Regional banking company Ameris Bancorp (NYSE: ABCB) beat Wall Street’s revenue expectations in Q2 CY2025, but sales were flat year on year at $300.7 million. Its non-GAAP profit of $1.59 per share was 19.3% above analysts’ consensus estimates.

Is now the time to buy Ameris Bancorp? Find out by accessing our full research report, it’s free.

Ameris Bancorp (ABCB) Q2 CY2025 Highlights:

- Net Interest Income: $231.8 million vs analyst estimates of $225.5 million (9.4% year-on-year growth, 2.8% beat)

- Net Interest Margin: 3.8% vs analyst estimates of 3.7% (19 basis point year-on-year increase, 10.2 bps beat)

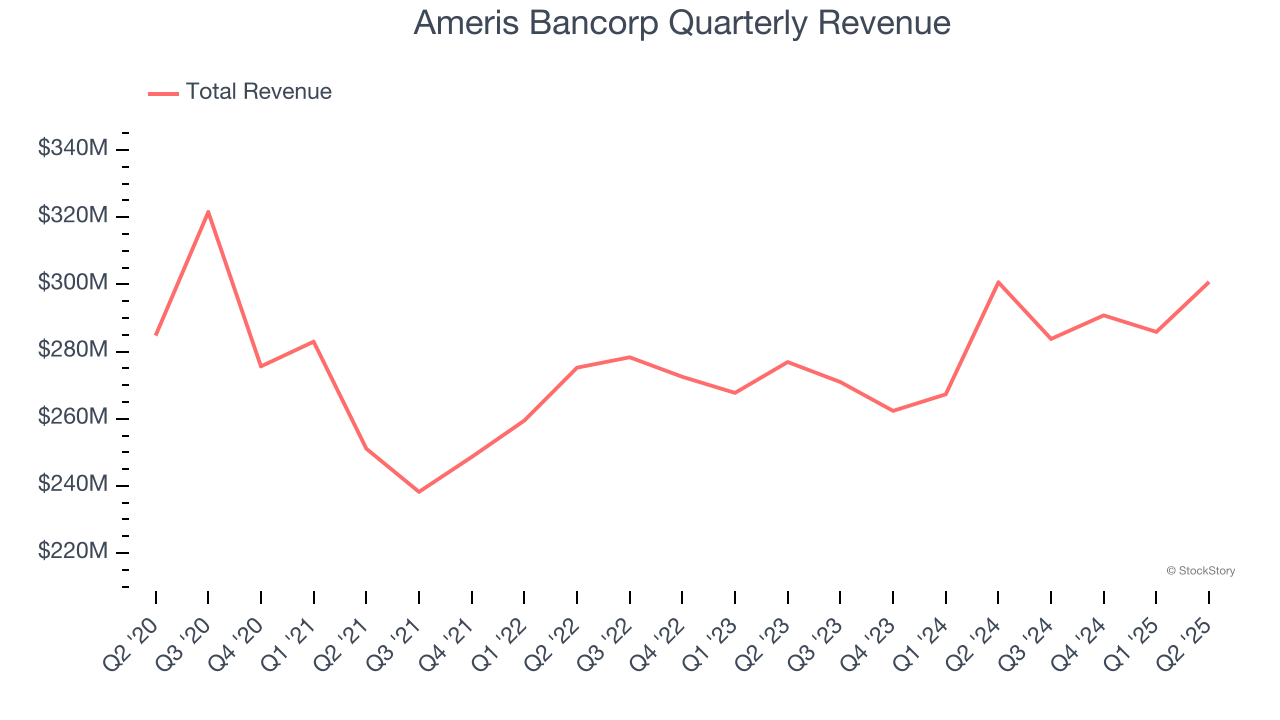

- Revenue: $300.7 million vs analyst estimates of $296.6 million (flat year on year, 1.4% beat)

- Efficiency Ratio: 51.6% vs analyst estimates of 52.6% (1 percentage point beat)

- Adjusted EPS: $1.59 vs analyst estimates of $1.33 (19.3% beat)

- Market Capitalization: $4.56 billion

Commenting on the Company’s results, Palmer Proctor, the Company’s Chief Executive Officer, said, “Our second quarter results underscore the strength, consistency, and long-term value of the Ameris franchise. We delivered above-peer profitability, with a return on assets of 1.65% and a return on tangible common equity of 15.82%. Tangible book value per share - one of our long-standing strategic priorities - grew at a 15.5% annualized rate to surpass $41. Other key performance indicators, including our net interest margin, allowance coverage ratio, and efficiency ratio, remain among the best in the industry. Backed by a strong balance sheet and a proven ability to execute, we are well positioned to capitalize on growth opportunities across our Southeast footprint and drive continued success through the remainder of 2025 and beyond.”

Company Overview

Tracing its roots back to 1971 and expanding significantly through both organic growth and strategic acquisitions, Ameris Bancorp (NYSE: ABCB) is a financial holding company that provides a full range of banking services to retail and commercial customers across select markets in the southeastern United States.

Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

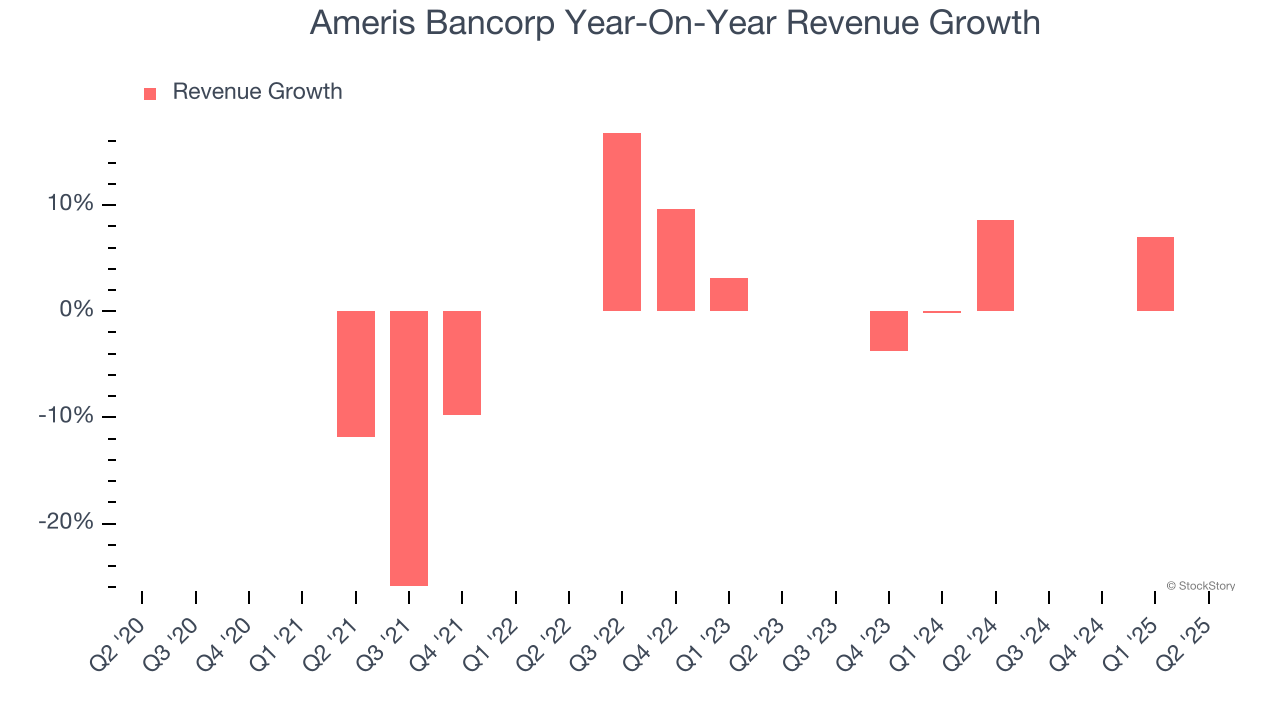

Regrettably, Ameris Bancorp’s revenue grew at a mediocre 4.7% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the bank sector, but there are still things to like about Ameris Bancorp.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Ameris Bancorp’s recent performance shows its demand has slowed as its annualized revenue growth of 3% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Ameris Bancorp’s $300.7 million of revenue was flat year on year but beat Wall Street’s estimates by 1.4%.

