Credit reporting company TransUnion (NYSE: TRU) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 9.5% year on year to $1.14 billion. The company expects next quarter’s revenue to be around $1.13 billion, close to analysts’ estimates. Its non-GAAP profit of $1.08 per share was 9% above analysts’ consensus estimates.

Is now the time to buy TransUnion? Find out by accessing our full research report, it’s free.

TransUnion (TRU) Q2 CY2025 Highlights:

- Revenue: $1.14 billion vs analyst estimates of $1.10 billion (9.5% year-on-year growth, 3.7% beat)

- Adjusted EPS: $1.08 vs analyst estimates of $0.99 (9% beat)

- Adjusted EBITDA: $407 million vs analyst estimates of $386.5 million (35.7% margin, 5.3% beat)

- The company lifted its revenue guidance for the full year to $4.45 billion at the midpoint from $4.39 billion, a 1.5% increase

- Management raised its full-year Adjusted EPS guidance to $4.09 at the midpoint, a 2% increase

- EBITDA guidance for the full year is $1.60 billion at the midpoint, in line with analyst expectations

- Operating Margin: 16.9%, in line with the same quarter last year

- Free Cash Flow Margin: 18.8%, down from 21.8% in the same quarter last year

- Market Capitalization: $18.45 billion

“In the second quarter, TransUnion delivered strong results that again exceeded financial guidance,” said Chris Cartwright, President and CEO.

Company Overview

One of the three major credit bureaus in the United States alongside Equifax and Experian, TransUnion (NYSE: TRU) is a global information and insights company that provides credit reports, fraud prevention tools, and data analytics to help businesses make decisions and consumers manage their financial health.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

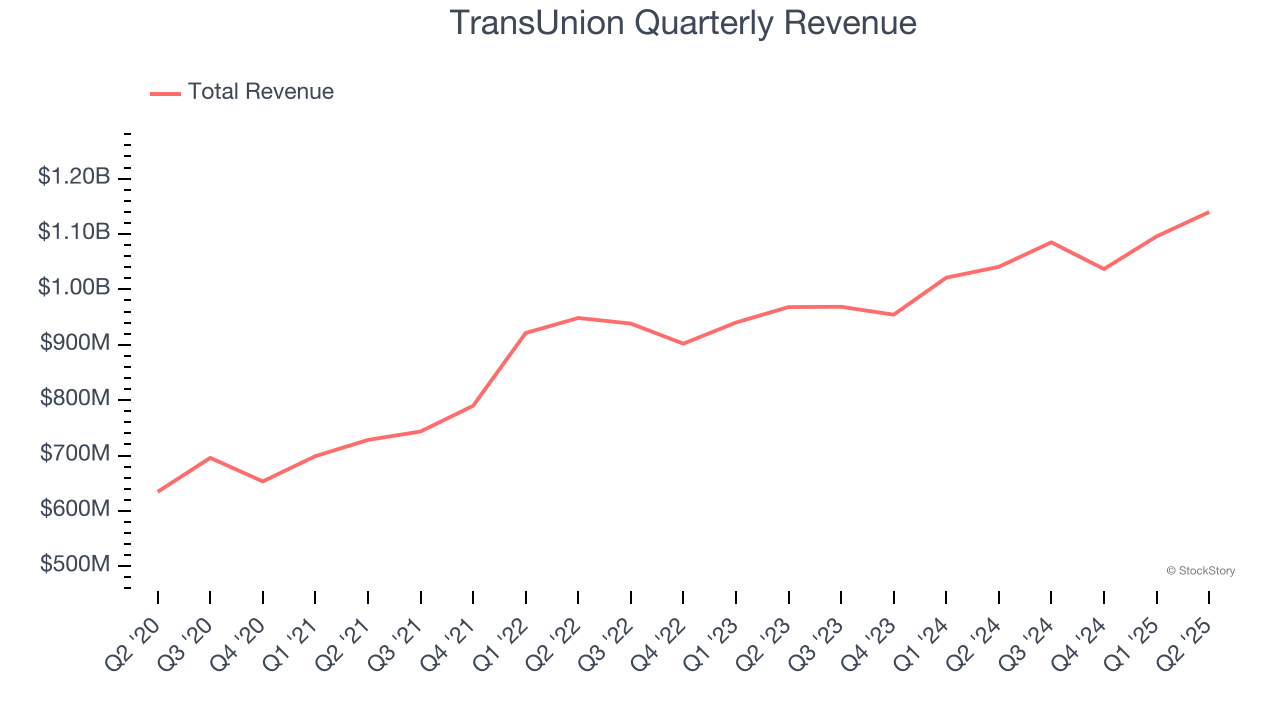

With $4.36 billion in revenue over the past 12 months, TransUnion is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

