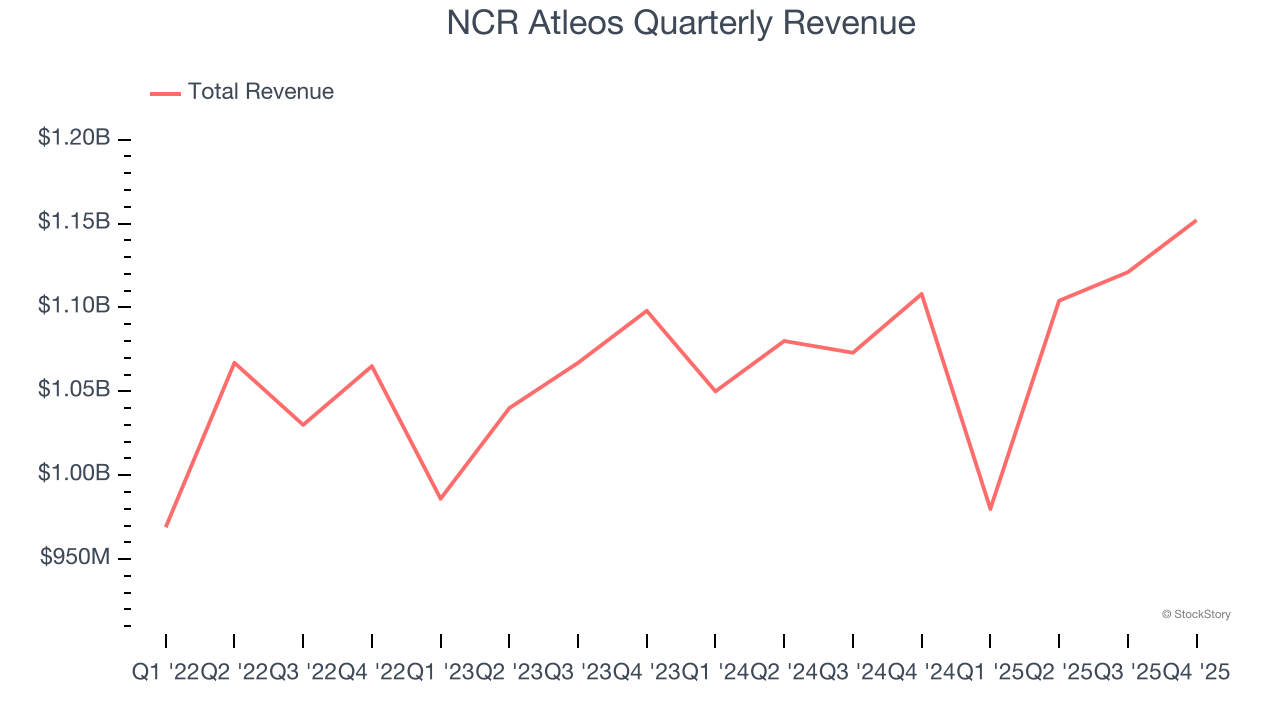

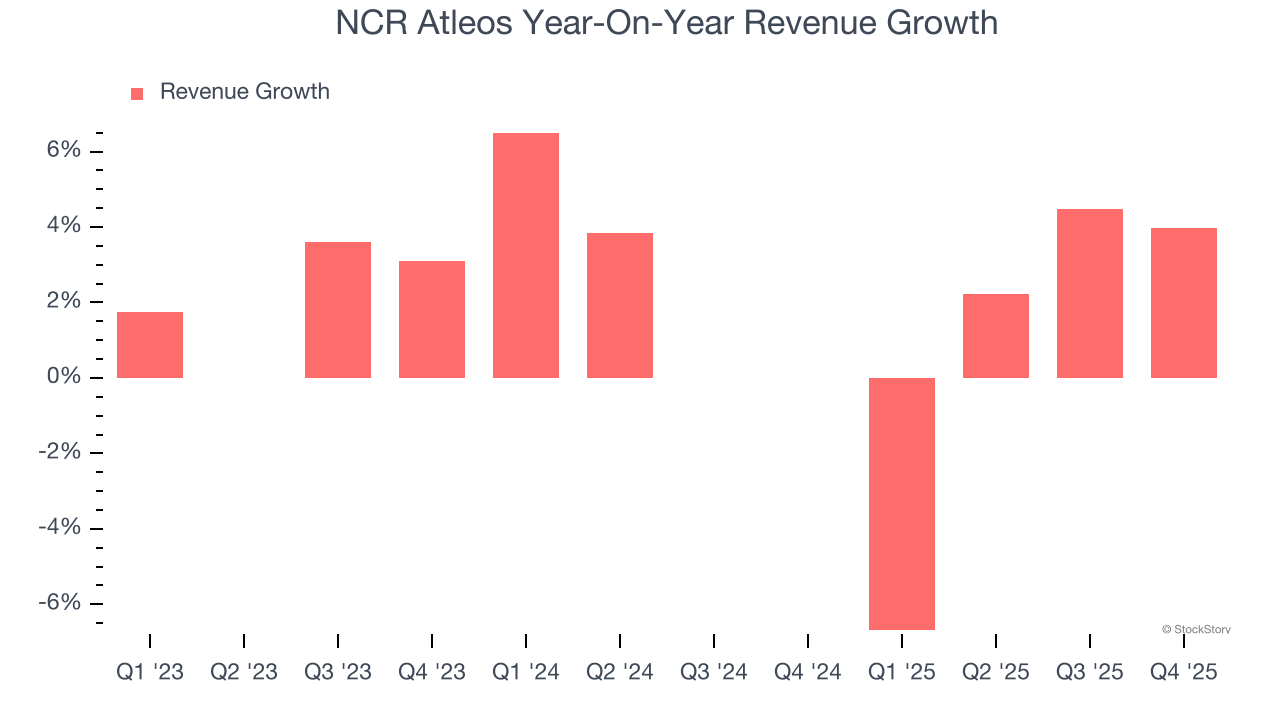

Financial technology company NCR Atleos (NYSE: NATL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 4% year on year to $1.15 billion. Its GAAP profit of $1.09 per share was 11.2% above analysts’ consensus estimates.

Is now the time to buy NCR Atleos? Find out by accessing our full research report, it’s free.

NCR Atleos (NATL) Q4 CY2025 Highlights:

- Revenue: $1.15 billion vs analyst estimates of $1.15 billion (4% year-on-year growth, in line)

- Pre-tax Profit: $77 million (6.7% margin)

- EPS (GAAP): $1.09 vs analyst estimates of $0.98 (11.2% beat)

- Market Capitalization: $3.00 billion

Company Overview

Spun off from NCR Voyix in 2023 to focus exclusively on self-service banking technology, NCR Atleos (NYSE: NATL) provides self-directed banking solutions including ATM and interactive teller machine technology, software, services, and a surcharge-free ATM network for financial institutions and retailers.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, NCR Atleos struggled to consistently increase demand as its $4.36 billion of revenue for the trailing 12 months was close to its revenue three years ago. This wasn’t a great result, but there are still things to like about NCR Atleos.

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. NCR Atleos’s annualized revenue growth of 2% over the last two years is above its three-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, NCR Atleos grew its revenue by 4% year on year, and its $1.15 billion of revenue was in line with Wall Street’s estimates.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Key Takeaways from NCR Atleos’s Q4 Results

It was good to see NCR Atleos beat analysts’ EPS expectations this quarter. Overall, this print had some key positives. The stock traded up 9.2% to $45.74 immediately following the results.

Sure, NCR Atleos had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).