The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Quest (NYSE: DGX) and the rest of the testing & diagnostics services stocks fared in Q4.

The testing and diagnostics services industry plays a crucial role in disease detection, monitoring, and prevention, serving hospitals, clinics, and individual consumers. This sector benefits from stable demand, driven by an aging population, increased prevalence of chronic diseases, and growing awareness of preventive healthcare. Recurring revenue streams come from routine screenings, lab tests, and diagnostic imaging, with reimbursement from Medicare, Medicaid, private insurance, and out-of-pocket payments. However, the industry faces challenges such as pricing pressures, regulatory compliance, and the need for continuous investment in new testing technologies. Looking ahead, industry tailwinds include the expansion of personalized medicine, increased adoption of at-home and rapid diagnostic tests, and advancements in AI-driven diagnostics that enhance accuracy and efficiency. However, headwinds such as reimbursement uncertainties, competition from decentralized testing solutions, and regulatory scrutiny over test validity and cost-effectiveness may impact profitability. Adapting to evolving healthcare models and integrating automation will be key for sustaining growth and maintaining operational efficiency.

The 5 testing & diagnostics services stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 2.1%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 15.7% since the latest earnings results.

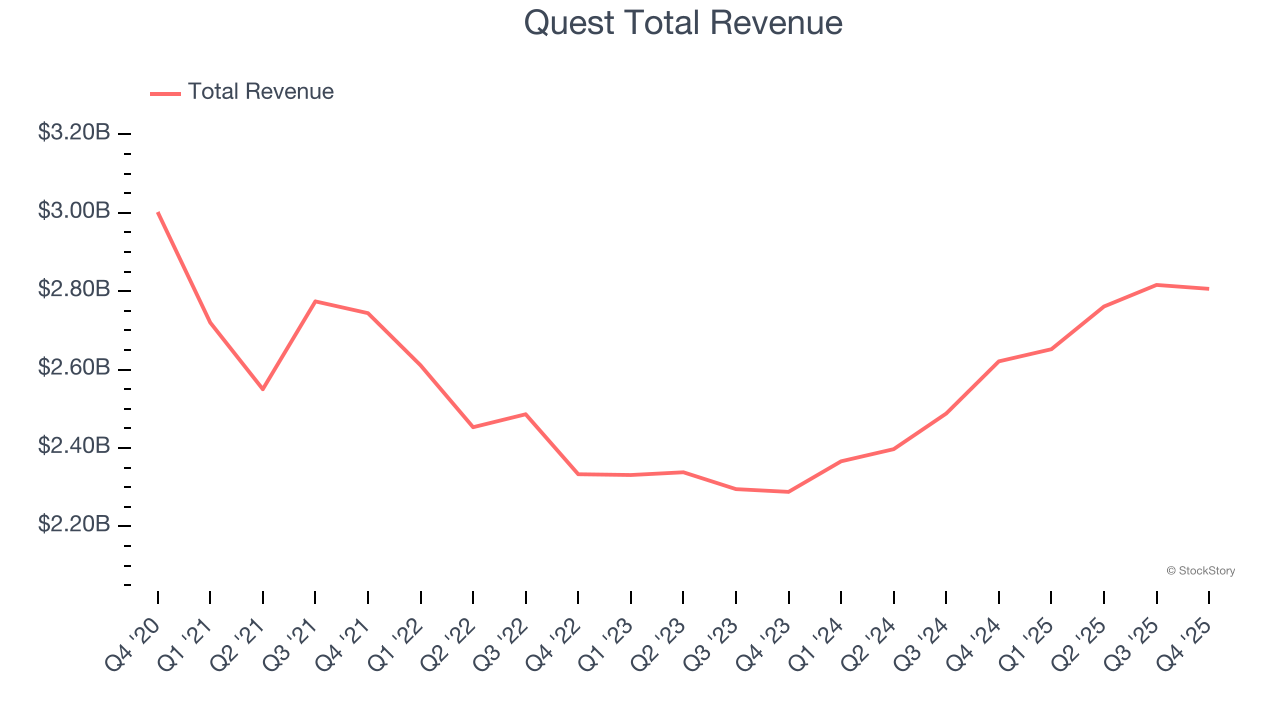

Quest (NYSE: DGX)

Processing approximately one-third of the adult U.S. population's lab tests annually, Quest Diagnostics (NYSE: DGX) provides laboratory testing and diagnostic information services to patients, physicians, hospitals, and other healthcare providers across the United States.

Quest reported revenues of $2.81 billion, up 7.1% year on year. This print exceeded analysts’ expectations by 1.9%. Overall, it was a very strong quarter for the company with full-year revenue guidance exceeding analysts’ expectations and a decent beat of analysts’ revenue estimates.

"We closed 2025 with a strong fourth quarter, and delivered double-digit growth in revenues and earnings per share for the full year," said Jim Davis, Chairman, CEO, and President.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $192.85.

Is now the time to buy Quest? Access our full analysis of the earnings results here, it’s free.

