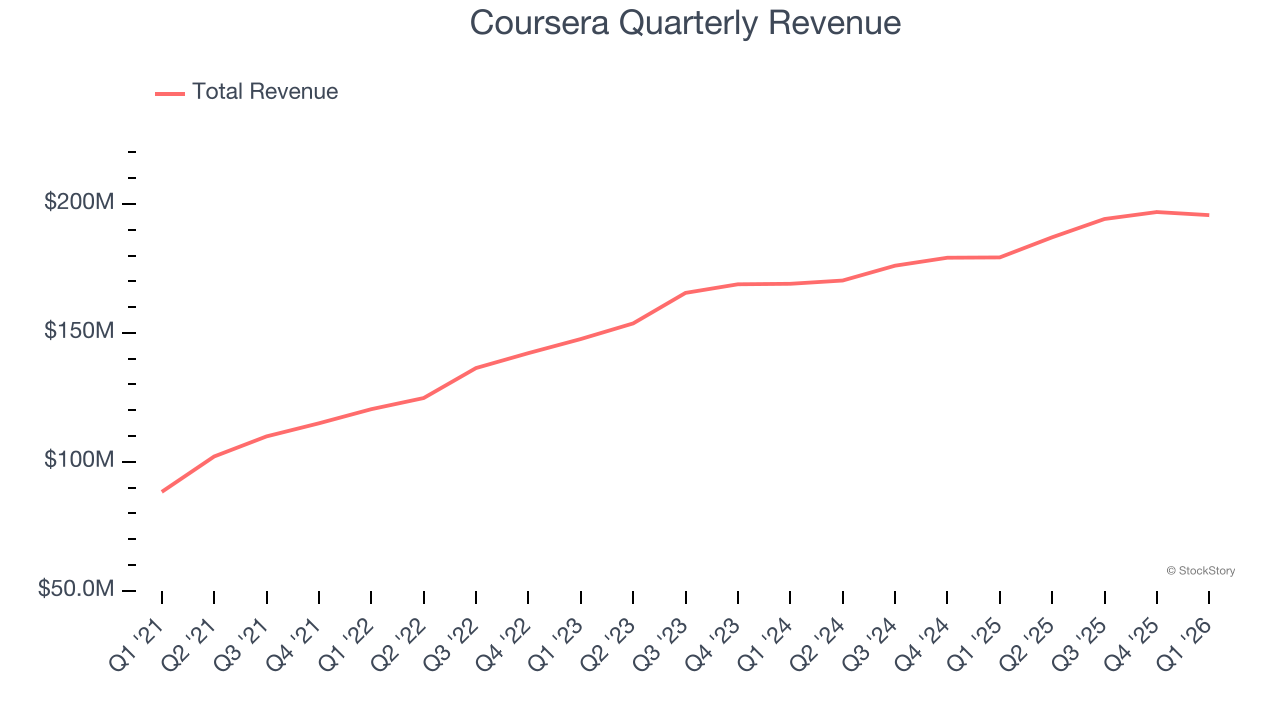

Online learning platform Coursera (NYSE: COUR) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 9.1% year on year to $195.7 million. On the other hand, next quarter’s revenue guidance of $198 million was less impressive, coming in 1.3% below analysts’ estimates. Its non-GAAP profit of $0.07 per share was 15.3% below analysts’ consensus estimates.

Is now the time to buy Coursera? Find out by accessing our full research report, it’s free.

Coursera (COUR) Q1 CY2026 Highlights:

- Revenue: $195.7 million vs analyst estimates of $194.9 million (9.1% year-on-year growth, in line)

- Adjusted EPS: $0.07 vs analyst expectations of $0.08 (15.3% miss)

- Adjusted EBITDA: $13.5 million vs analyst estimates of $13.71 million (6.9% margin, 1.6% miss)

- The company reconfirmed its revenue guidance for the full year of $810 million at the midpoint

- EBITDA guidance for the full year is $73 million at the midpoint, above analyst estimates of $70.99 million

