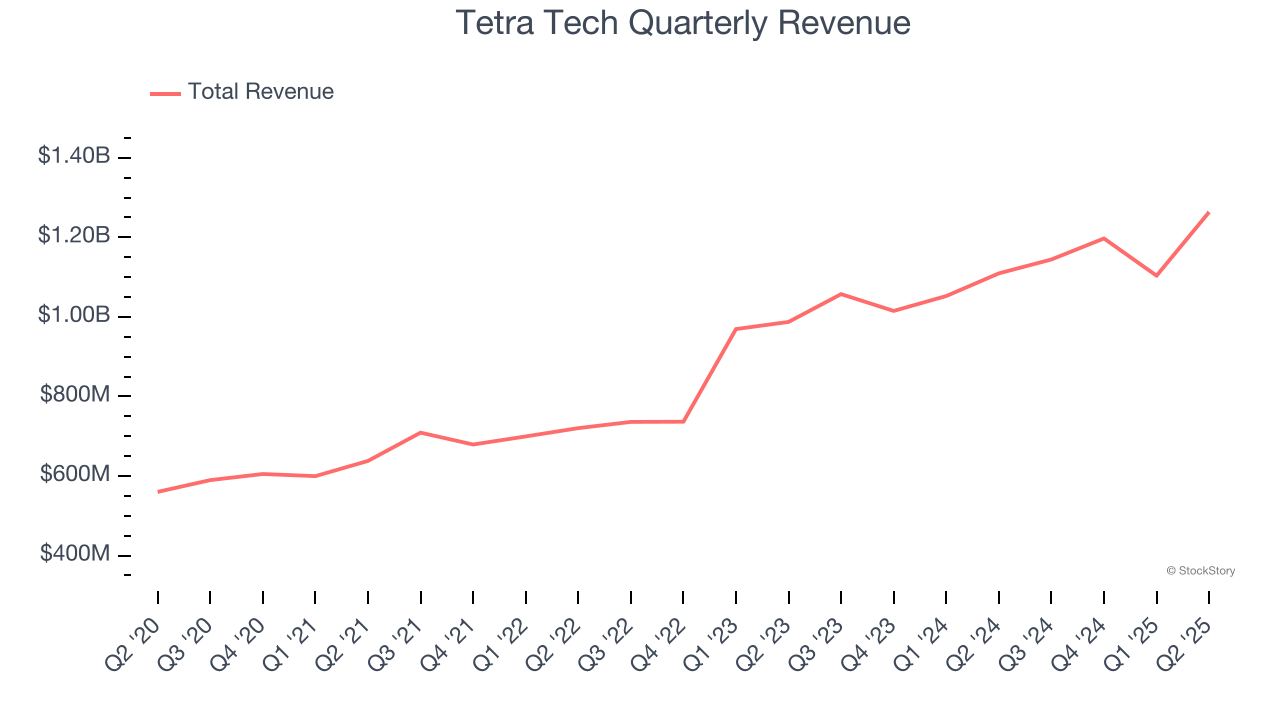

Environmental engineering firm Tetra Tech (NASDAQ: TTEK) announced better-than-expected revenue in Q2 CY2025, with sales up 13.9% year on year to $1.26 billion. On the other hand, next quarter’s revenue guidance of $1.05 billion was less impressive, coming in 6.7% below analysts’ estimates. Its GAAP profit of $0.43 per share was 17% above analysts’ consensus estimates.

Is now the time to buy Tetra Tech? Find out by accessing our full research report, it’s free.

Tetra Tech (TTEK) Q2 CY2025 Highlights:

- Revenue: $1.26 billion vs analyst estimates of $1.13 billion (13.9% year-on-year growth, 11.9% beat)

