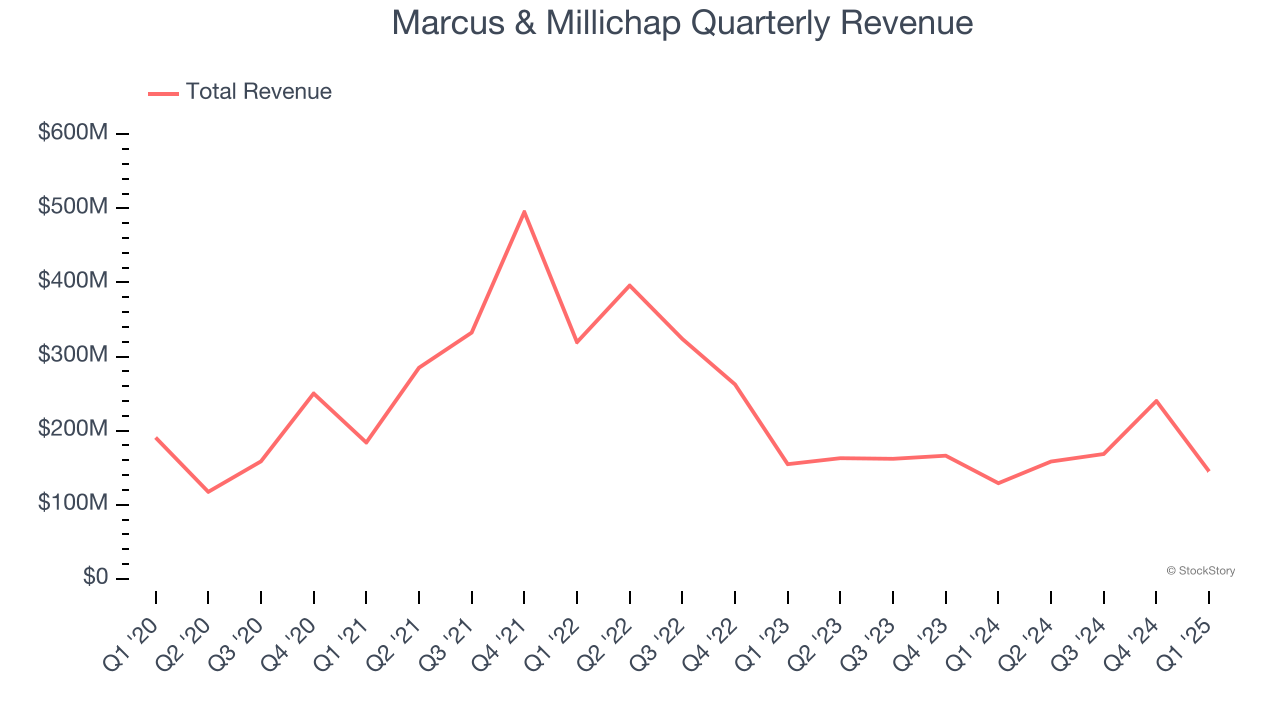

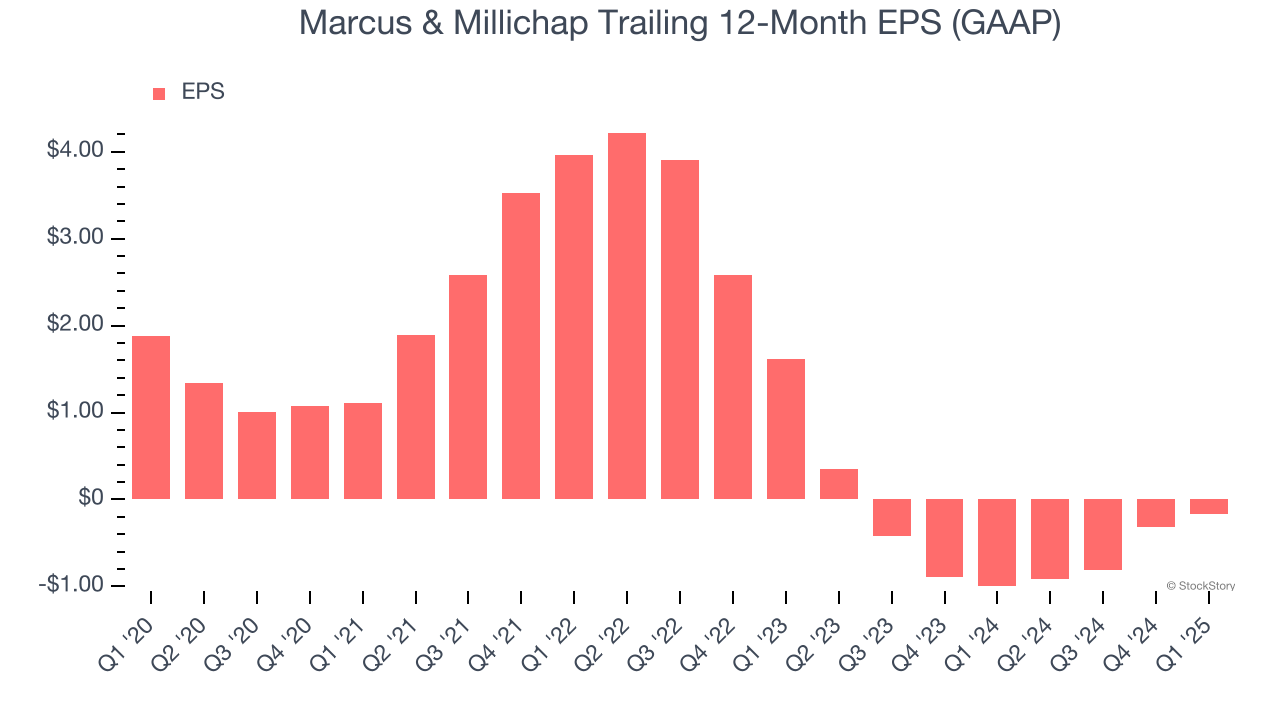

Real estate brokerage and services firm Marcus & Millichap (NYSE: MMI) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 12.3% year on year to $145 million. Its GAAP loss of $0.11 per share was 31.3% above analysts’ consensus estimates.

Is now the time to buy Marcus & Millichap? Find out by accessing our full research report, it’s free.

Marcus & Millichap (MMI) Q1 CY2025 Highlights:

- Revenue: $145 million vs analyst estimates of $140.2 million (12.3% year-on-year growth, 3.5% beat)