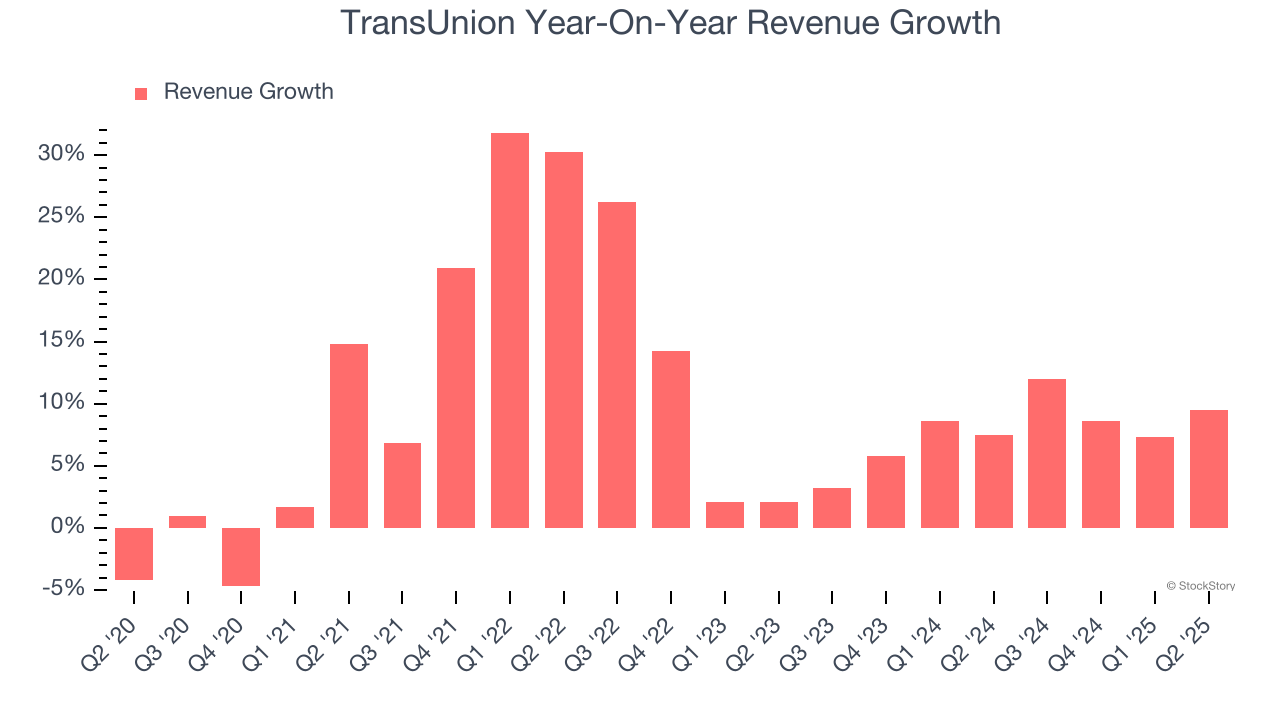

As you can see below, TransUnion’s 10.1% annualized revenue growth over the last five years was impressive. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. TransUnion’s annualized revenue growth of 7.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, TransUnion reported year-on-year revenue growth of 9.5%, and its $1.14 billion of revenue exceeded Wall Street’s estimates by 3.7%. Company management is currently guiding for a 3.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a slight deceleration versus the last two years. Still, this projection is above the sector average and implies the market sees some success for its newer products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

