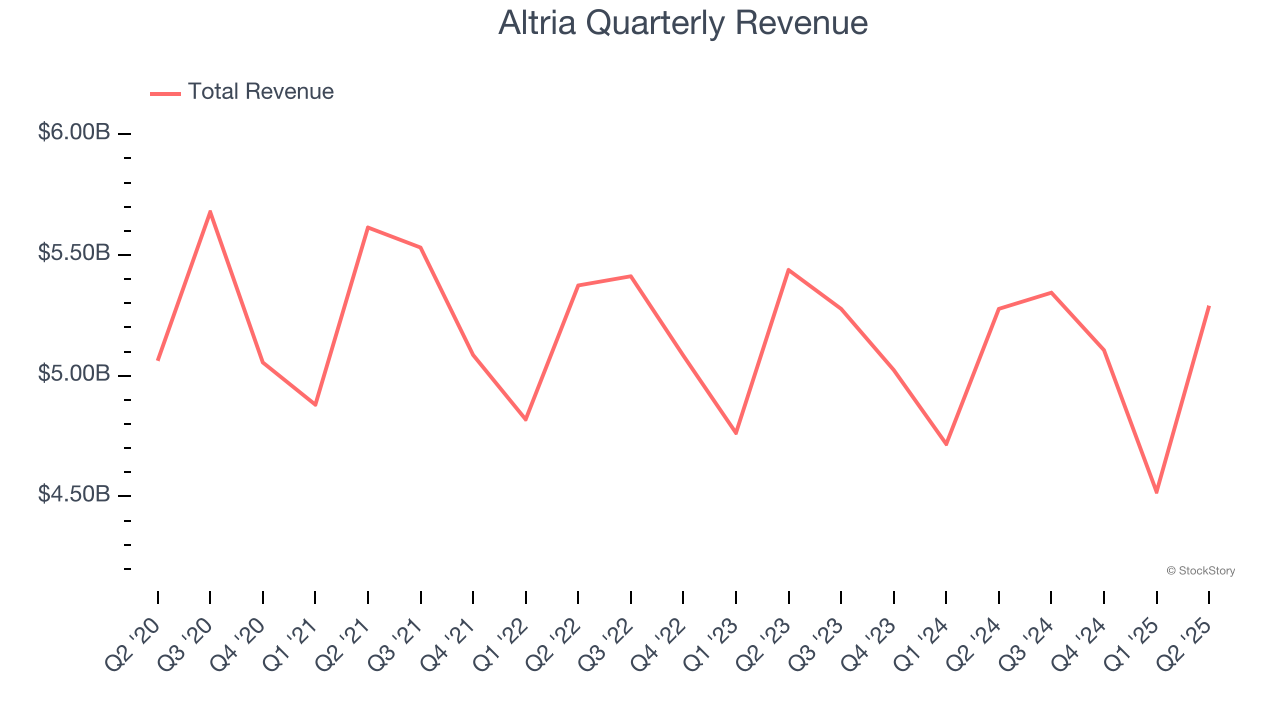

Tobacco company Altria (NYSE: MO) announced better-than-expected revenue in Q2 CY2025, but sales were flat year on year at $5.29 billion. Its non-GAAP profit of $1.44 per share was 4% above analysts’ consensus estimates.

Is now the time to buy Altria? Find out by accessing our full research report, it’s free.

Altria (MO) Q2 CY2025 Highlights:

- Revenue: $5.29 billion vs analyst estimates of $5.2 billion (flat year on year, 1.8% beat)

- Adjusted EPS: $1.44 vs analyst estimates of $1.38 (4% beat)

- Adjusted EPS guidance for the full year is $5.40 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 62.8%, up from 48% in the same quarter last year

- Market Capitalization: $99.99 billion

“In the second quarter, we continued the pursuit of our Vision while maintaining our strong and profitable core businesses,” said Billy Gifford, Altria’s Chief Executive Officer.

Company Overview

Best known for its Marlboro brand of cigarettes, Altria (NYSE: MO) offers tobacco and nicotine products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $20.26 billion in revenue over the past 12 months, Altria is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To accelerate sales, Altria likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Altria struggled to increase demand as its $20.26 billion of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a tough starting point for our analysis.

This quarter, Altria’s $5.29 billion of revenue was flat year on year but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and indicates its newer products will not lead to better top-line performance yet. At least the company is tracking well in other measures of financial health.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

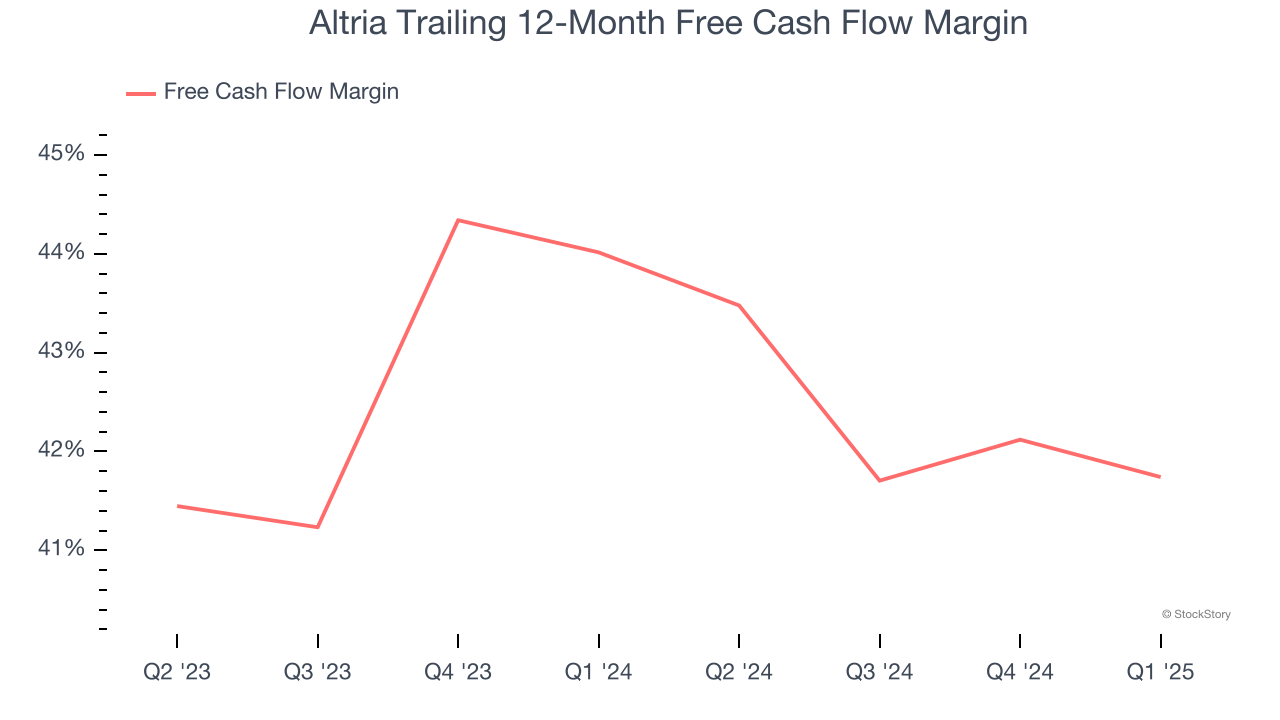

Altria has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging an eye-popping 49.3% over the last two years.

Key Takeaways from Altria’s Q2 Results

It was encouraging to see Altria beat analysts’ revenue and EPS expectations this quarter. On the other hand, its gross margin missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $59.44 immediately following the results.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.