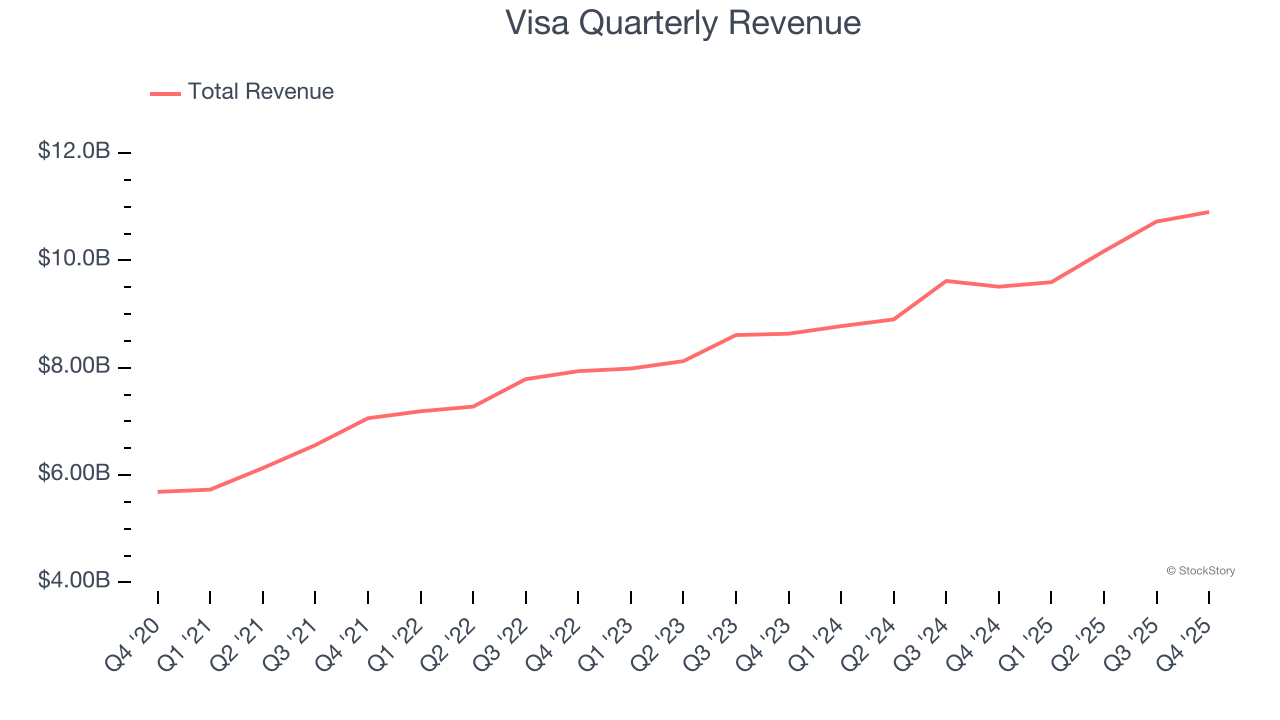

Global payments technology company Visa (NYSE: V) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 14.6% year on year to $10.9 billion. Its non-GAAP profit of $3.17 per share was 0.9% above analysts’ consensus estimates.

Is now the time to buy Visa? Find out by accessing our full research report, it’s free.

Visa (V) Q4 CY2025 Highlights:

- Net Interest Income: $183 million

- Revenue: $10.9 billion vs analyst estimates of $10.69 billion (14.6% year-on-year growth, 2% beat)

- Pre-tax Profit: $6.73 billion (61.7% margin)

- Adjusted EPS: $3.17 vs analyst estimates of $3.14 (0.9% beat)

- Market Capitalization: $625.3 billion

Company Overview

Processing over 829 million transactions daily and connecting billions of cards to 150 million merchant locations worldwide, Visa (NYSE: V) operates one of the world's largest electronic payments networks, facilitating secure money movement across more than 200 countries through its VisaNet processing platform.

Revenue Growth

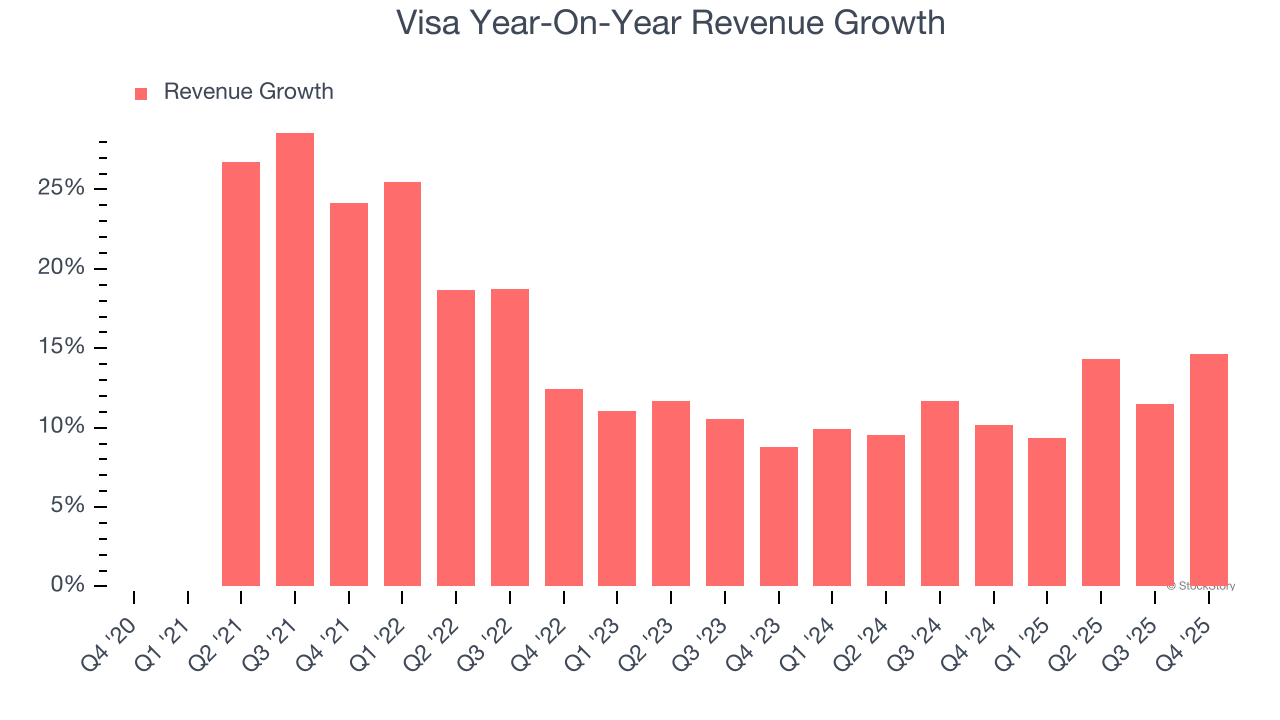

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Visa grew its revenue at a solid 14% compounded annual growth rate. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Visa’s annualized revenue growth of 11.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Visa reported year-on-year revenue growth of 14.6%, and its $10.9 billion of revenue exceeded Wall Street’s estimates by 2%.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Key Takeaways from Visa’s Q4 Results

While Visa beat on revenue and EPS, the magnitude of the beats was quite small. Investors were likely hoping for more, and shares traded down 2% to $325.93 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).