F.N.B. Corporation currently trades at $16.26 per share and has shown little upside over the past six months, posting a small loss of 1.1%.

Is there a buying opportunity in F.N.B. Corporation, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is F.N.B. Corporation Not Exciting?

We're sitting this one out for now. Here are three reasons you should be careful with FNB and a stock we'd rather own.

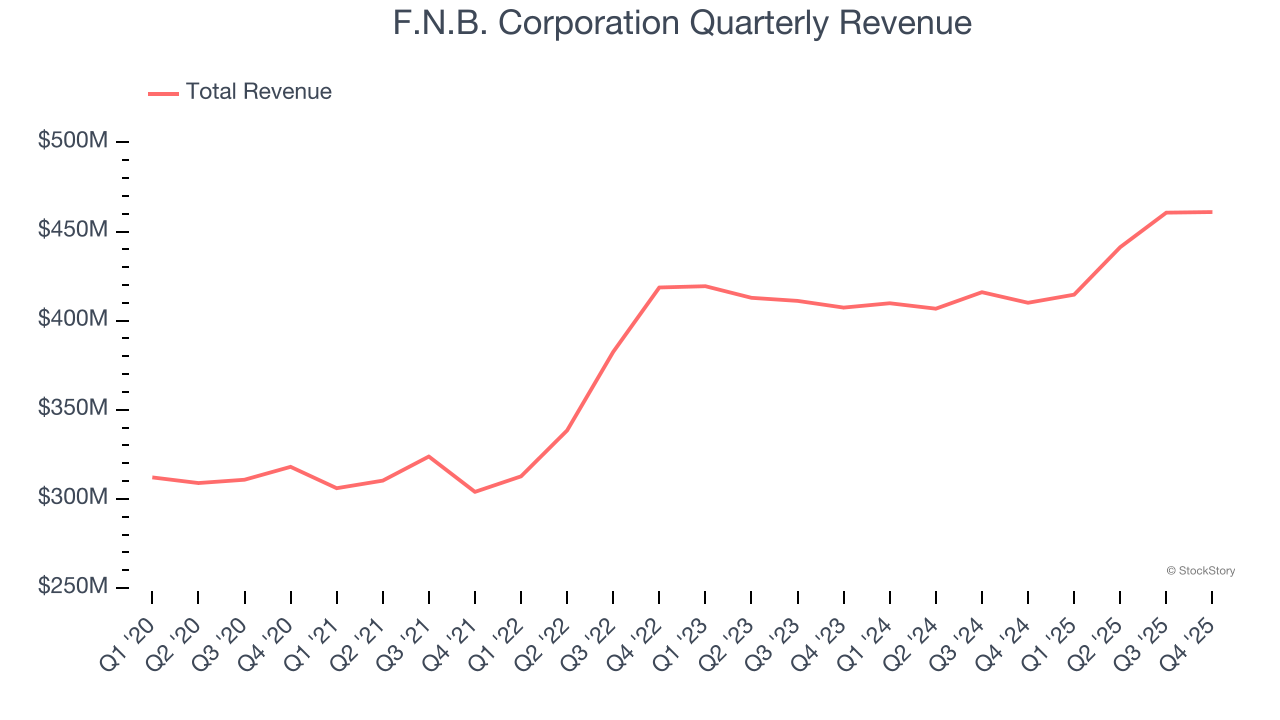

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Regrettably, F.N.B. Corporation’s revenue grew at a tepid 7.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector.

