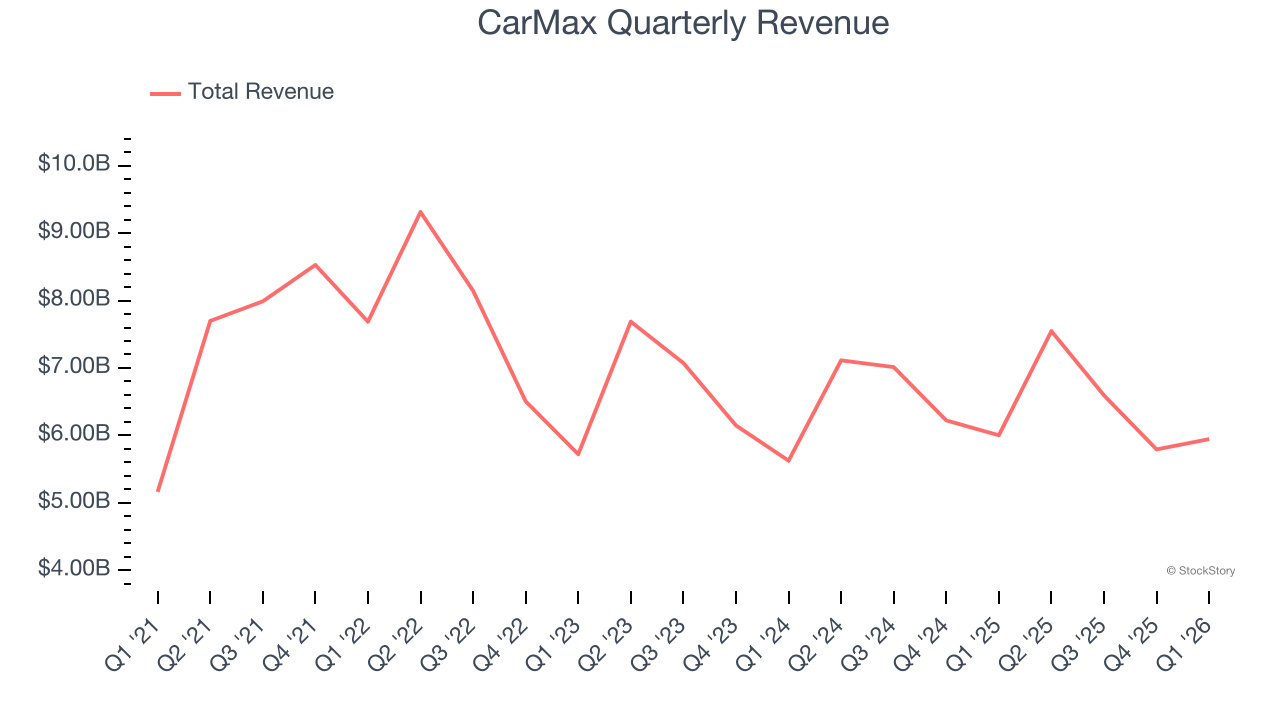

Used automotive vehicle retailer Carmax (NYSE: KMX) reported Q1 CY2026 results beating Wall Street’s revenue expectations, but sales were flat year on year at $5.95 billion. Its GAAP loss of $0.85 per share was significantly below analysts’ consensus estimates.

Is now the time to buy CarMax? Find out by accessing our full research report, it’s free.

CarMax (KMX) Q1 CY2026 Highlights:

- Revenue: $5.95 billion vs analyst estimates of $5.72 billion (flat year on year, 3.9% beat)

- EPS (GAAP): -$0.85 vs analyst estimates of $0.22 (significant miss due to $141 million one-time impairment charge)

- Adjusted EBITDA: $77.39 million vs analyst estimates of $145.6 million (1.3% margin, 46.8% miss)

- Operating Margin: -0.1%, down from 2.5% in the same quarter last year

- Free Cash Flow was -$687.3 million, down from $18.76 million in the same quarter last year

