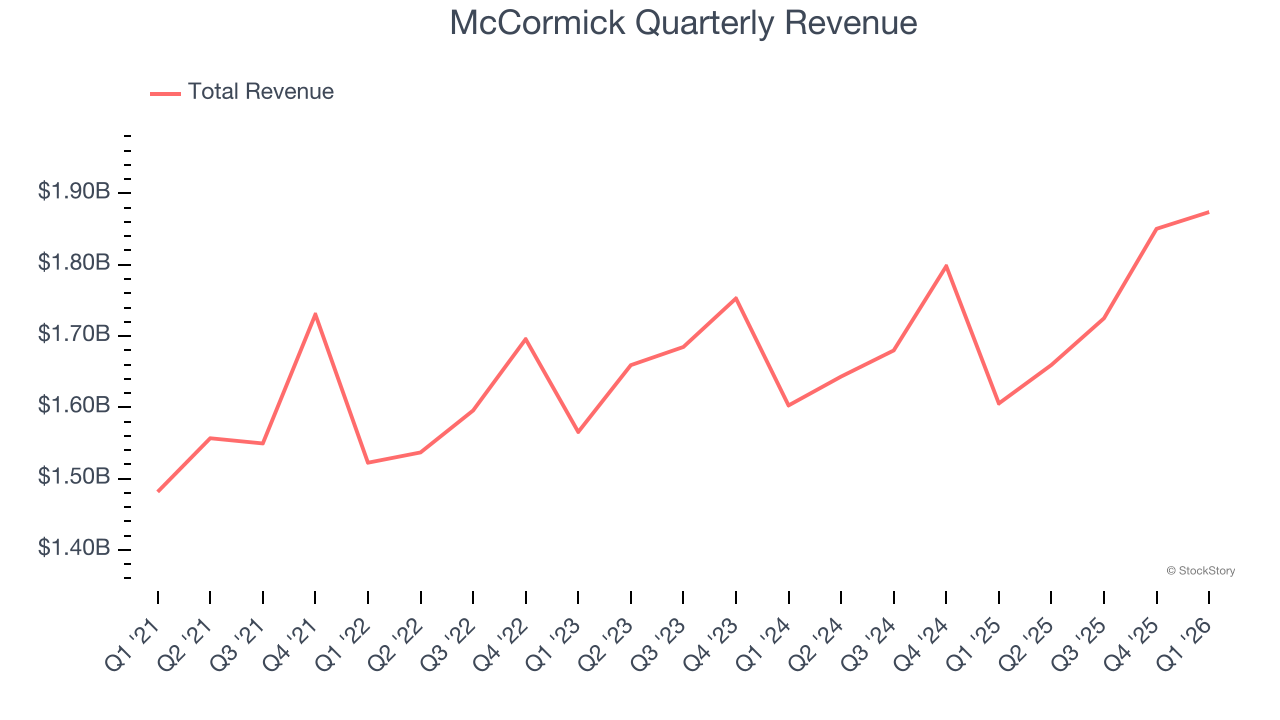

Food flavoring company McCormick (NYSE: MKC) announced better-than-expected revenue in Q1 CY2026, with sales up 16.7% year on year to $1.87 billion. Its non-GAAP profit of $0.66 per share was 10.9% above analysts’ consensus estimates.

Is now the time to buy McCormick? Find out by accessing our full research report, it’s free.

McCormick (MKC) Q1 CY2026 Highlights:

- Revenue: $1.87 billion vs analyst estimates of $1.78 billion (16.7% year-on-year growth, 5.1% beat)

- Adjusted EPS: $0.66 vs analyst estimates of $0.59 (10.9% beat)

- Management reiterated its full-year Adjusted EPS guidance of $3.09 at the midpoint

