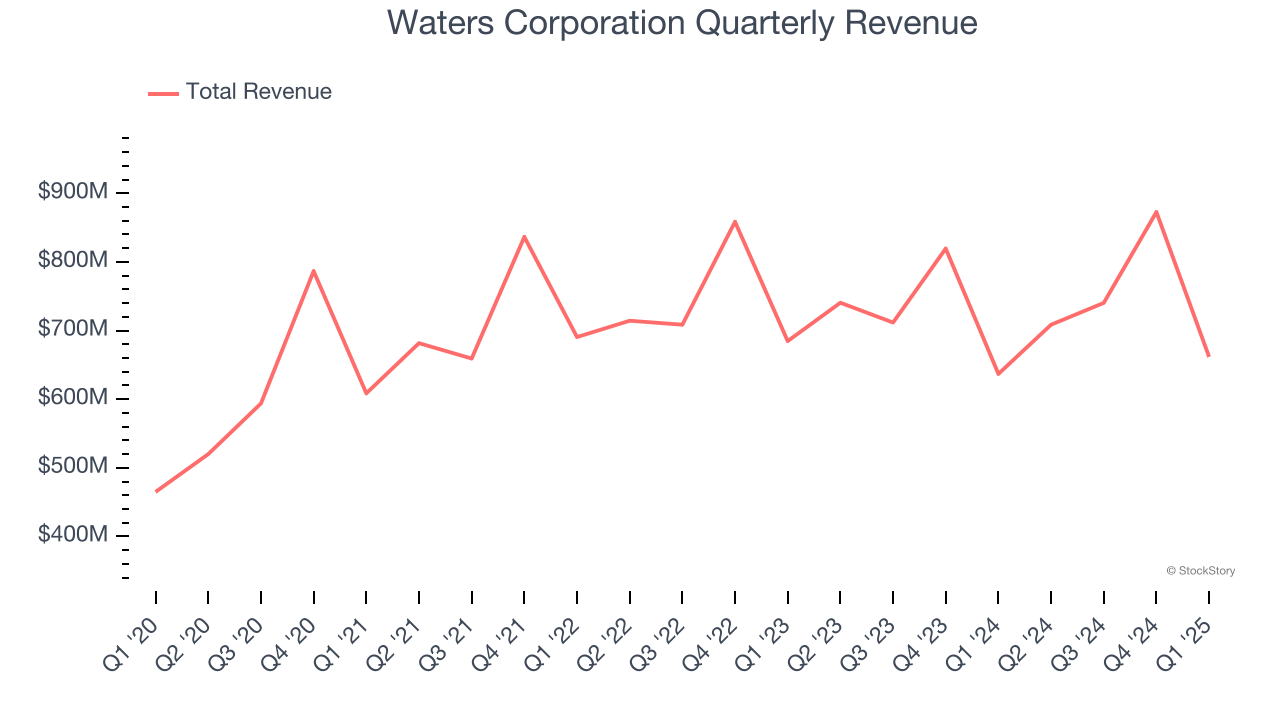

Scientific instruments company Waters Corporation (NYSE: WAT) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 3.9% year on year to $661.7 million. Guidance for next quarter’s revenue was better than expected at $751 million at the midpoint, 1.9% above analysts’ estimates. Its non-GAAP profit of $2.25 per share was 1.3% above analysts’ consensus estimates.

Is now the time to buy Waters Corporation? Find out by accessing our full research report, it’s free.

Waters Corporation (WAT) Q1 CY2025 Highlights:

- Revenue: $661.7 million vs analyst estimates of $654.1 million (3.9% year-on-year growth, 1.2% beat)

- Adjusted EPS: $2.25 vs analyst estimates of $2.22 (1.3% beat)

- Adjusted EBITDA: $214 million vs analyst estimates of $205.8 million (32.3% margin, 4% beat)

- Revenue Guidance for Q2 CY2025 is $751 million at the midpoint, above analyst estimates of $737.2 million

- Management slightly raised its full-year Adjusted EPS guidance to $12.90 at the midpoint