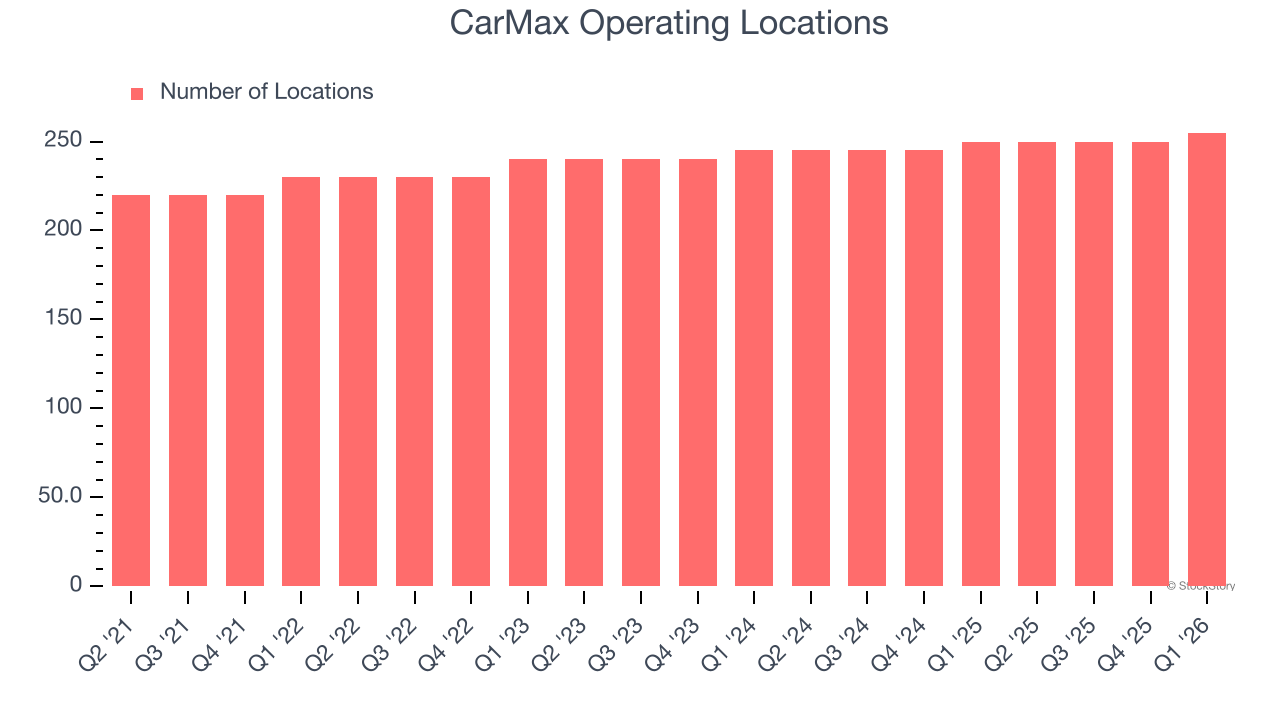

- Locations: 255 at quarter end, up from 250 in the same quarter last year

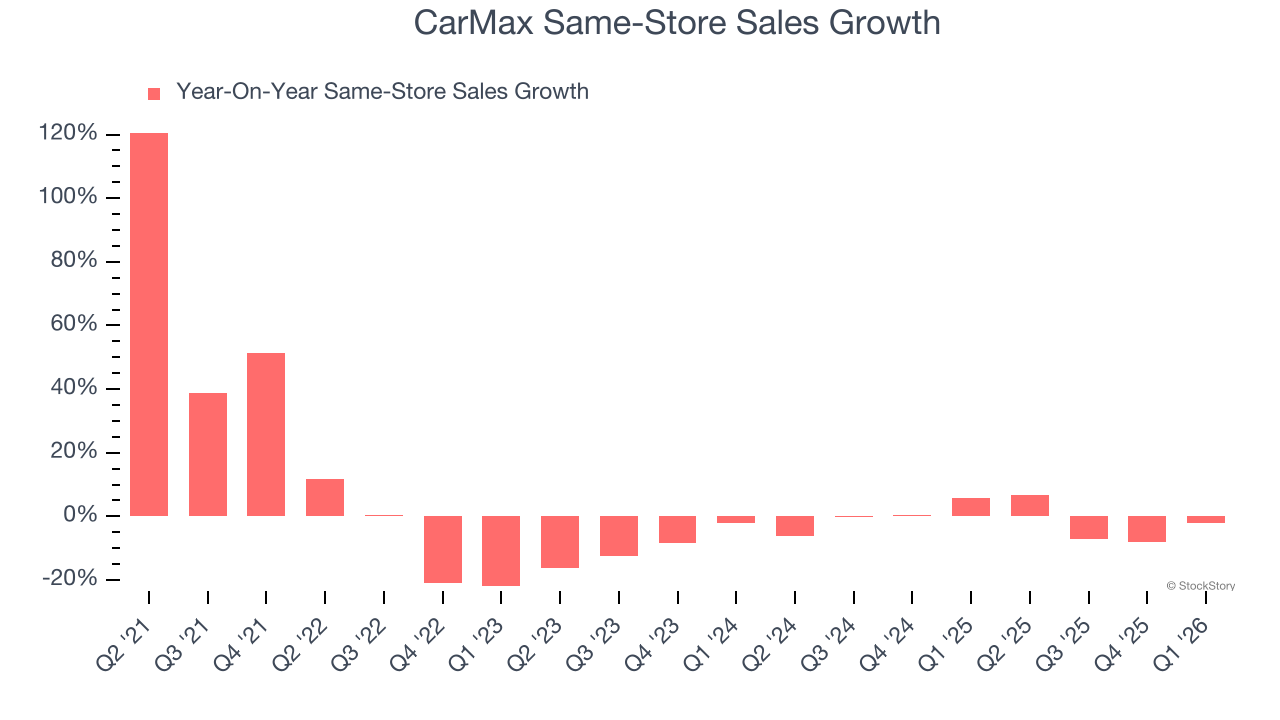

- Same-Store Sales fell 2% year on year (5.9% in the same quarter last year)

- Market Capitalization: $6.96 billion

“We are moving with urgency to improve execution, drive efficiencies, and sharpen our customer offering,” said Keith Barr, President and Chief Executive Officer.

Company Overview

Known for its transparent, customer-centric approach and wide selection of vehicles, Carmax (NYSE: KMX) is the largest automotive retailer in the United States.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $25.88 billion in revenue over the past 12 months, CarMax is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. To expand meaningfully, CarMax likely needs to tweak its prices or enter new markets.

As you can see below, CarMax’s demand was weak over the last three years. Its sales fell by 4.5% annually despite opening new stores. This implies its underperformance was driven by lower sales at existing, established locations.

This quarter, CarMax’s $5.95 billion of revenue was flat year on year but beat Wall Street’s estimates by 3.9%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

CarMax sported 255 locations in the latest quarter. Over the last two years, it has generally opened new stores, averaging 2.1% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

CarMax’s demand has been shrinking over the last two years as its same-store sales have averaged 1.3% annual declines. This performance is concerning - it shows CarMax artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, CarMax’s same-store sales fell by 2% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from CarMax’s Q1 Results

We enjoyed seeing CarMax beat analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed meaningfully. Overall, this quarter could have been better. The stock traded down 7.1% to $45.70 immediately following the results.

CarMax’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).