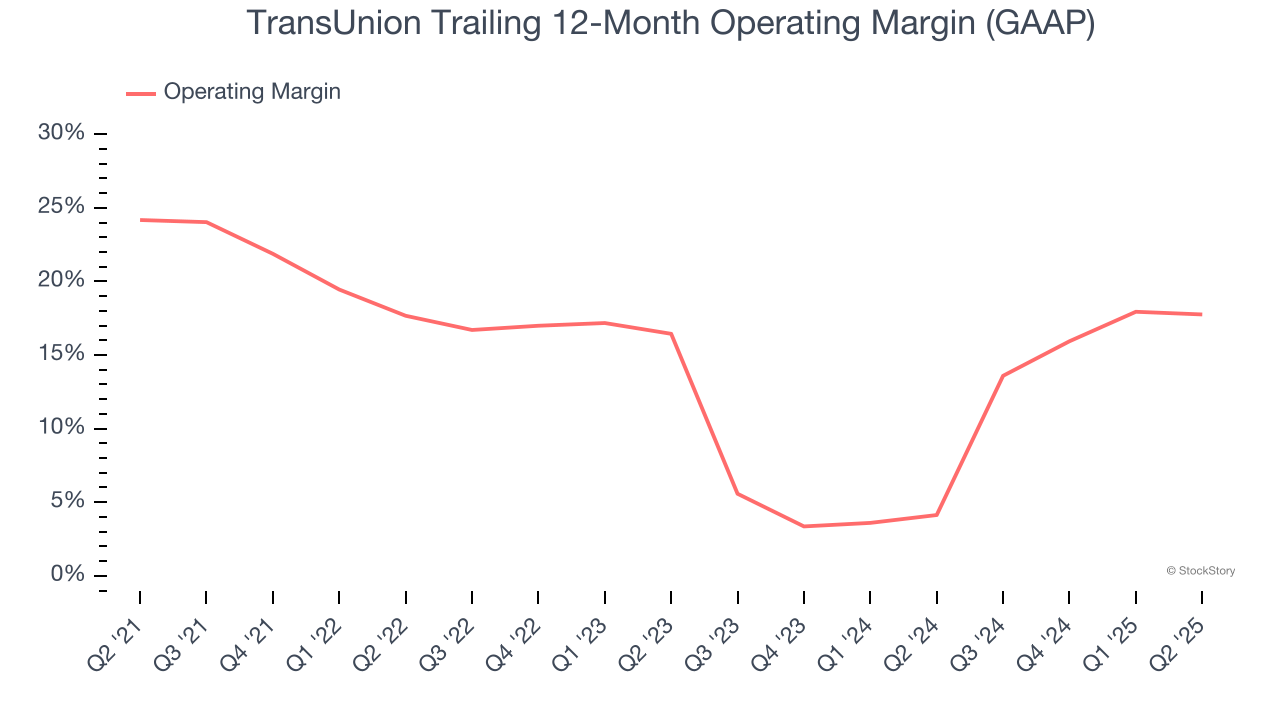

TransUnion has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average operating margin of 15.5%.

Looking at the trend in its profitability, TransUnion’s operating margin decreased by 6.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q2, TransUnion generated an operating margin profit margin of 16.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