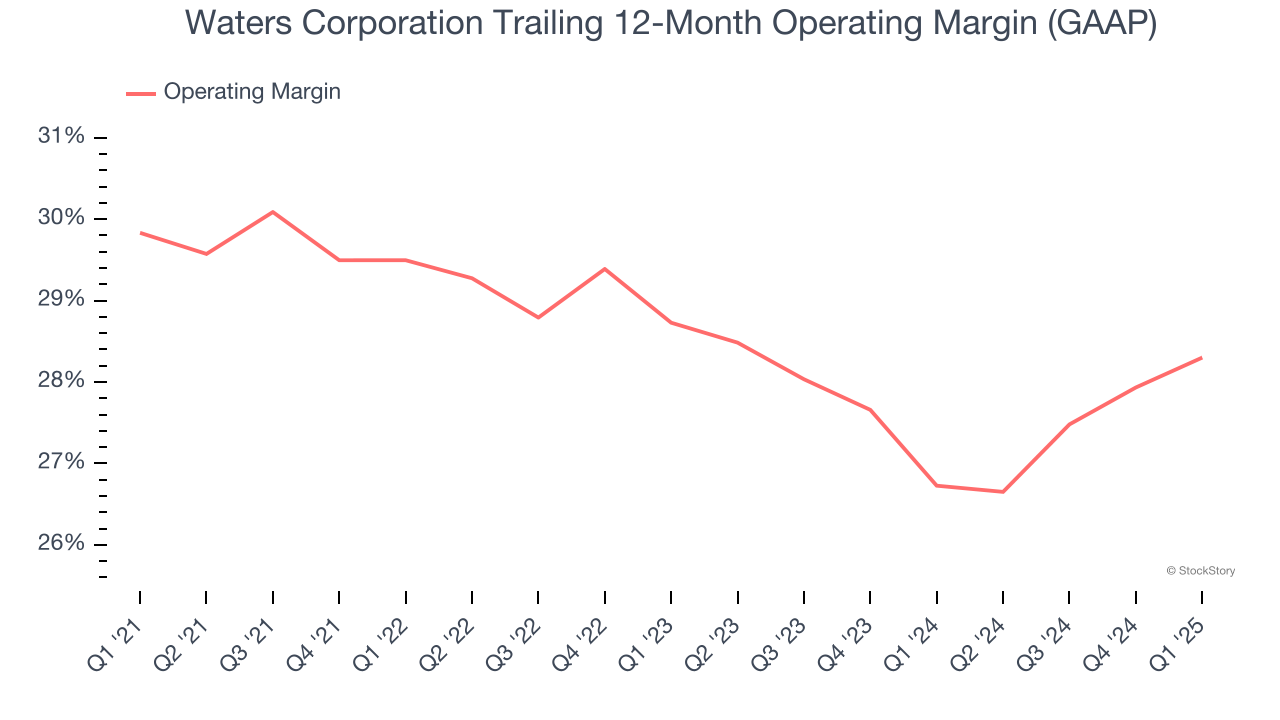

- Operating Margin: 22.9%, up from 21% in the same quarter last year

- Free Cash Flow Margin: 35.3%, down from 36.8% in the same quarter last year

