Archer-Daniels-Midland has had an impressive run over the past six months as its shares have beaten the S&P 500 by 10.8%. The stock now trades at $70.16, marking a 13.4% gain. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Archer-Daniels-Midland, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Archer-Daniels-Midland Not Exciting?

We’re happy investors have made money, but we're swiping left on Archer-Daniels-Midland for now. Here are three reasons there are better opportunities than ADM and a stock we'd rather own.

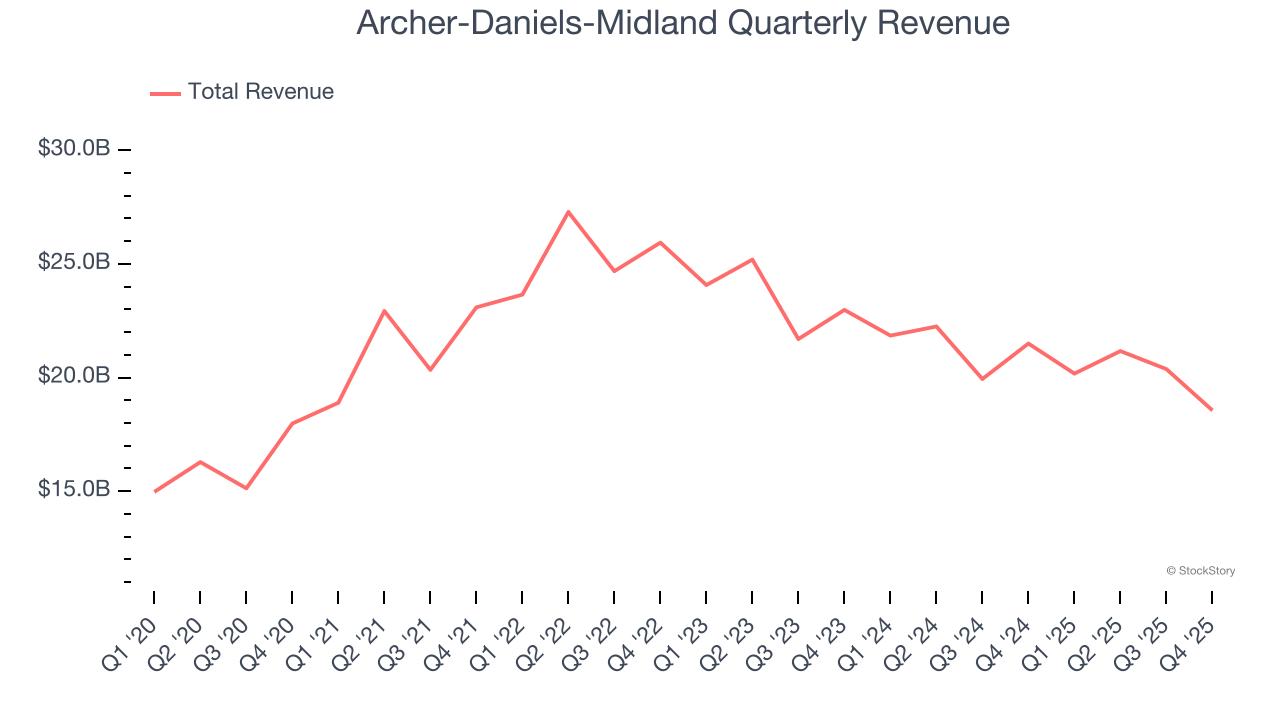

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Archer-Daniels-Midland’s demand was weak over the last three years as its sales fell at a 7.5% annual rate. This was below our standards and is a sign of lacking business quality.

