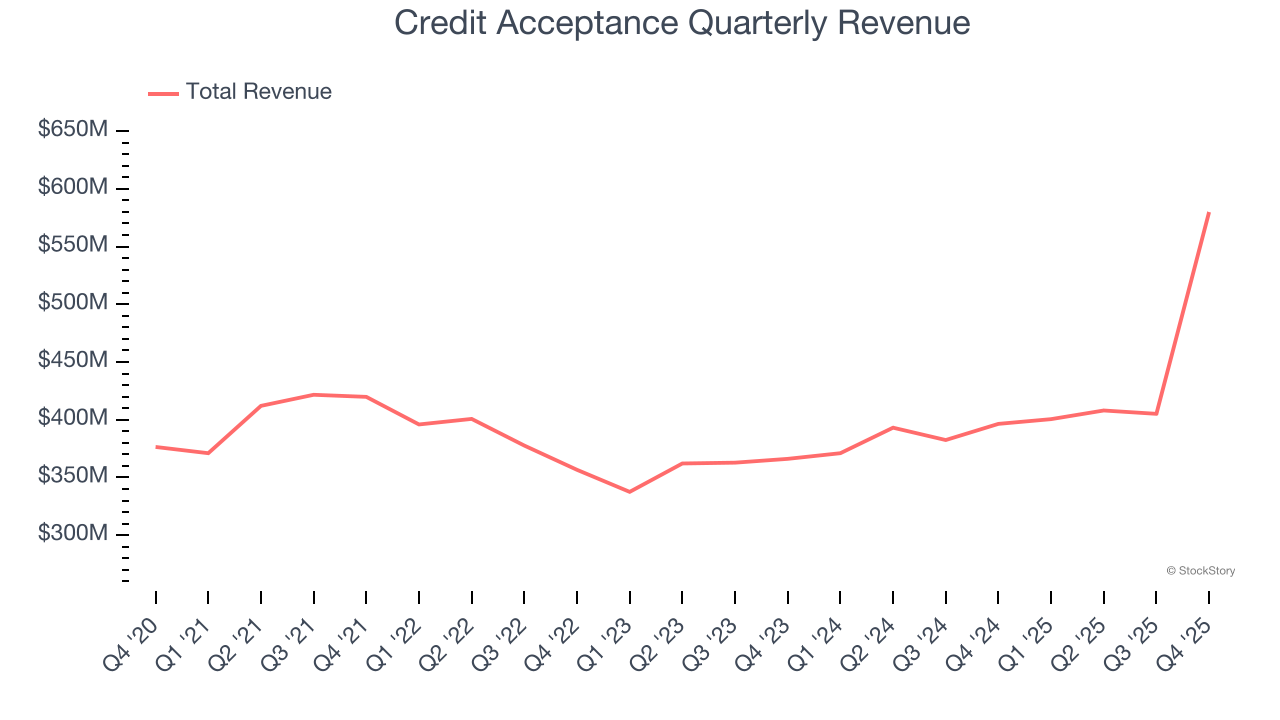

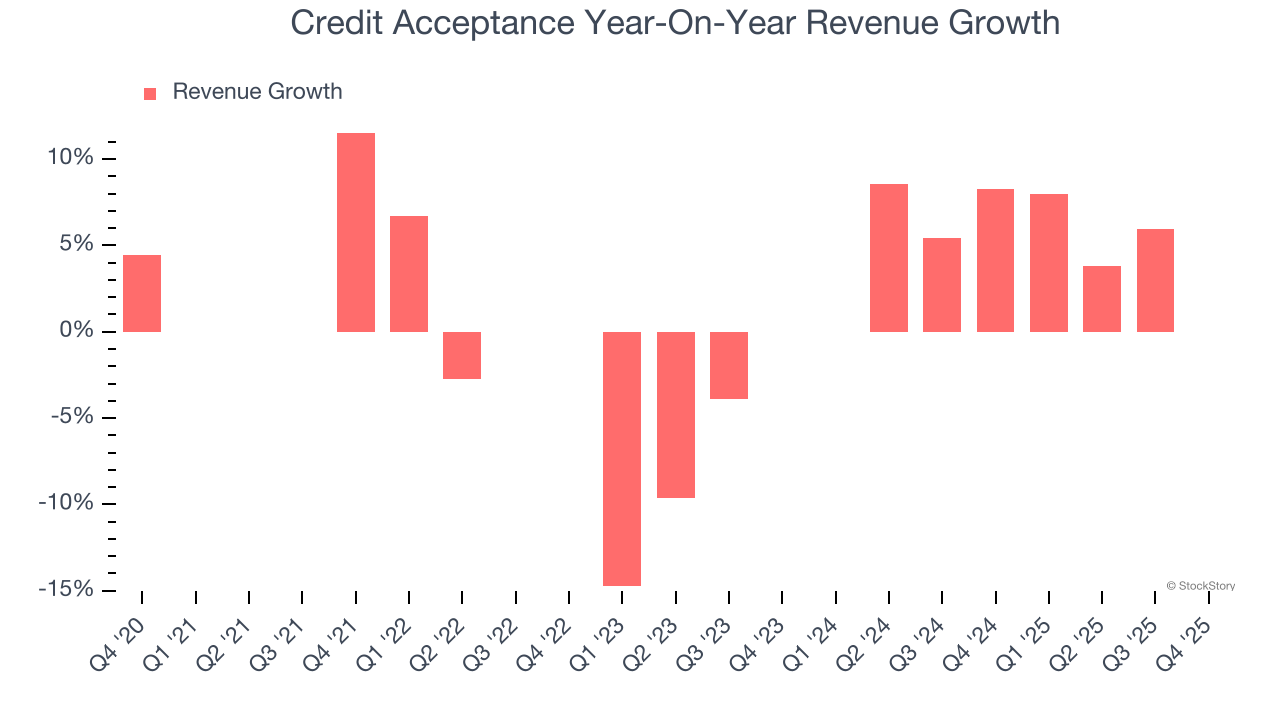

Auto financing company Credit Acceptance (NASDAQ: CACC) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 46.3% year on year to $579.9 million. Its non-GAAP profit of $11.35 per share was 15.2% above analysts’ consensus estimates.

Is now the time to buy Credit Acceptance? Find out by accessing our full research report, it’s free.

Credit Acceptance (CACC) Q4 CY2025 Highlights:

- Revenue: $579.9 million vs analyst estimates of $464.5 million (46.3% year-on-year growth, 24.8% beat)

- Pre-tax Profit: $157 million (27.1% margin)

- Adjusted EPS: $11.35 vs analyst estimates of $9.85 (15.2% beat)

- Market Capitalization: $4.78 billion

“We are pleased to announce sequential growth in our financial results in the fourth quarter of 2025,” said Vinayak Hegde, CEO of Credit Acceptance.

Company Overview

Founded in 1972 by Donald Foss to serve customers overlooked by traditional lenders, Credit Acceptance (NASDAQ: CACC) provides auto financing solutions that enable car dealers to sell vehicles to consumers with limited or impaired credit histories.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Credit Acceptance’s 4.9% annualized revenue growth over the last five years was tepid. This was below our standard for the financials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Credit Acceptance’s annualized revenue growth of 12% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Credit Acceptance reported magnificent year-on-year revenue growth of 46.3%, and its $579.9 million of revenue beat Wall Street’s estimates by 24.8%.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Key Takeaways from Credit Acceptance’s Q4 Results

We were impressed by how significantly Credit Acceptance blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $450.24 immediately following the results.

So should you invest in Credit Acceptance right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).