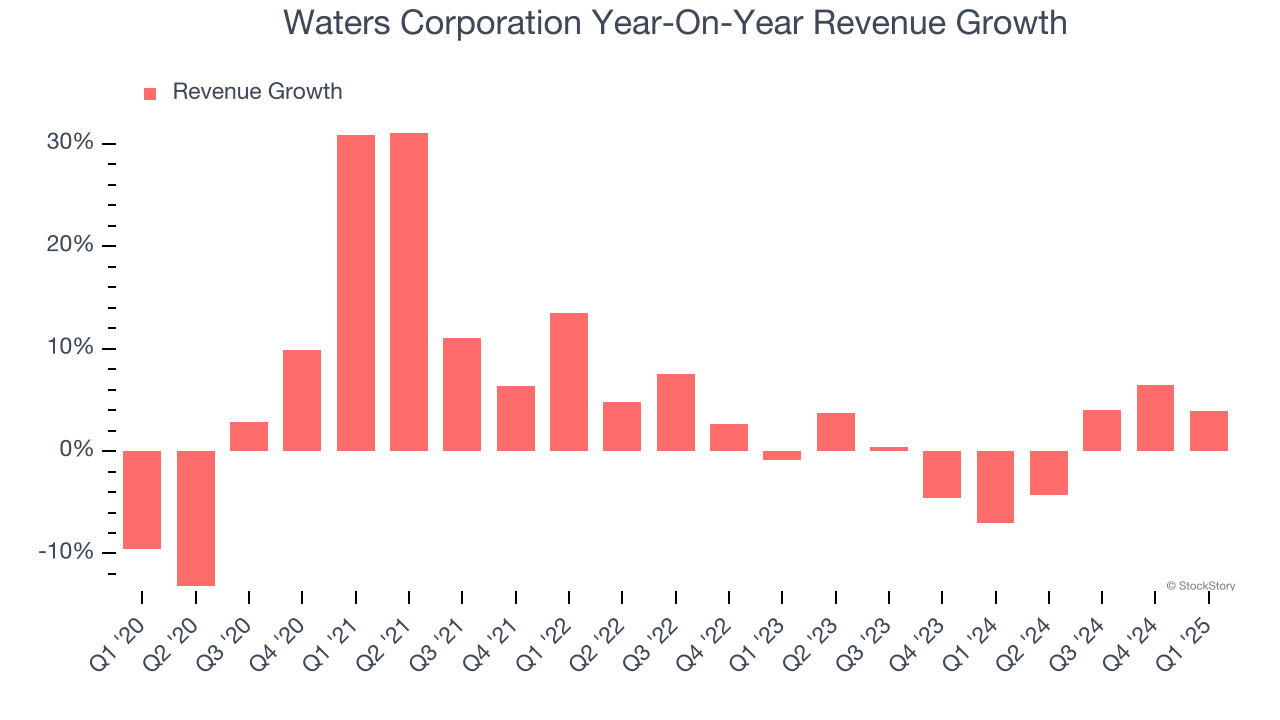

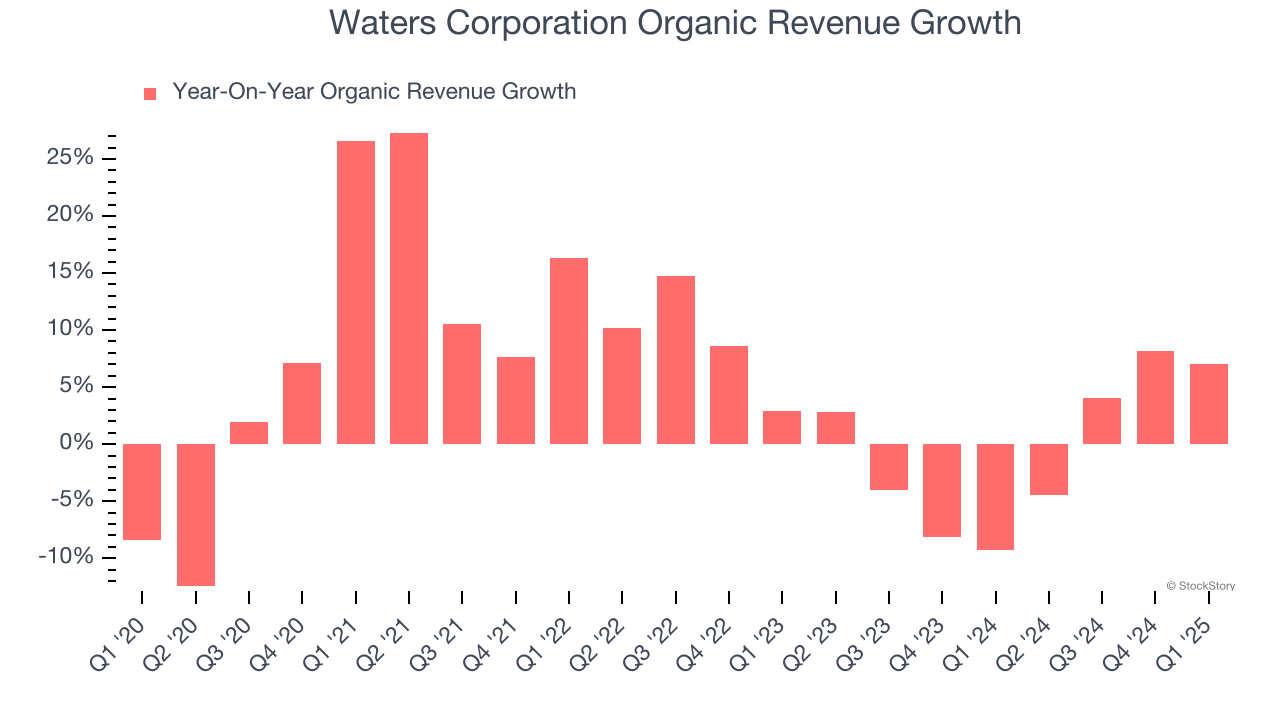

- Organic Revenue rose 7% year on year (-9.3% in the same quarter last year)