- Operating Margin: -12.9%, down from -8% in the same quarter last year

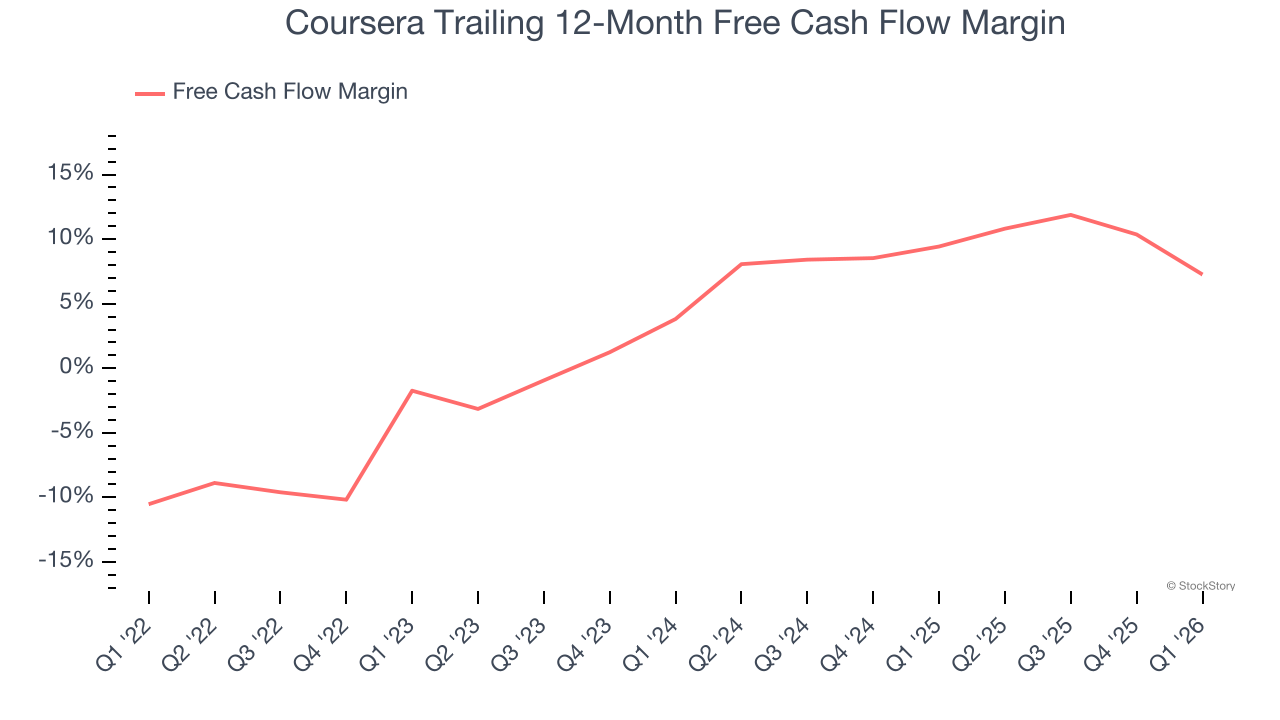

- Free Cash Flow was $3 million, up from -$2 million in the previous quarter

- Market Capitalization: $1.05 billion

“Coursera delivered a strong start to 2026, including our fourth consecutive quarter of double-digit year-over-year Consumer revenue growth and a first quarter record of 7.6 million new registered learners. We have now surpassed more than 200 million cumulative learners, giving us both broad scale and deep insight into how the world learns and the skills employers value at a pivotal moment for global labor markets,” said Coursera CEO Greg Hart.

Company Overview

Founded by two Stanford University computer science professors, Coursera (NYSE: COUR) is an online learning platform that offers courses, specializations, and degrees from top universities and organizations around the world.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Coursera grew its sales at a decent 12% compounded annual growth rate. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, Coursera grew its revenue by 9.1% year on year, and its $195.7 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 5.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Coursera has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.3% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that Coursera’s margin expanded by 9 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Coursera’s free cash flow clocked in at $3 million in Q1, equivalent to a 1.5% margin. The company’s cash profitability regressed as it was 12.6 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from Coursera’s Q1 Results

It was great to see Coursera’s full-year EBITDA guidance top analysts’ expectations. On the other hand, its revenue guidance for next quarter slightly missed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9.1% to $5.42 immediately after reporting.

Coursera’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).