- EPS (GAAP): -$0.11 vs analyst estimates of -$0.16 (31.3% beat)

- Adjusted EBITDA: -$8.74 million vs analyst estimates of -$16.5 million (-6% margin, 47% beat)

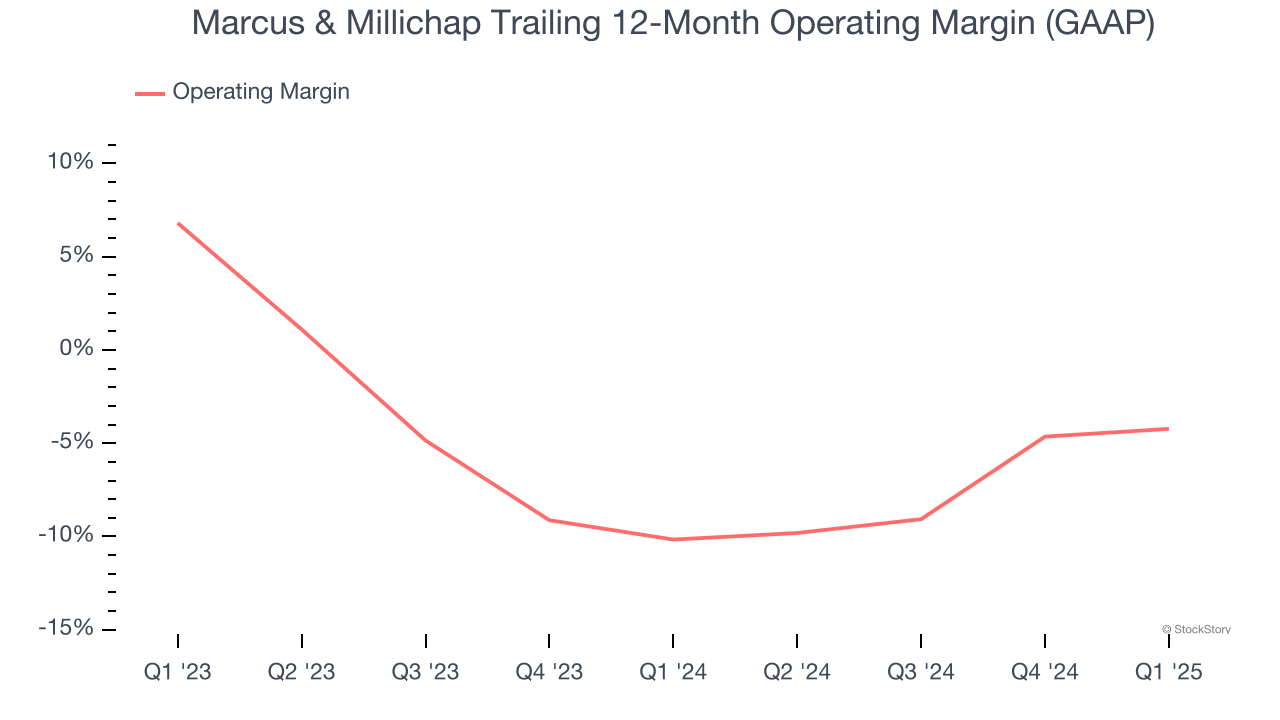

- Operating Margin: -12.2%, up from -15.4% in the same quarter last year

- Market Capitalization: $1.15 billion

“We are pleased to report an improved first quarter, reflecting our strategic focus and ability to execute despite persistent headwinds across the sector,” said Hessam Nadji, president and chief executive officer of Marcus & Millichap.

