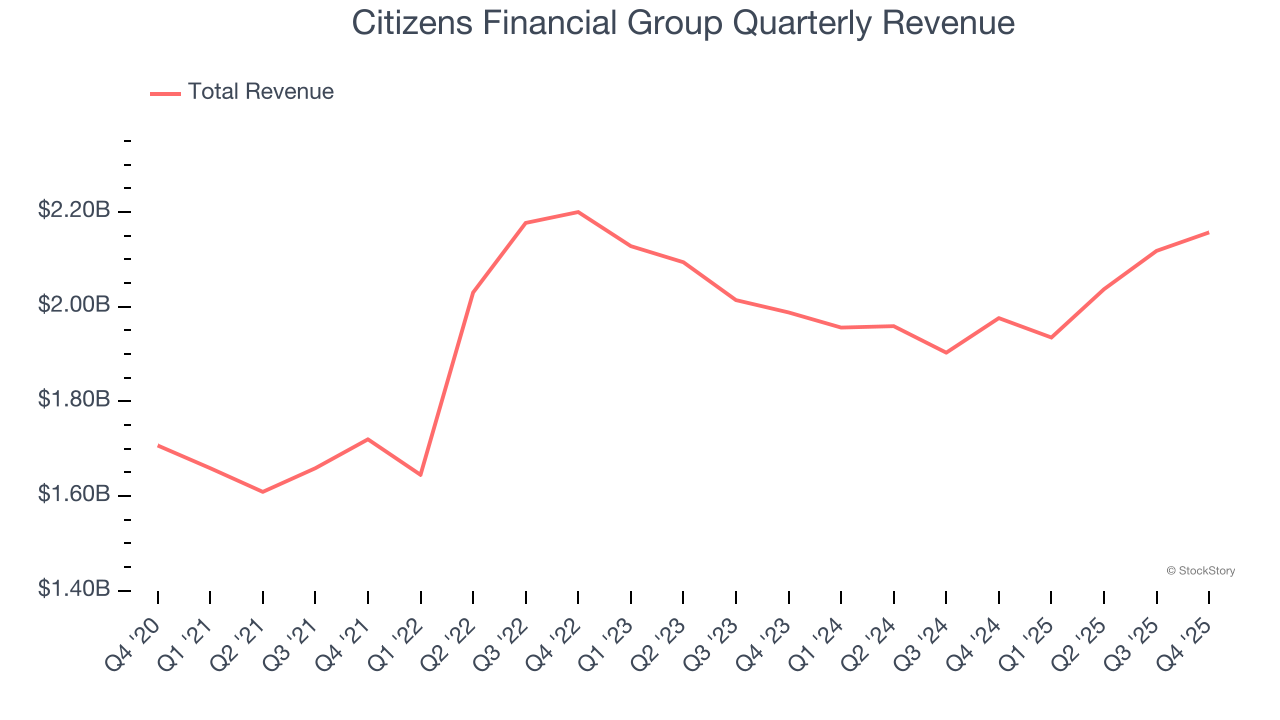

Regional banking company Citizens Financial Group (NYSE: CFG) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 9.2% year on year to $2.16 billion. Its non-GAAP profit of $1.13 per share was 2.2% above analysts’ consensus estimates.

Is now the time to buy Citizens Financial Group? Find out by accessing our full research report, it’s free.

Citizens Financial Group (CFG) Q4 CY2025 Highlights:

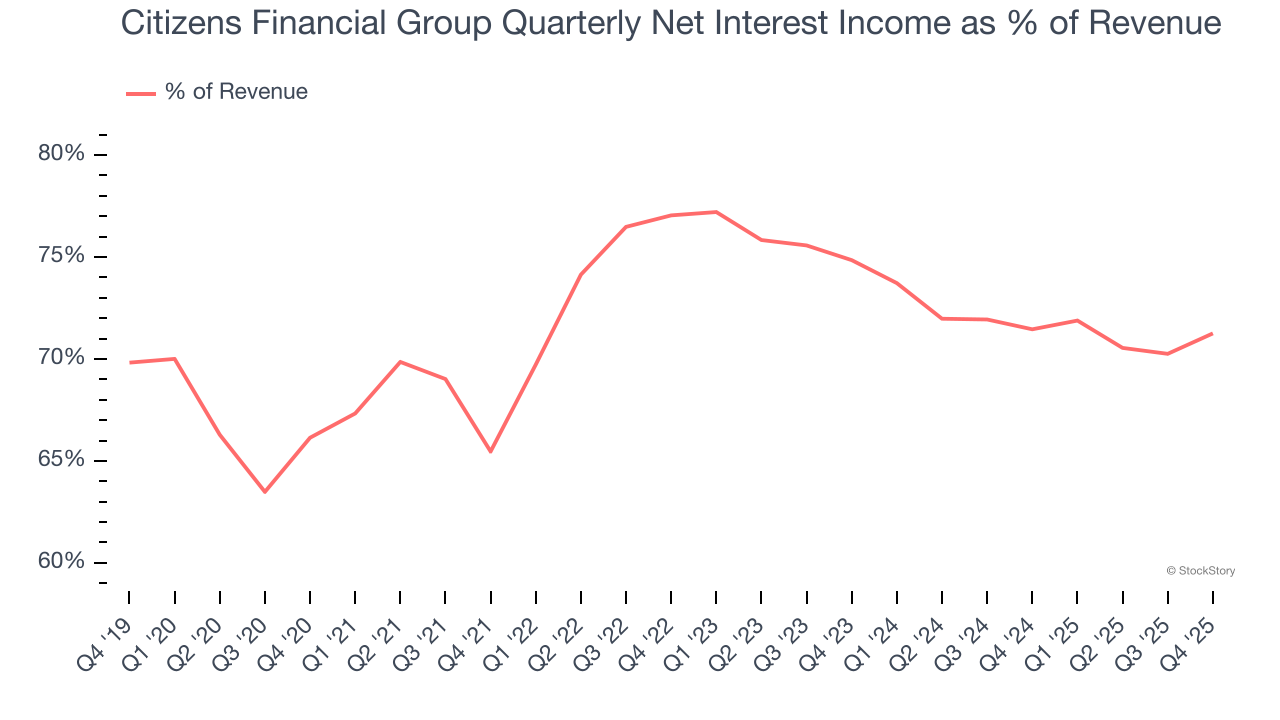

- Net Interest Income: $1.54 billion vs analyst estimates of $1.53 billion (8.9% year-on-year growth, in line)

- Net Interest Margin: 3.1% vs analyst estimates of 3.1% (in line)

- Revenue: $2.16 billion vs analyst estimates of $2.14 billion (9.2% year-on-year growth, 0.7% beat)

- Efficiency Ratio: 62.2% vs analyst estimates of 62.3% (7 basis point beat)

- Adjusted EPS: $1.13 vs analyst estimates of $1.11 (2.2% beat)

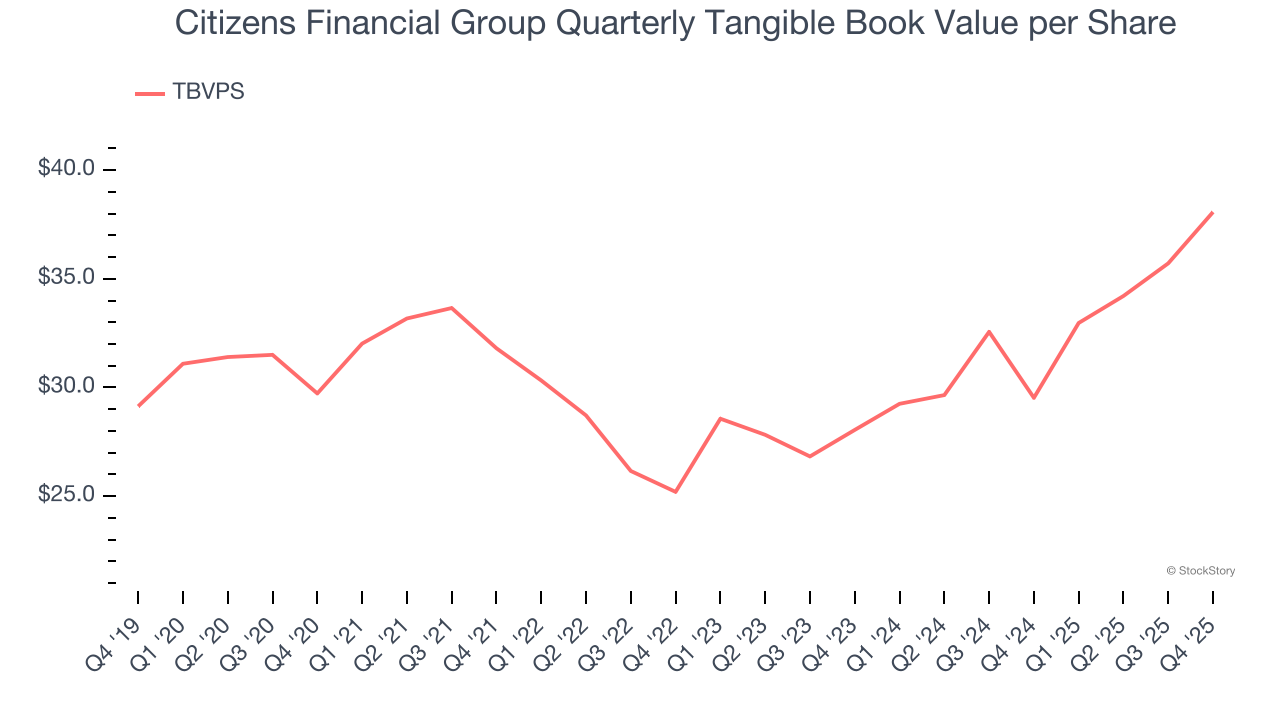

- Tangible Book Value per Share: $38.07 vs analyst estimates of $37.79 (28.9% year-on-year growth, 0.7% beat)

- Market Capitalization: $25.69 billion

Company Overview

Tracing its roots back to 1828 as a community-focused institution, Citizens Financial Group (NYSE: CFG) is a regional bank that provides retail and commercial banking services to individuals, small businesses, and large corporations across 14 states.