- Operating Margin: 12.1%, down from 14% in the same quarter last year

- Free Cash Flow Margin: 1%, down from 4.9% in the same quarter last year

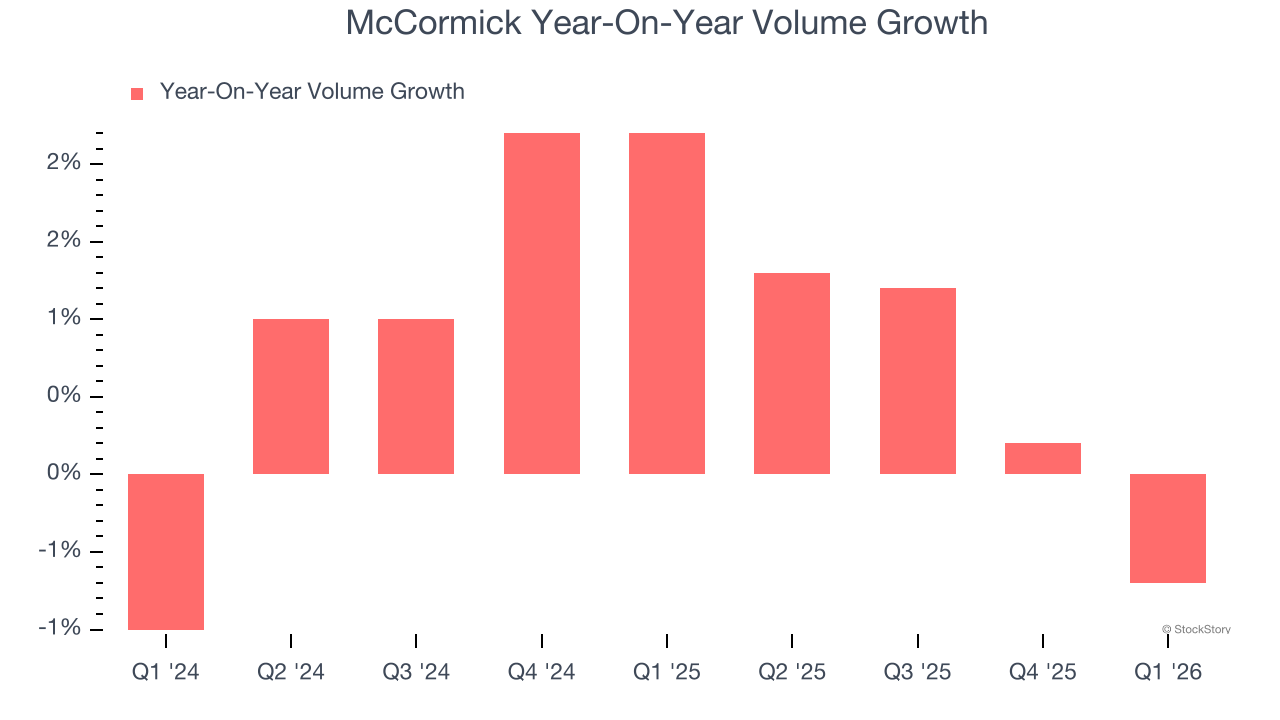

- Sales Volumes were flat year on year (2.2% in the same quarter last year)

- Market Capitalization: $14.43 billion

Brendan M. Foley, Chairman, President, and CEO, stated, "We are pleased to begin the year with first quarter results that demonstrate the strength and resilience of our business. We delivered strong growth in sales, adjusted operating income, and adjusted earnings per share, supported by the McCormick de Mexico acquisition and organic growth across both Consumer and Flavor Solutions. Strong sales, acquisition accretion, and disciplined cost management enabled margin expansion as we continued to invest for future growth."

Company Overview

The classic red Heinz ketchup bottle’s competitor, McCormick (NYSE: MKC) sells food-flavoring products like condiments, spices, and seasoning mixes.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $7.11 billion in revenue over the past 12 months, McCormick is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. For McCormick to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, McCormick grew its sales at a sluggish 3.6% compounded annual growth rate over the last three years, but to its credit, consumers bought more of its products.

This quarter, McCormick reported year-on-year revenue growth of 16.7%, and its $1.87 billion of revenue exceeded Wall Street’s estimates by 5.1%.

Looking ahead, sell-side analysts expect revenue to grow 11.8% over the next 12 months, an acceleration versus the last three years. This projection is commendable and suggests its newer products will fuel better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

McCormick’s average quarterly volume growth was a healthy 1% over the last two years. This is pleasing because it shows consumers are purchasing more of its products.

In McCormick’s Q1 2026, year on year sales volumes were flat. This result was a meaningful deceleration from its historical levels. We’ll be watching closely to see if McCormick can reaccelerate demand for its products.

Key Takeaways from McCormick’s Q1 Results

We enjoyed seeing McCormick beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 5.5% to $56.66 immediately following the results.

Is McCormick an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).