Occidental Petroleum has had an impressive run over the past six months as its shares have beaten the S&P 500 by 27.3%. The stock now trades at $54.46, marking a 33.1% gain. This run-up might have investors contemplating their next move.

Following the strength, is OXY a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Occidental Petroleum Spark Debate?

Backed by Warren Buffett's Berkshire Hathaway as a major shareholder, Occidental Petroleum (NYSE: OXY) explores for, develops, and produces oil, natural gas liquids, and natural gas, primarily in the United States and Middle East.

Two Positive Attributes:

1. Economies of Scale Give It Negotiating Leverage with Suppliers

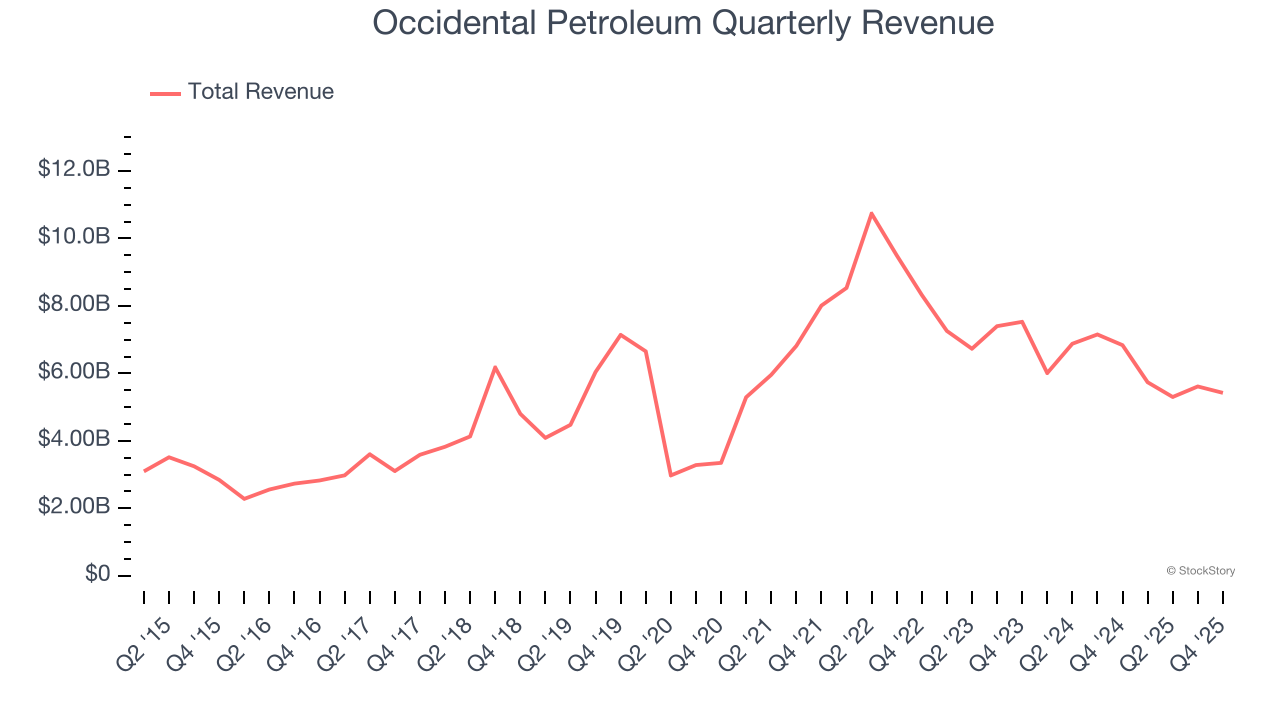

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program.

Occidental Petroleum’s $22.08 billion of revenue in the last year is top-tier for the industry, suggesting the type of diversification that reduces operational risk.

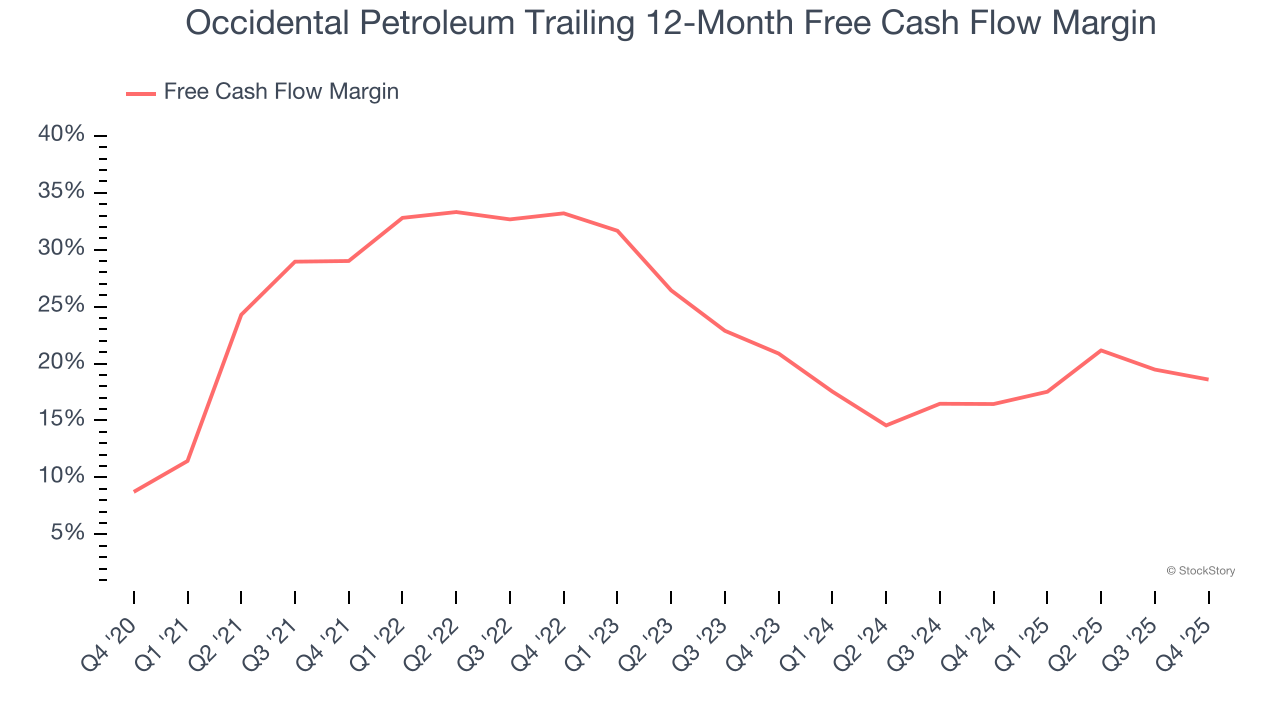

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Occidental Petroleum has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 24.4% over the last five years.

One Reason to be Careful:

Long-Term Revenue Growth Disappoints

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Unfortunately, Occidental Petroleum’s 6.3% annualized revenue growth over the last five years was sluggish. This wasn’t a great result compared to the rest of the energy upstream and integrated energy sector, but there are still things to like about Occidental Petroleum.

Final Judgment

Occidental Petroleum’s positive characteristics outweigh the negatives, and with its shares outperforming the market lately, the stock trades at 11.7× forward P/E (or $54.46 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Occidental Petroleum

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.