- Market Capitalization: $20.73 billion

"Thanks to the focus and dedication of our teams, the momentum in our business has remained strong despite a very dynamic external environment," said Dr. Udit Batra, President & CEO, Waters Corporation.

Company Overview

Founded in 1958 and pioneering innovations in laboratory analysis for over six decades, Waters (NYSE: WAT) develops and manufactures analytical instruments, software, and consumables for liquid chromatography, mass spectrometry, and thermal analysis used in scientific research and quality testing.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Waters Corporation grew its sales at a mediocre 4.8% compounded annual growth rate. This was below our standard for the healthcare sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Waters Corporation’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

Waters Corporation also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Waters Corporation’s organic revenue was flat. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Waters Corporation reported modest year-on-year revenue growth of 3.9% but beat Wall Street’s estimates by 1.2%. Company management is currently guiding for a 6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Waters Corporation has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 28.6%.

Looking at the trend in its profitability, Waters Corporation’s operating margin decreased by 1.5 percentage points over the last five years. A silver lining is that on a two-year basis, its margin has stabilized. Still, shareholders will want to see Waters Corporation become more profitable in the future.

In Q1, Waters Corporation generated an operating profit margin of 22.9%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

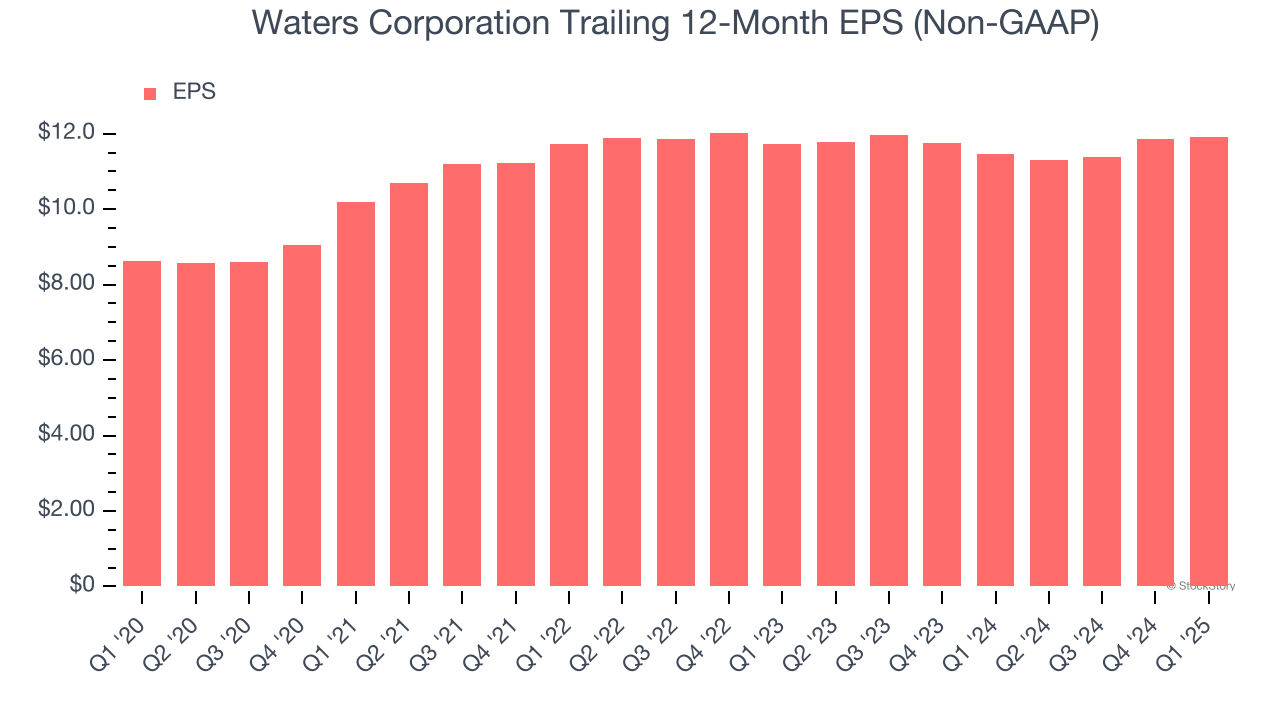

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Waters Corporation’s EPS grew at a decent 6.7% compounded annual growth rate over the last five years, higher than its 4.8% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t expand.