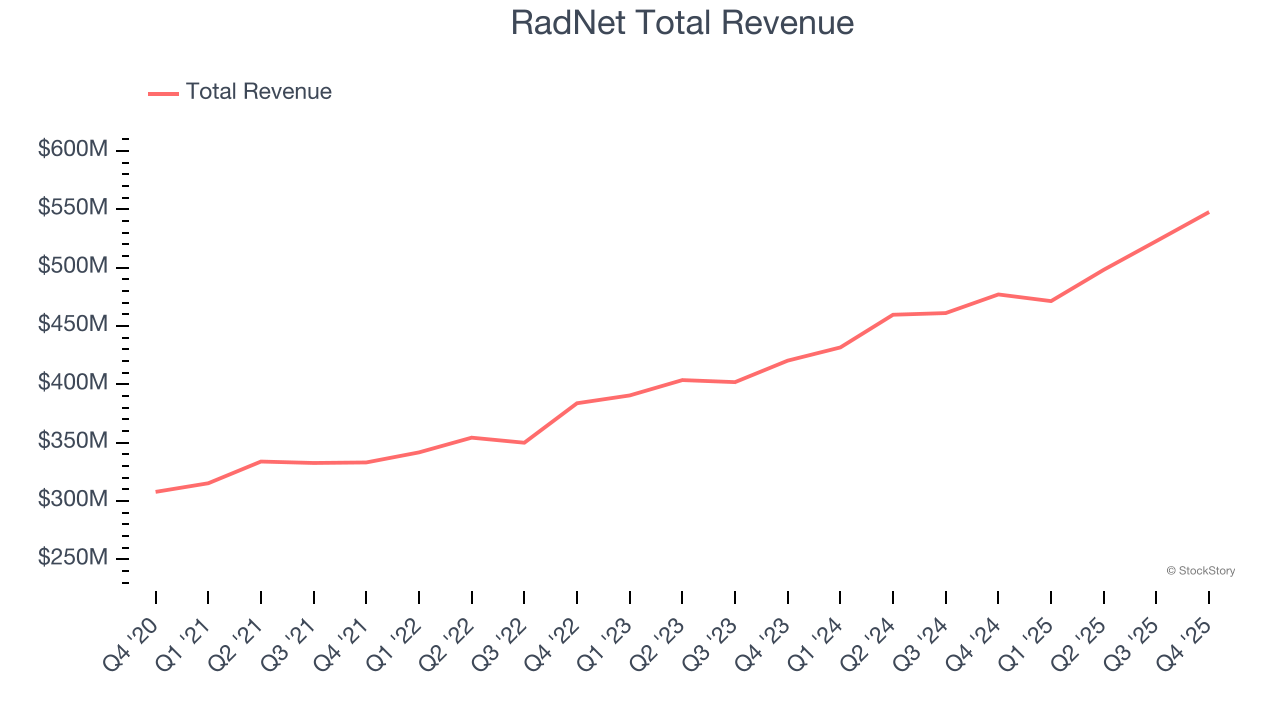

Best Q4: RadNet (NASDAQ: RDNT)

With over 350 imaging facilities across seven states and a growing artificial intelligence division, RadNet (NASDAQ: RDNT) operates a network of outpatient diagnostic imaging centers across the United States, offering services like MRI, CT scans, PET scans, mammography, and X-rays.

RadNet reported revenues of $547.7 million, up 14.8% year on year, outperforming analysts’ expectations by 5.8%. The business had an exceptional quarter with a solid beat of analysts’ revenue and EPS estimates.

RadNet scored the biggest analyst estimates beat among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 19.4% since reporting. It currently trades at $56.29.

Is now the time to buy RadNet? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Labcorp (NYSE: LH)

With over 600 million tests performed annually and involvement in 90% of FDA-approved drugs in 2023, Labcorp (NYSE: LH) provides laboratory testing services and drug development solutions to doctors, hospitals, pharmaceutical companies, and patients worldwide.

Labcorp reported revenues of $3.52 billion, up 5.6% year on year, falling short of analysts’ expectations by 1.4%. It was a mixed quarter as it posted a solid beat of analysts’ full-year EPS guidance estimates but a slight miss of analysts’ revenue estimates.

Labcorp delivered the highest full-year guidance raise but had the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 6.5% since the results and currently trades at $264.25.

Read our full analysis of Labcorp’s results here.

NeoGenomics (NASDAQ: NEO)

Operating a network of CAP-accredited and CLIA-certified laboratories across the United States and United Kingdom, NeoGenomics (NASDAQ: NEO) provides specialized cancer diagnostic testing services, including genetic analysis, molecular testing, and pathology consultation for oncologists and healthcare providers.

NeoGenomics reported revenues of $190.2 million, up 10.6% year on year. This print beat analysts’ expectations by 1%. It was a strong quarter as it also recorded a beat of analysts’ EPS estimates and an impressive beat of analysts’ full-year EPS guidance estimates.

The stock is down 30.7% since reporting and currently trades at $7.89.

Read our full, actionable report on NeoGenomics here, it’s free.

Guardant Health (NASDAQ: GH)

Pioneering the field of "liquid biopsy" with technology that can identify cancer-specific genetic mutations from a simple blood draw, Guardant Health (NASDAQ: GH) develops blood tests that detect and monitor cancer by analyzing tumor DNA in the bloodstream, helping doctors make treatment decisions without invasive biopsies.

Guardant Health reported revenues of $281.3 million, up 39.4% year on year. This result surpassed analysts’ expectations by 3.5%. Overall, it was a strong quarter as it also put up full-year revenue guidance beating analysts’ expectations and an impressive beat of analysts’ revenue estimates.

Guardant Health delivered the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is down 22.7% since reporting and currently trades at $82.20.

Read our full, actionable report on Guardant Health here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.