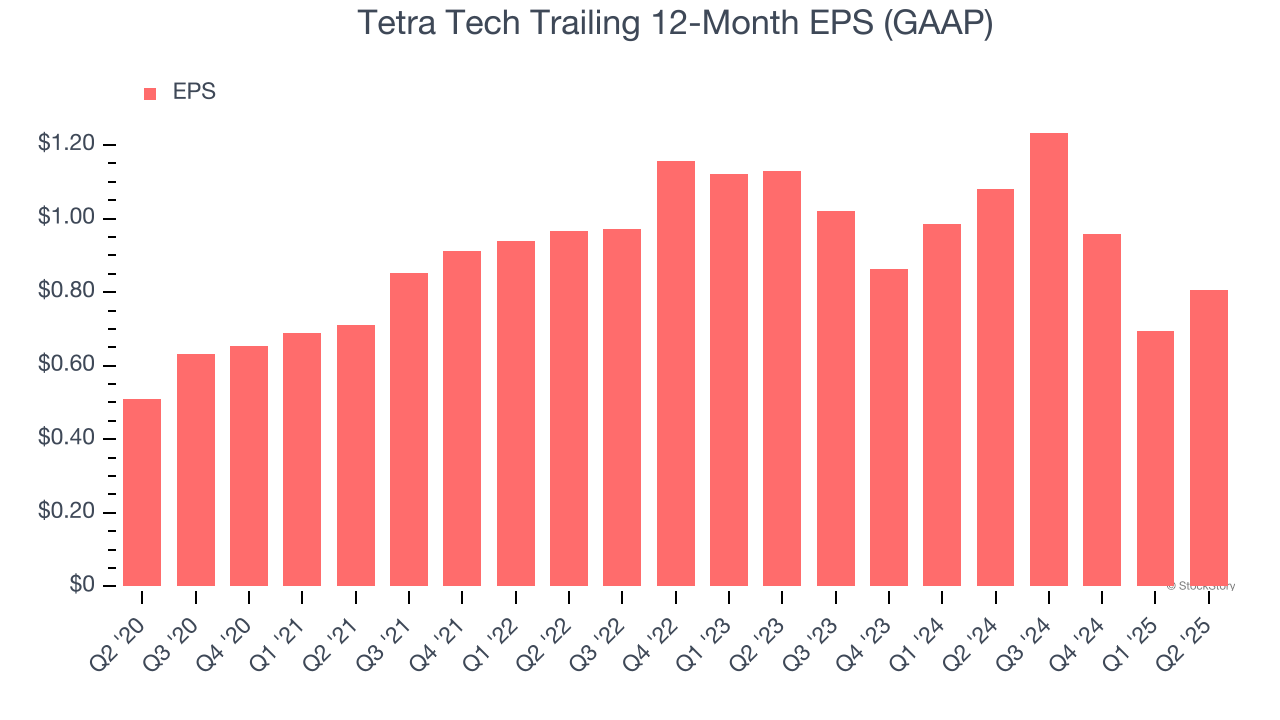

- EPS (GAAP): $0.43 vs analyst estimates of $0.37 (17% beat)

- Adjusted Operating Income: $164.9 million vs analyst estimates of $148.2 million (13.1% margin, 11.3% beat)

- Revenue Guidance for Q3 CY2025 is $1.05 billion at the midpoint, below analyst estimates of $1.13 billion

- EPS (GAAP) guidance for Q3 CY2025 is $0.41 at the midpoint, beating analyst estimates by 5.9%