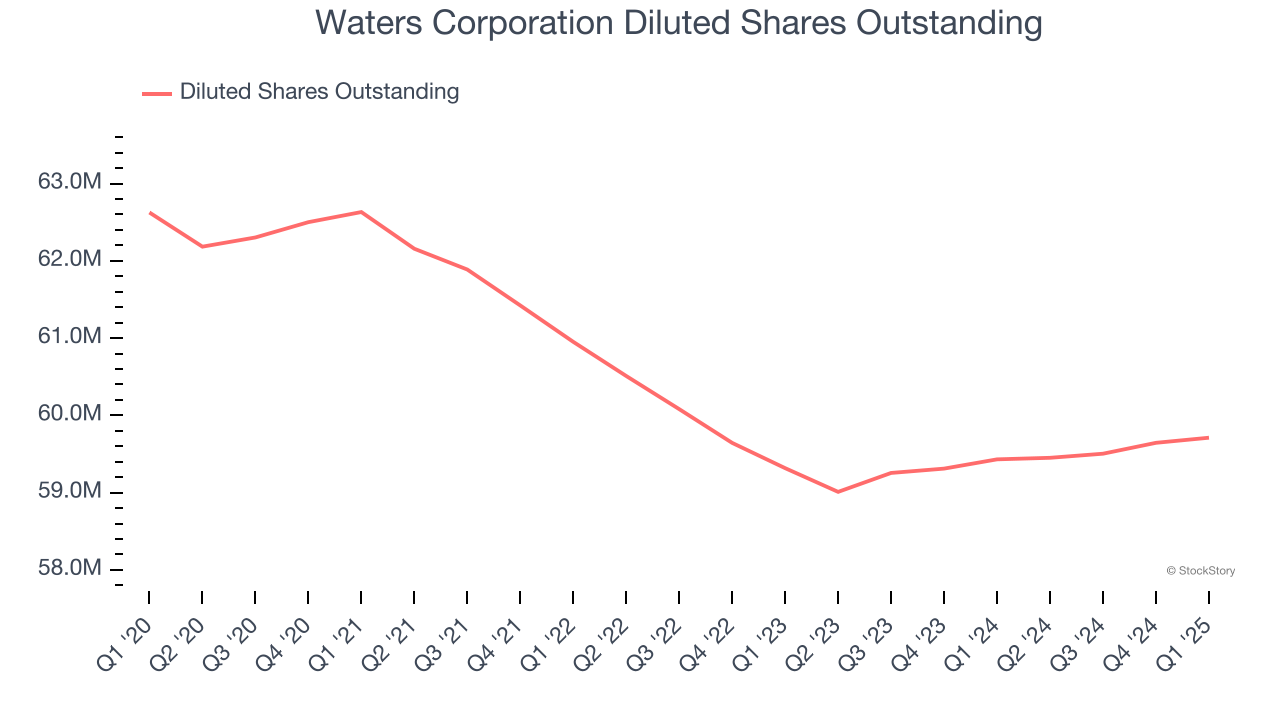

Diving into the nuances of Waters Corporation’s earnings can give us a better understanding of its performance. A five-year view shows that Waters Corporation has repurchased its stock, shrinking its share count by 4.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, Waters Corporation reported EPS at $2.25, up from $2.21 in the same quarter last year. This print beat analysts’ estimates by 1.3%. Over the next 12 months, Wall Street expects Waters Corporation’s full-year EPS of $11.91 to grow 11.1%.

Key Takeaways from Waters Corporation’s Q1 Results

It was great to see Waters Corporation’s revenue guidance for next quarter top analysts’ expectations. We were also happy its organic revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $350.53 immediately following the results.

So do we think Waters Corporation is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.