Over the last six months, Amphastar Pharmaceuticals’s shares have sunk to $22.73, producing a disappointing 6.3% loss - a stark contrast to the S&P 500’s 5.8% gain. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Amphastar Pharmaceuticals, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Amphastar Pharmaceuticals Not Exciting?

Even with the cheaper entry price, we're cautious about Amphastar Pharmaceuticals. Here are three reasons there are better opportunities than AMPH and a stock we'd rather own.

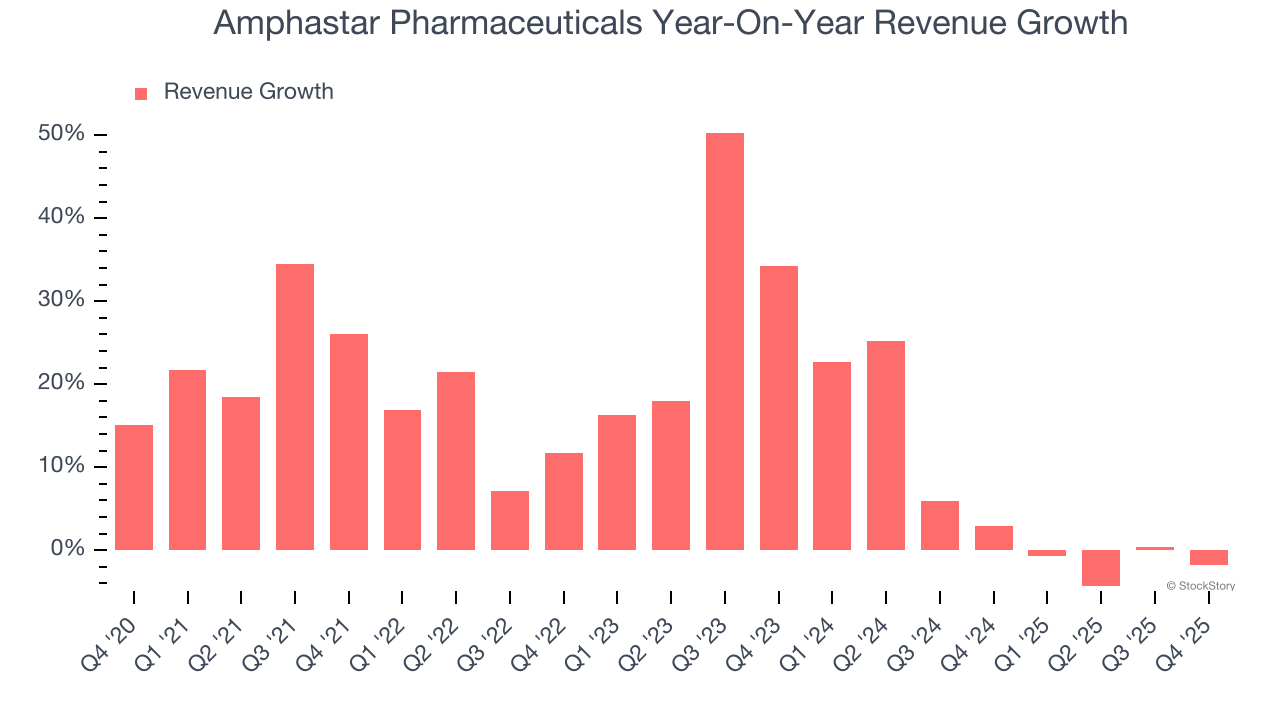

1. Lackluster Revenue Growth

Long-term growth is the most important, but within healthcare, a stretched historical view may miss new innovations or demand cycles. Amphastar Pharmaceuticals’s recent performance shows its demand has slowed as its annualized revenue growth of 5.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

2. Fewer Distribution Channels Limit its Ceiling

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $719.9 million in revenue over the past 12 months, Amphastar Pharmaceuticals is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

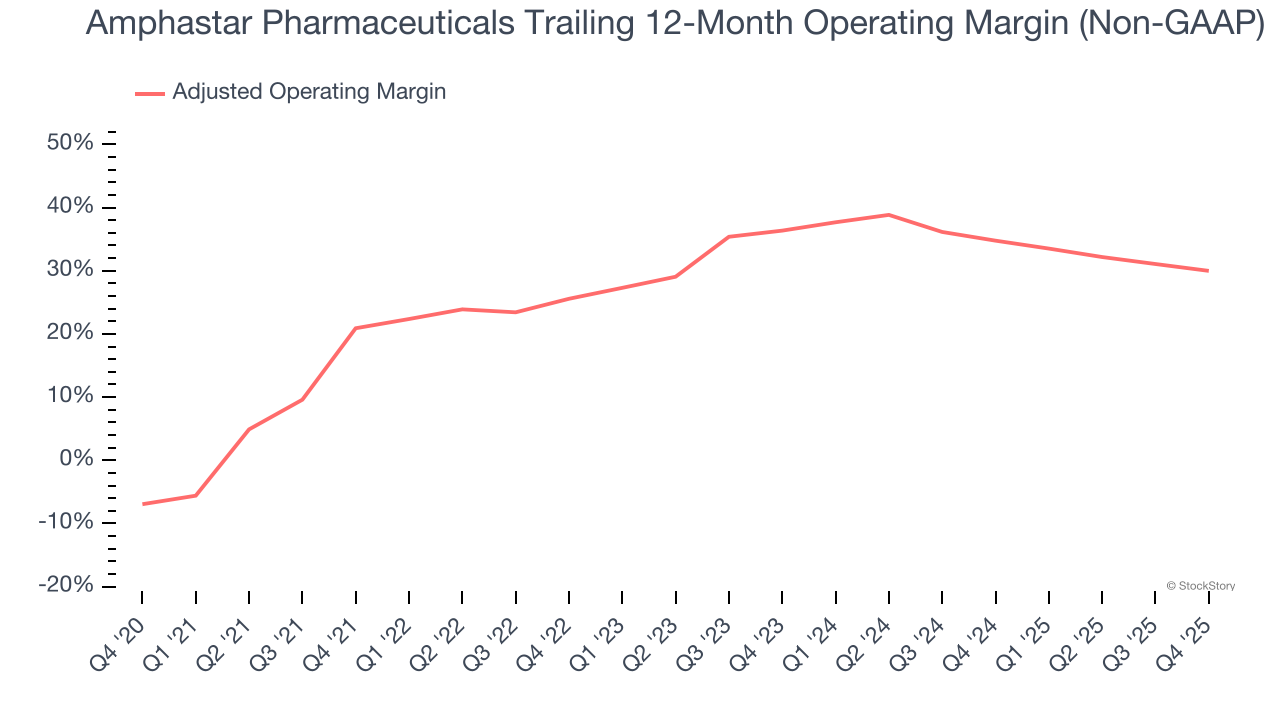

3. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Looking at the trend in its profitability, Amphastar Pharmaceuticals’s adjusted operating margin decreased by 6.4 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 30%.

Final Judgment

Amphastar Pharmaceuticals’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 7× forward P/E (or $22.73 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Amphastar Pharmaceuticals

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.