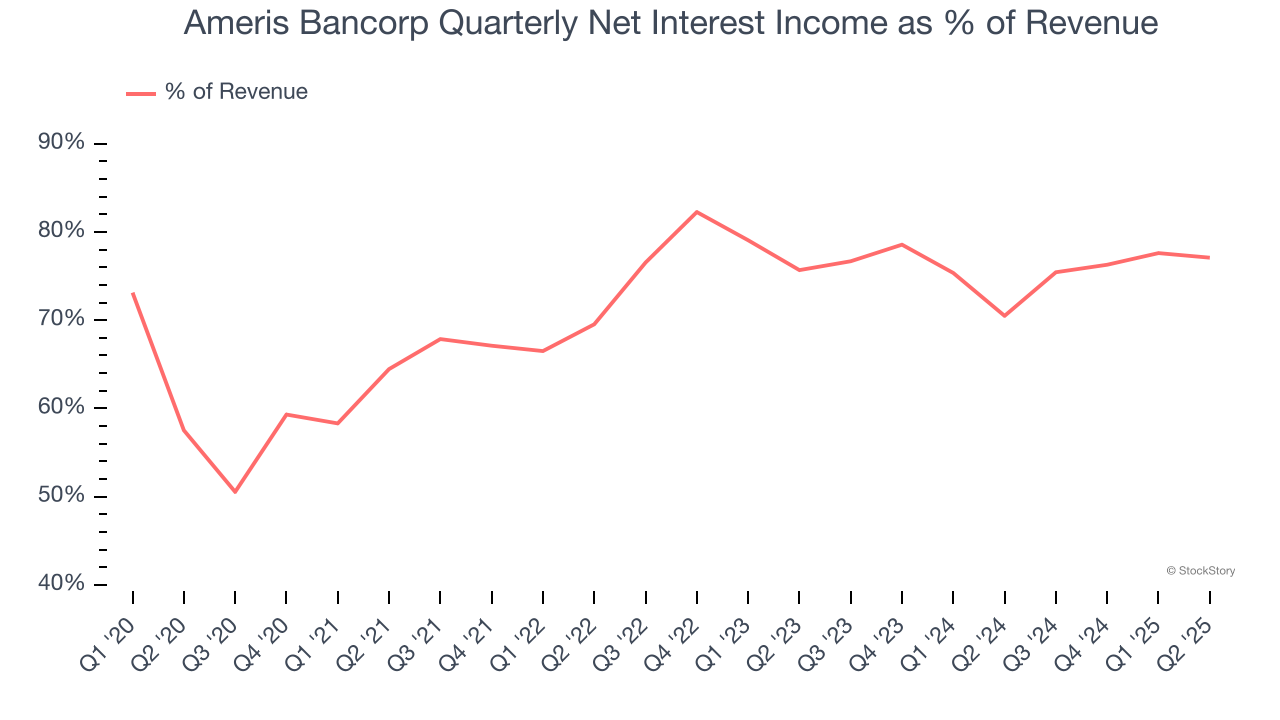

Net interest income made up 71.2% of the company’s total revenue during the last five years, meaning lending operations are Ameris Bancorp’s largest source of revenue.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

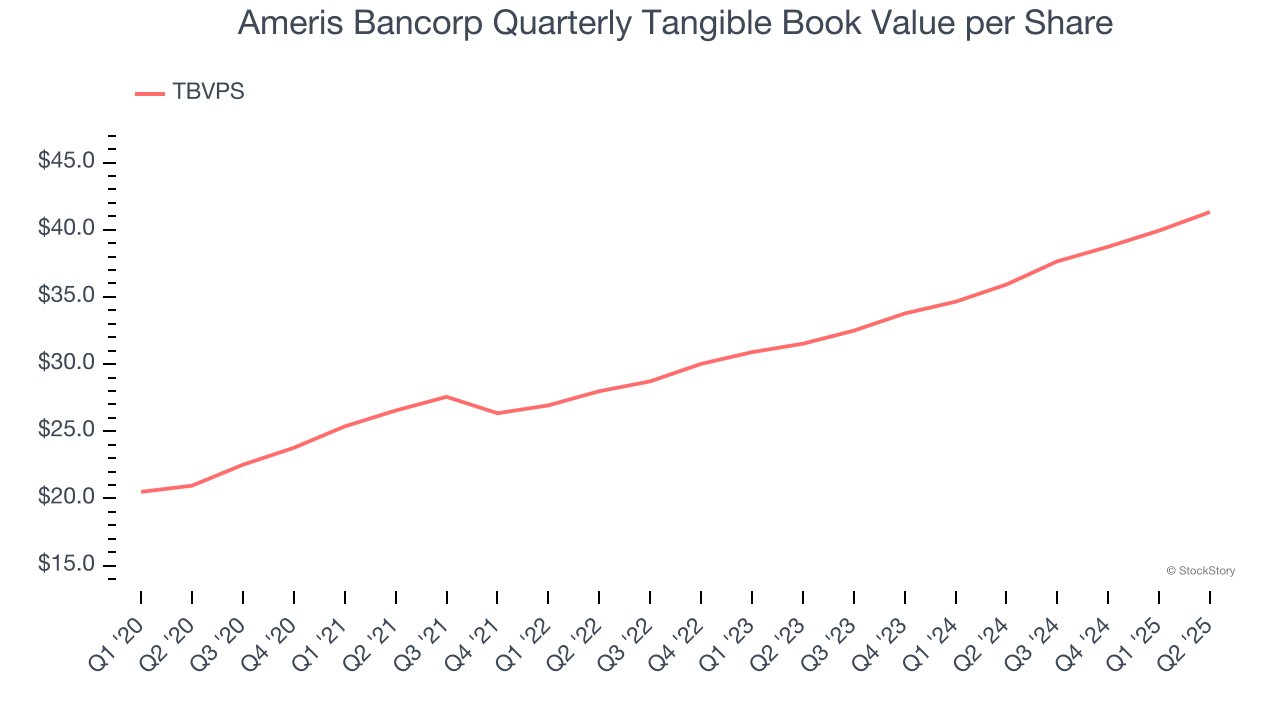

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

Ameris Bancorp’s TBVPS grew at an incredible 14.5% annual clip over the last five years. The last two years show a similar trajectory as TBVPS grew by 14.5% annually from $31.52 to $41.32 per share.

Over the next 12 months, Consensus estimates call for Ameris Bancorp’s TBVPS to grow by 10.5% to $45.68, solid growth rate.

Key Takeaways from Ameris Bancorp’s Q2 Results

We enjoyed seeing Ameris Bancorp beat analysts’ expectations across the board this quarter. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $66.40 immediately following the results.

Indeed, Ameris Bancorp had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.