- Operating Margin: 13.1%, up from 11.6% in the same quarter last year

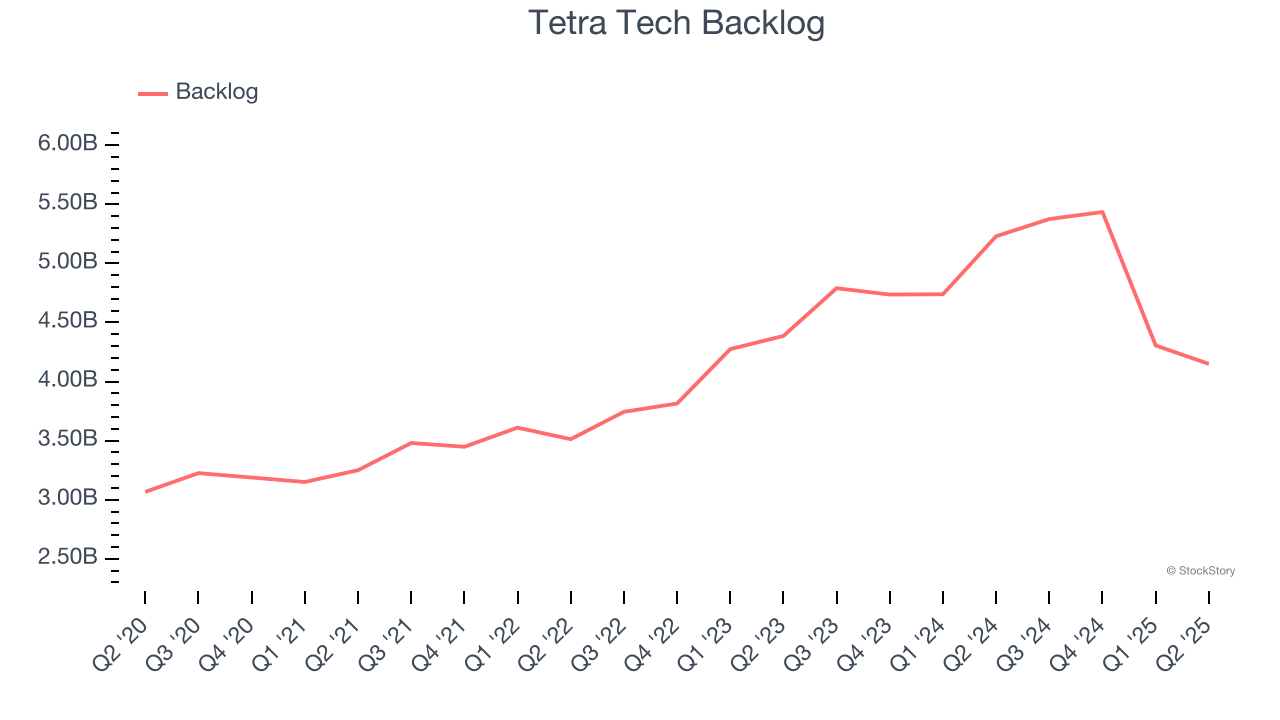

- Backlog: $4.15 billion at quarter end, down 20.7% year on year

- Market Capitalization: $9.89 billion

Dan Batrack, Chairman and CEO, commented, “Tetra Tech delivered another strong quarter with increasing revenue, record operating income, and significant operating margin expansion over the third quarter of last year. This performance is being driven by our high-end water, environmental and sustainable infrastructure services, which includes our clients’ increased funding for preparing and responding to natural disasters. Although the financial results for fiscal 2025 to date have exceeded our initial expectations, we are continuing to navigate the near-term financial impacts from the changes in U.S. federal government priorities and the related secondary impacts to our end markets.”

Company Overview

With a 50-year legacy of "Leading with Science" and operations on all seven continents, Tetra Tech (NASDAQ: TTEK) provides high-end consulting and engineering services focused on water management, environmental solutions, and sustainable infrastructure for government and commercial clients worldwide.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $4.71 billion in revenue over the past 12 months, Tetra Tech is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Tetra Tech grew its sales at an exceptional 14.6% compounded annual growth rate over the last five years. This is an encouraging starting point for our analysis because it shows Tetra Tech’s demand was higher than many business services companies.

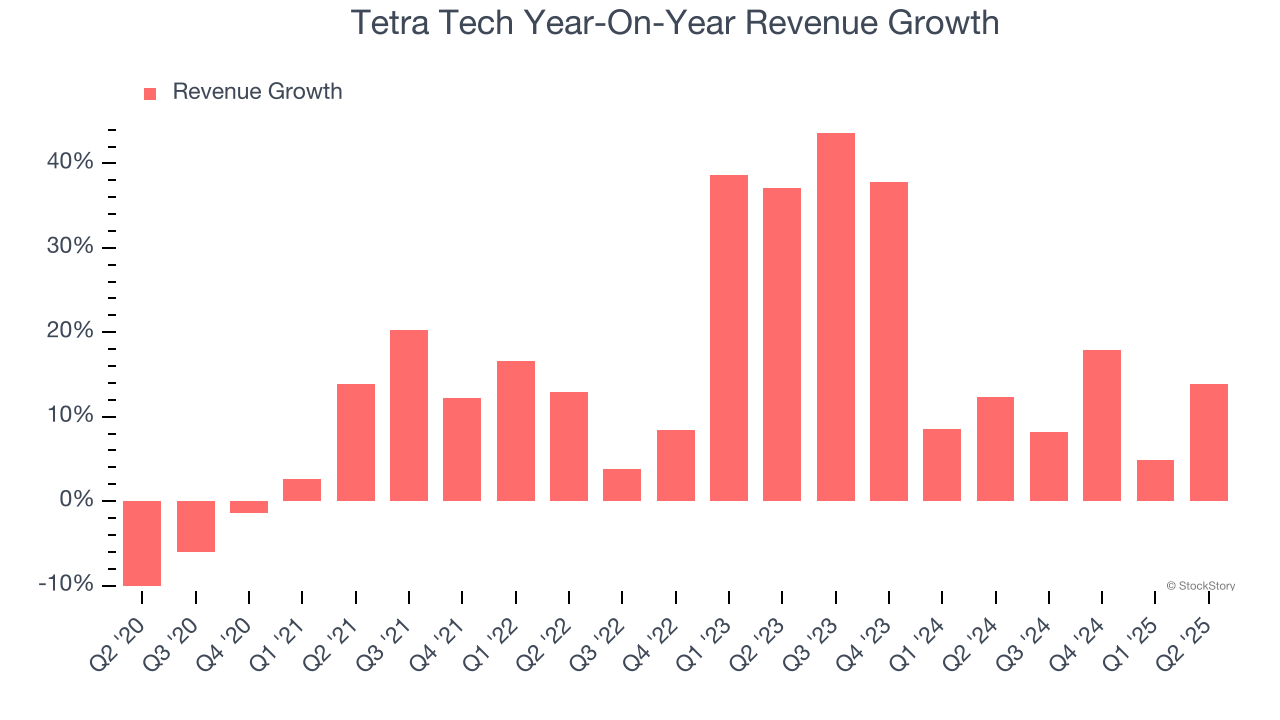

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Tetra Tech’s annualized revenue growth of 17.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Tetra Tech’s backlog reached $4.15 billion in the latest quarter and averaged 9.9% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Tetra Tech was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Tetra Tech reported year-on-year revenue growth of 13.9%, and its $1.26 billion of revenue exceeded Wall Street’s estimates by 11.9%. Company management is currently guiding for a 8.3% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 7.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