Company Overview

Founded in 1971, Marcus & Millichap (NYSE: MMI) specializes in commercial real estate investment sales, financing, research, and advisory services.

Sales Growth

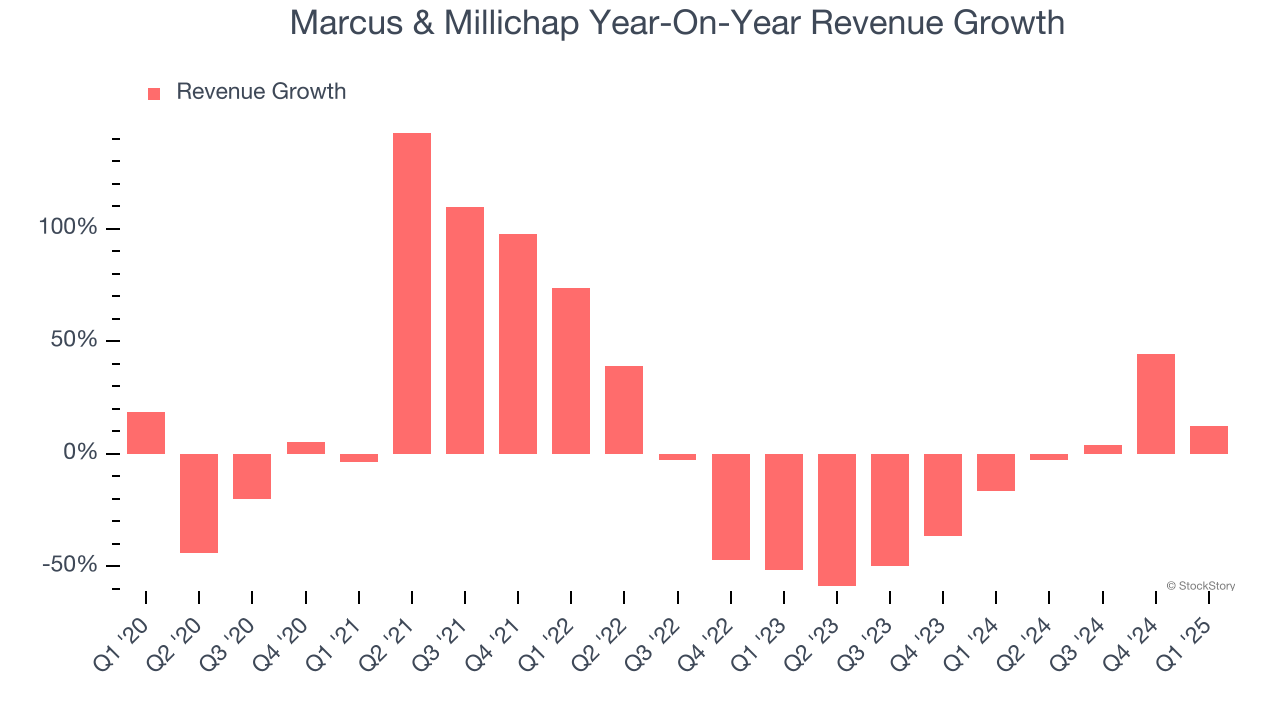

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Marcus & Millichap’s demand was weak and its revenue declined by 3.2% per year. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Marcus & Millichap’s recent performance shows its demand remained suppressed as its revenue has declined by 20.9% annually over the last two years.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Brokerage and Financing, which are 85.2% and 12.5% of revenue. Over the last two years, Marcus & Millichap’s Brokerage revenue (commission fees) averaged 12.9% year-on-year growth while its Financing revenue (financing fees) averaged 25.9% growth.

This quarter, Marcus & Millichap reported year-on-year revenue growth of 12.3%, and its $145 million of revenue exceeded Wall Street’s estimates by 3.5%.

Looking ahead, sell-side analysts expect revenue to grow 14.2% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and indicates its newer products and services will spur better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Marcus & Millichap’s operating margin has risen over the last 12 months, but it still averaged negative 7% over the last two years. This is due to its large expense base and inefficient cost structure.

In Q1, Marcus & Millichap generated a negative 12.2% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Marcus & Millichap, its EPS declined by 15.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q1, Marcus & Millichap reported EPS at negative $0.11, up from negative $0.26 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Marcus & Millichap’s full-year EPS of negative $0.17 will reach break even.

Key Takeaways from Marcus & Millichap’s Q1 Results

We were impressed by how significantly Marcus & Millichap blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.2% to $29.75 immediately following the results.

Marcus & Millichap had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.