Sales Growth

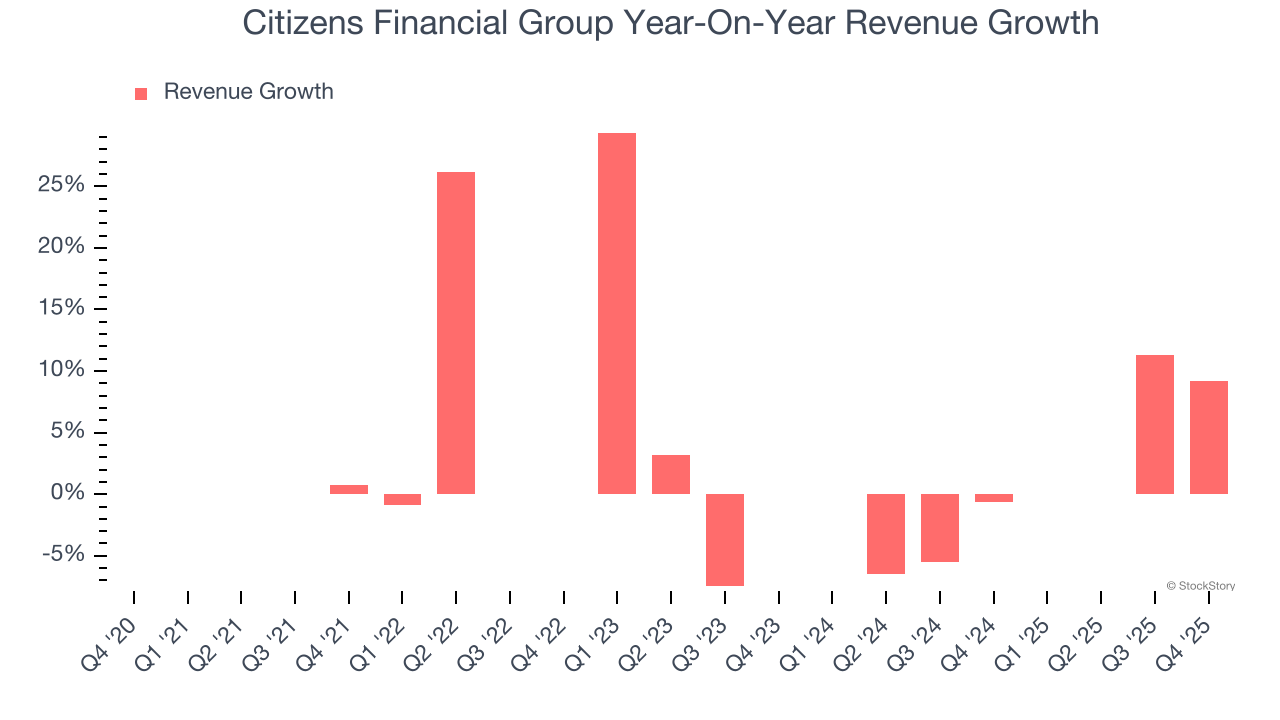

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Over the last five years, Citizens Financial Group grew its revenue at a sluggish 3.6% compounded annual growth rate. This was below our standard for the banking sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Citizens Financial Group’s recent performance shows its demand has slowed as its revenue was flat over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Citizens Financial Group reported year-on-year revenue growth of 9.2%, and its $2.16 billion of revenue exceeded Wall Street’s estimates by 0.7%.

Net interest income made up 72.3% of the company’s total revenue during the last five years, meaning lending operations are Citizens Financial Group’s largest source of revenue.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Tangible Book Value Per Share (TBVPS)

Banks operate as balance sheet businesses, with profits generated through borrowing and lending activities. Valuations reflect this reality, emphasizing balance sheet strength and long-term book value compounding ability.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

Citizens Financial Group’s TBVPS grew at a decent 5.1% annual clip over the last five years. TBVPS growth has accelerated recently, growing by 16.5% annually over the last two years from $28.05 to $38.07 per share.

Over the next 12 months, Consensus estimates call for Citizens Financial Group’s TBVPS to grow by 6.5% to $40.53, lousy growth rate.

Key Takeaways from Citizens Financial Group’s Q4 Results

It was good to see Citizens Financial Group narrowly top analysts’ tangible book value per share expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates, which carried through to a slight EPS beat. Overall, this quarter was fine, but the stock traded down 1.3% to $59.05 immediately after reporting.

So do we think Citizens Financial Group is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).