4.6%, down from 2.9% in the same quarter last year

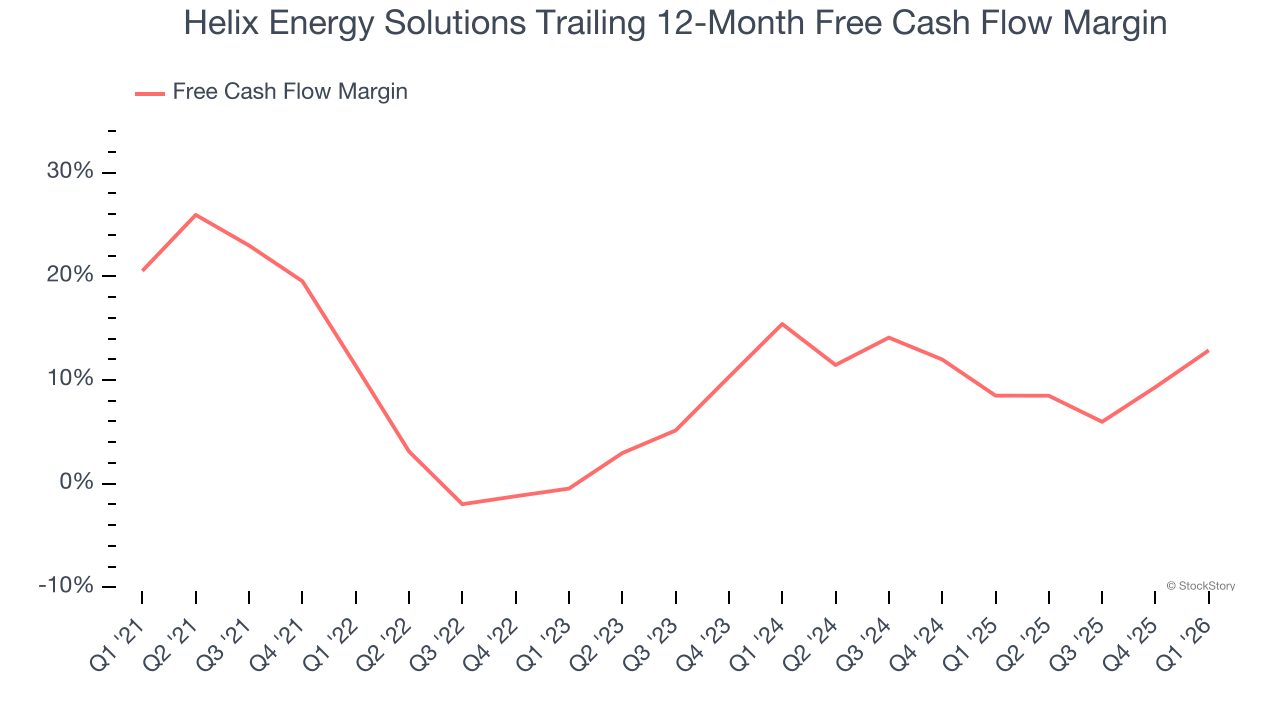

- Free Cash Flow Margin: 20.5%, up from 4.3% in the same quarter last year

- Market Capitalization: $1.42 billion

Owen Kratz, President and Chief Executive Officer of Helix, stated, “Our first quarter results reflect the expected seasonal slowdown of operations in the North Sea and Gulf of America shelf as well as the costs of the successful workover of our Thunder Hawk field during the quarter. Nonetheless, we generated $59 million of Free Cash Flow and ended the quarter with over half a billion dollars in cash providing Helix with tremendous opportunities. While we face ongoing macro uncertainties and softness in some of the markets we serve, the recent commodity price increases have generated improved demand for our services, and recent government actions in the North Sea have provided a regulatory catalyst to spur decommissioning activities by our customers. Helix continues to expect momentum to build in the offshore market in the latter half of 2026 and into 2027 and is poised to capitalize on those opportunities.”

Company Overview

Playing a pivotal role in the 2010 Macondo oil spill response with its Q4000 vessel, Helix Energy Solutions (NYSE: HLX) provides specialized services to extend the life of offshore oil and gas wells and decommission aging infrastructure.

Revenue Growth

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Thankfully, Helix Energy Solutions’s 12.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Helix Energy Solutions’s annualized revenue growth of 8.1% over the last ten years is below its five-year trend, but we still think the results were good.

This quarter, Helix Energy Solutions reported modest year-on-year revenue growth of 3.6% but beat Wall Street’s estimates by 8.4%.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted EBITDA Margin

Helix Energy Solutions was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 18.9% was weak for an upstream and integrated energy business.

On the plus side, Helix Energy Solutions’s EBITDA margin rose by 9.9 percentage points over the last year, as its sales growth gave it operating leverage.

In Q1, Helix Energy Solutions generated an EBITDA margin profit margin of 11.2%, down 7.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

Helix Energy Solutions has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.9% over the last five years, slightly better than the broader energy upstream and integrated energy sector.

Absolute FCF margin levels matter but so does stability of free cash flow. All else equal, we’d prefer a 25.0% average free cash flow margin that is quite steady no matter how commodity prices behave rather than extremely high margins when times are good and negative ones when they’re tough.

Helix Energy Solutions’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 8.8 (lower is better), indicating reasonable insulation from commodity swings.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Helix Energy Solutions? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Helix Energy Solutions’s free cash flow clocked in at $58.98 million in Q1, equivalent to a 20.5% margin. This result was good as its margin was 16.2 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Helix Energy Solutions’s Q1 Results

We were impressed by how significantly Helix Energy Solutions blew past analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed. Overall, this was a mixed quarter. The stock remained flat at $9.60 immediately following the results.

Helix Energy Solutions’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).