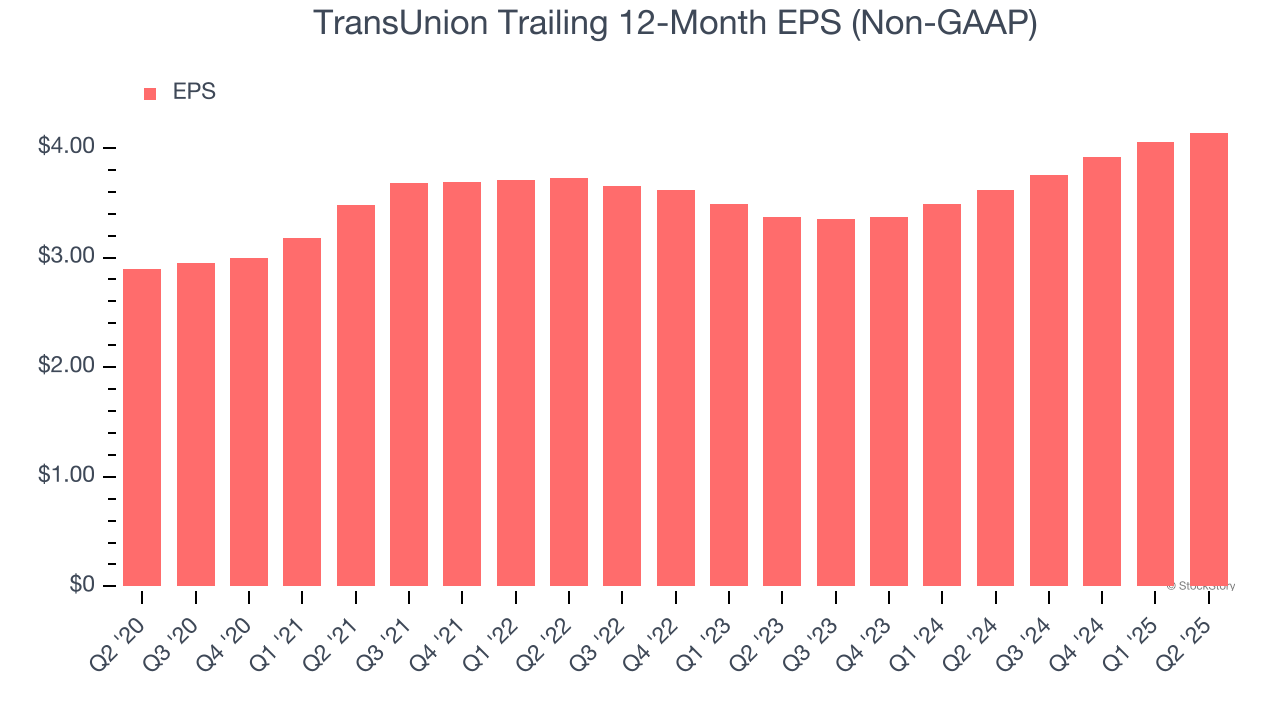

TransUnion’s EPS grew at an unimpressive 7.4% compounded annual growth rate over the last five years, lower than its 10.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

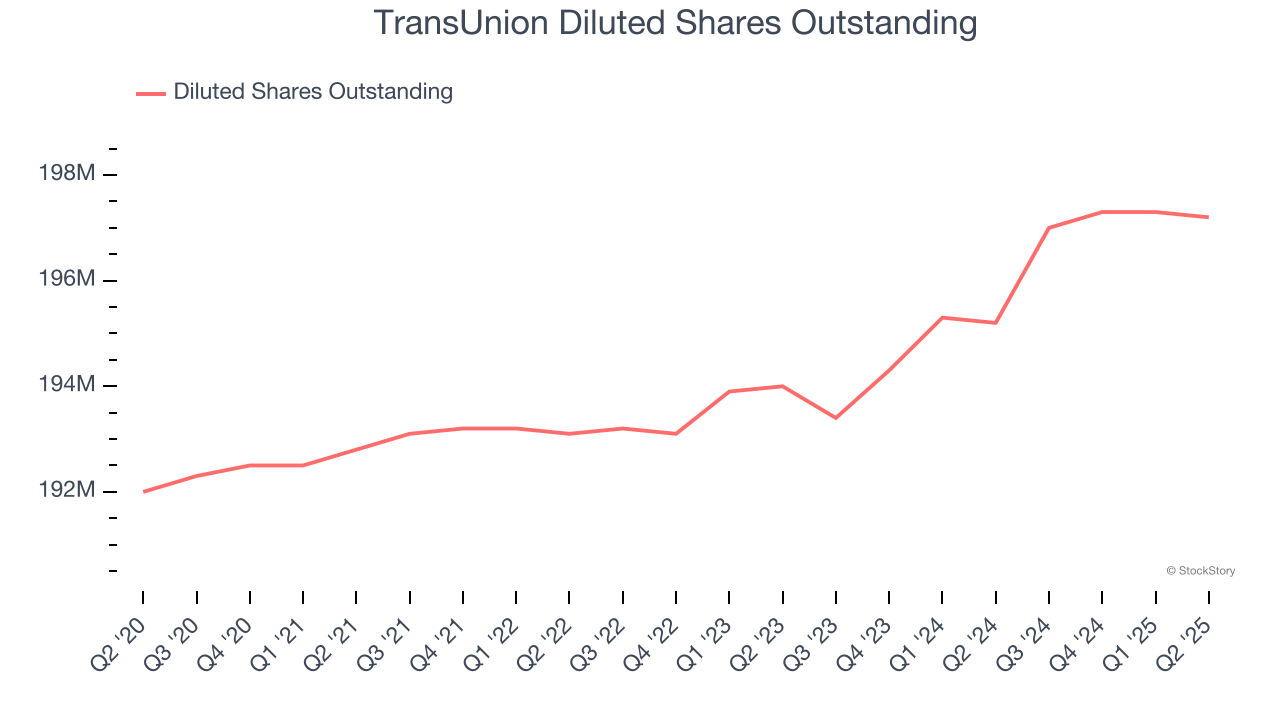

We can take a deeper look into TransUnion’s earnings to better understand the drivers of its performance. As we mentioned earlier, TransUnion’s operating margin was flat this quarter but declined by 6.4 percentage points over the last five years. Its share count also grew by 2.7%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For TransUnion, its two-year annual EPS growth of 10.8% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q2, TransUnion reported EPS at $1.08, up from $0.99 in the same quarter last year. This print beat analysts’ estimates by 9%. Over the next 12 months, Wall Street expects TransUnion’s full-year EPS of $4.14 to grow 6.5%.

Key Takeaways from TransUnion’s Q2 Results

We enjoyed seeing TransUnion beat analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. We were also glad it slightly raised its full-year revenue and EPS guidance. Overall, this print had some key positives. The stock remained flat at $94.46 immediately after reporting.

Is TransUnion an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.