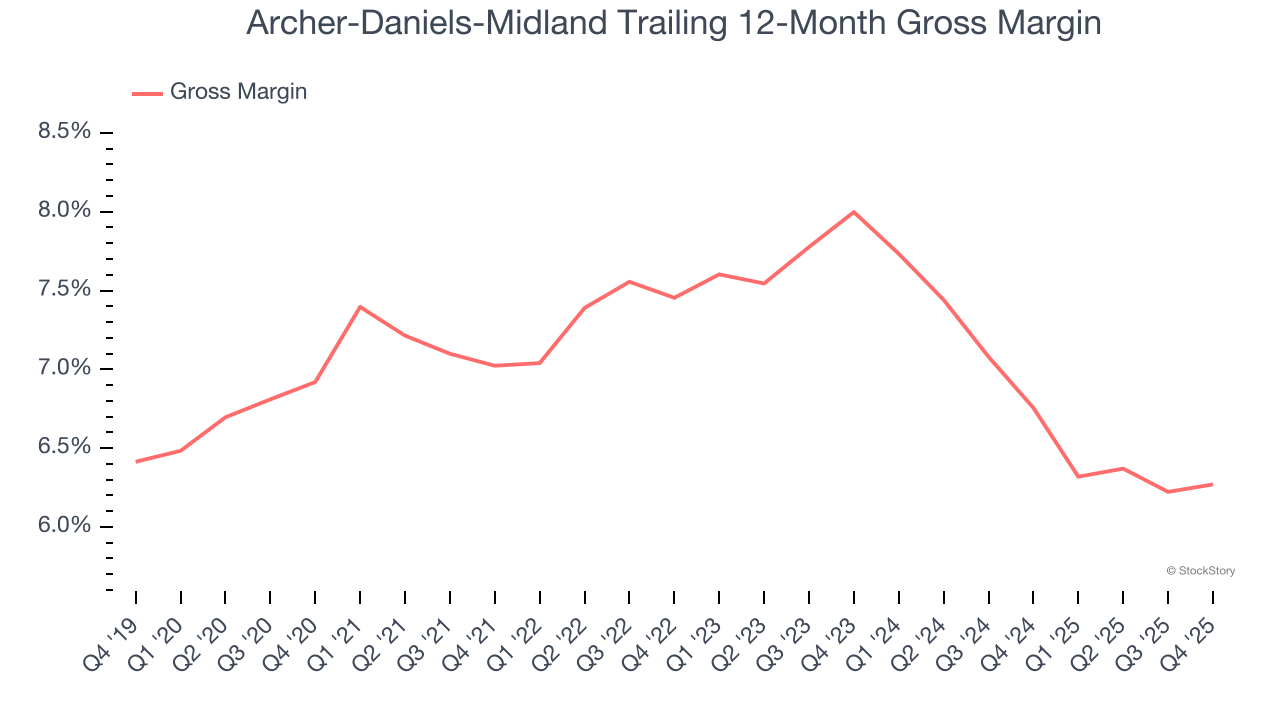

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

Archer-Daniels-Midland has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 6.5% gross margin over the last two years. That means Archer-Daniels-Midland paid its suppliers a lot of money ($93.48 for every $100 in revenue) to run its business.

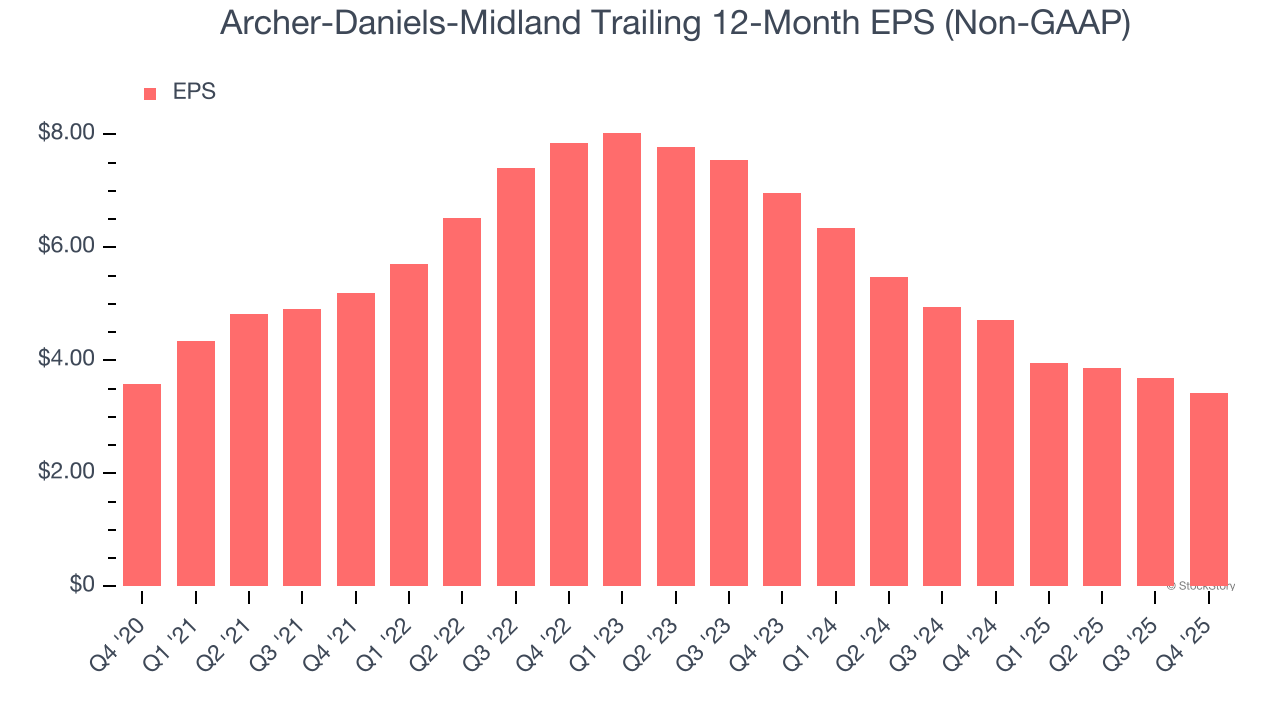

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Archer-Daniels-Midland, its EPS declined by 24.2% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Archer-Daniels-Midland’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 16.9× forward P/E (or $70.16 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Archer-Daniels-Midland

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.