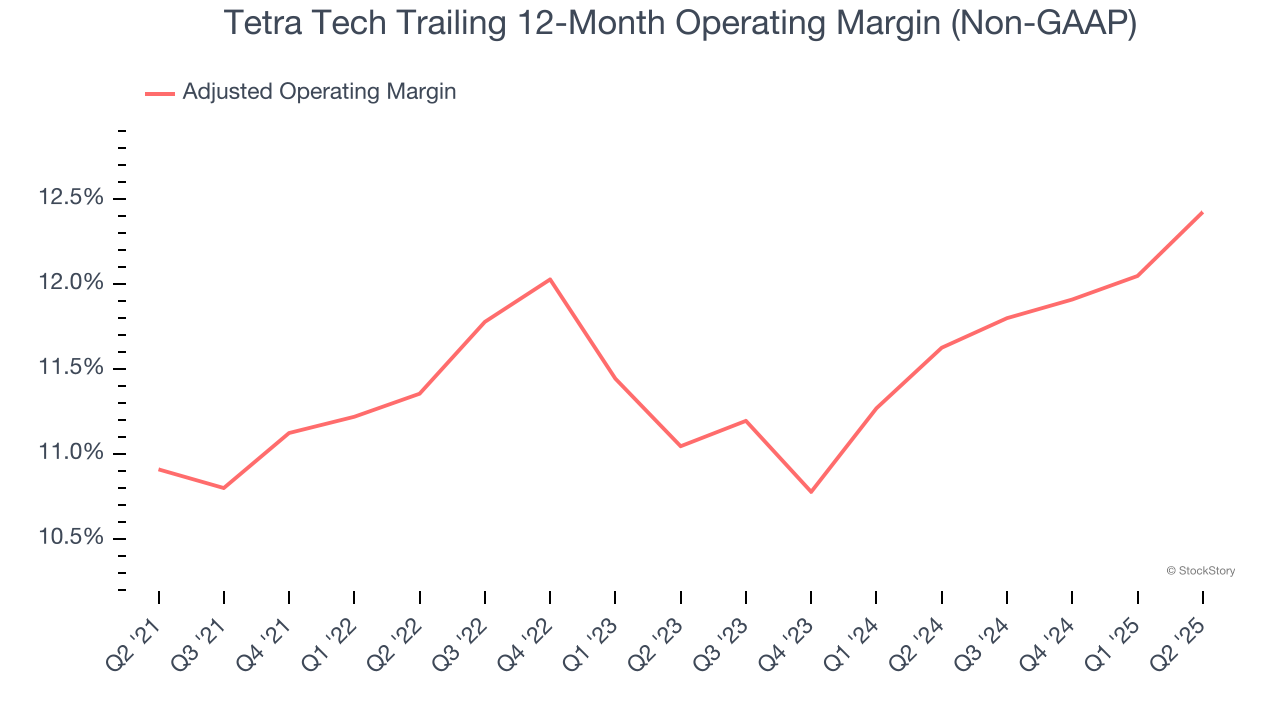

Tetra Tech has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 11.6%, higher than the broader business services sector.

Looking at the trend in its profitability, Tetra Tech’s adjusted operating margin rose by 1.5 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q2, Tetra Tech generated an adjusted operating margin profit margin of 13.1%, up 1.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tetra Tech’s EPS grew at a solid 9.6% compounded annual growth rate over the last five years. Despite its adjusted operating margin improvement during that time, this performance was lower than its 14.6% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Tetra Tech, its two-year annual EPS declines of 15.5% mark a reversal from its (seemingly) healthy five-year trend. These shorter-term results weren’t ideal, but given it was successful in other measures of financial health, we’re hopeful Tetra Tech can return to earnings growth in the future.

In Q2, Tetra Tech reported EPS at $0.43, up from $0.32 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tetra Tech’s full-year EPS of $0.81 to grow 82.2%.

Key Takeaways from Tetra Tech’s Q2 Results

We were impressed by how significantly Tetra Tech blew past analysts’ revenue, EPS, and adjusted operating income expectations this quarter. We were also excited its EPS guidance for next quarter outperformed Wall Street’s estimates by a wide margin. On the other hand, its quarterly revenue guidance and backlog fell short. Zooming out, we think this was a mixed quarter. The stock traded up 2.9% to $38.33 immediately following the results.

So do we think Tetra Tech is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.