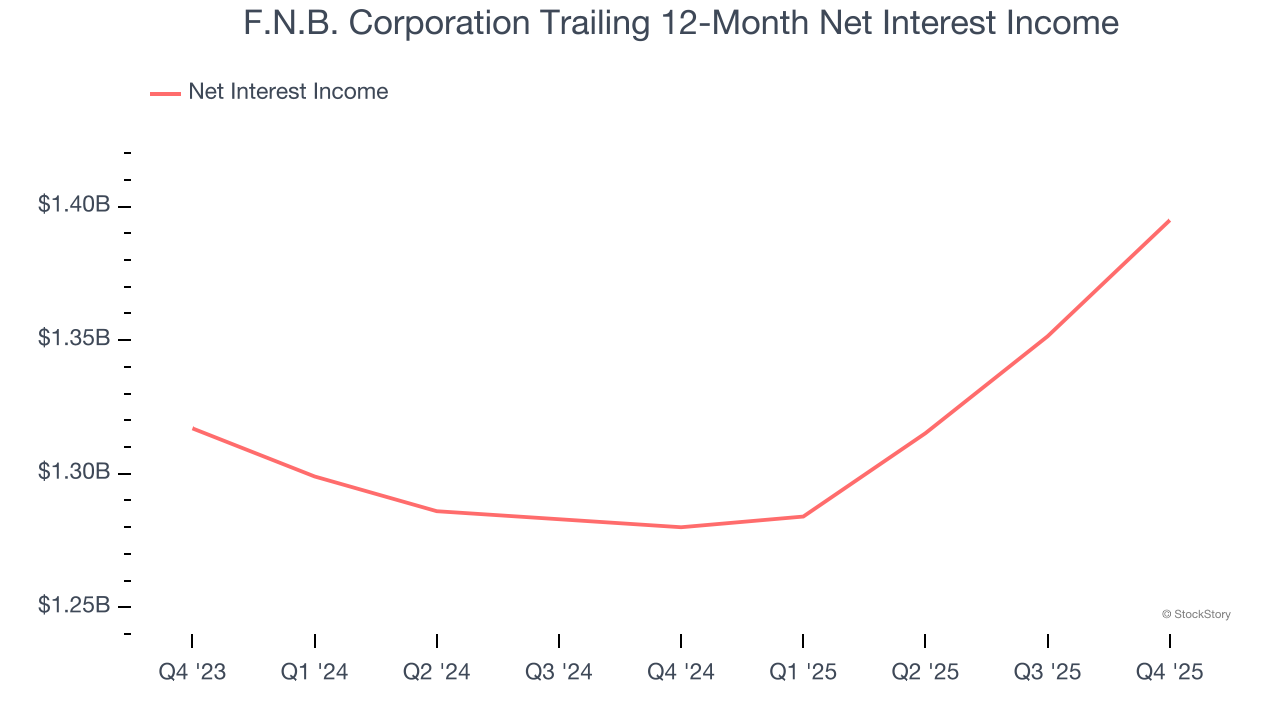

2. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

F.N.B. Corporation’s net interest income has grown at a 8.6% annualized rate over the last five years, slightly worse than the broader banking industry.

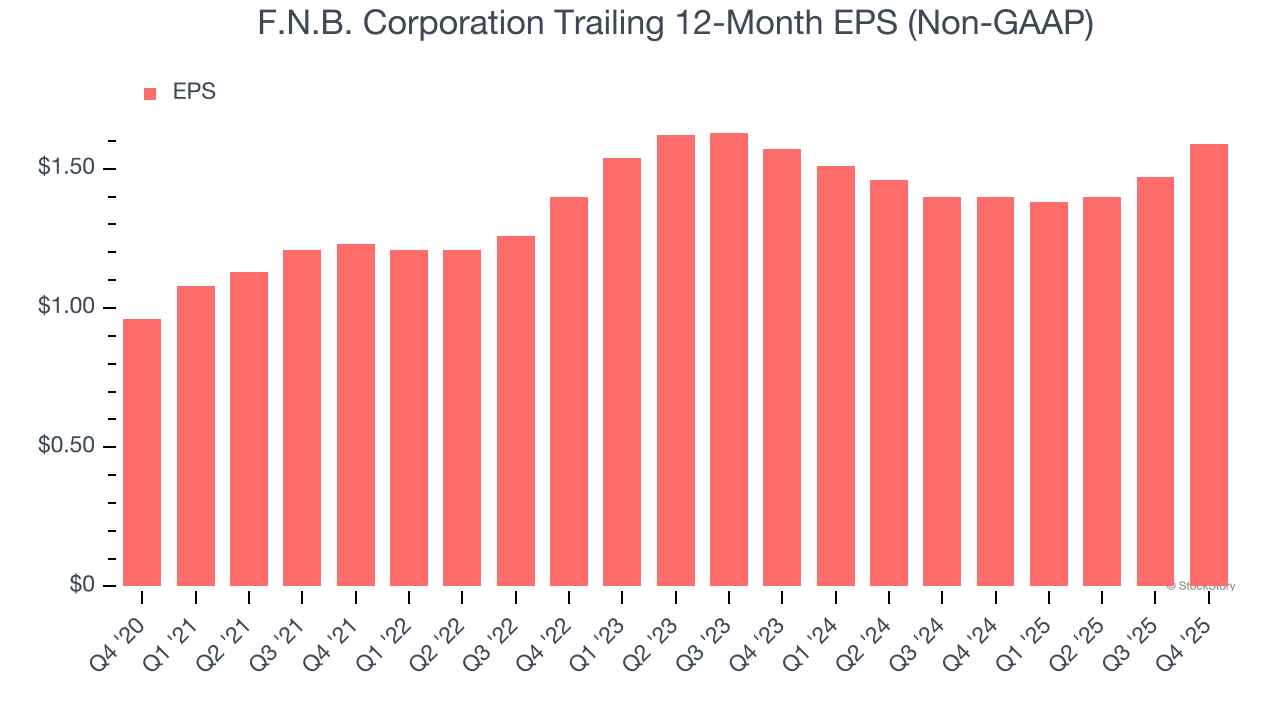

3. EPS Growth Has Stalled Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

F.N.B. Corporation’s flat EPS over the last two years was worse than its 3.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

F.N.B. Corporation isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 0.8× forward P/B (or $16.26 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.