Shareholders of SAIC would probably like to forget the past six months even happened. The stock dropped 22.3% and now trades at $115.71. This might have investors contemplating their next move.

Is now the time to buy SAIC, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think SAIC Will Underperform?

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons why we avoid SAIC and a stock we'd rather own.

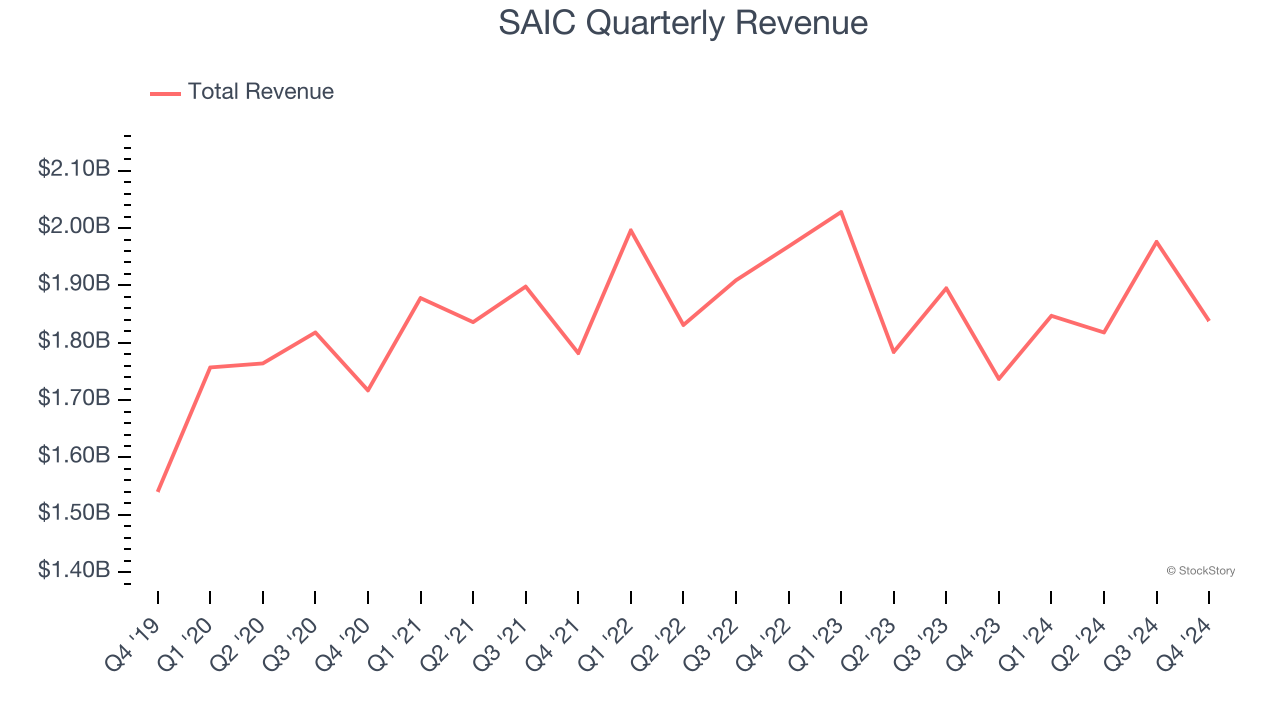

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, SAIC grew its sales at a tepid 3.2% compounded annual growth rate. This was below our standard for the business services sector.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect SAIC’s revenue to rise by 2.7%. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

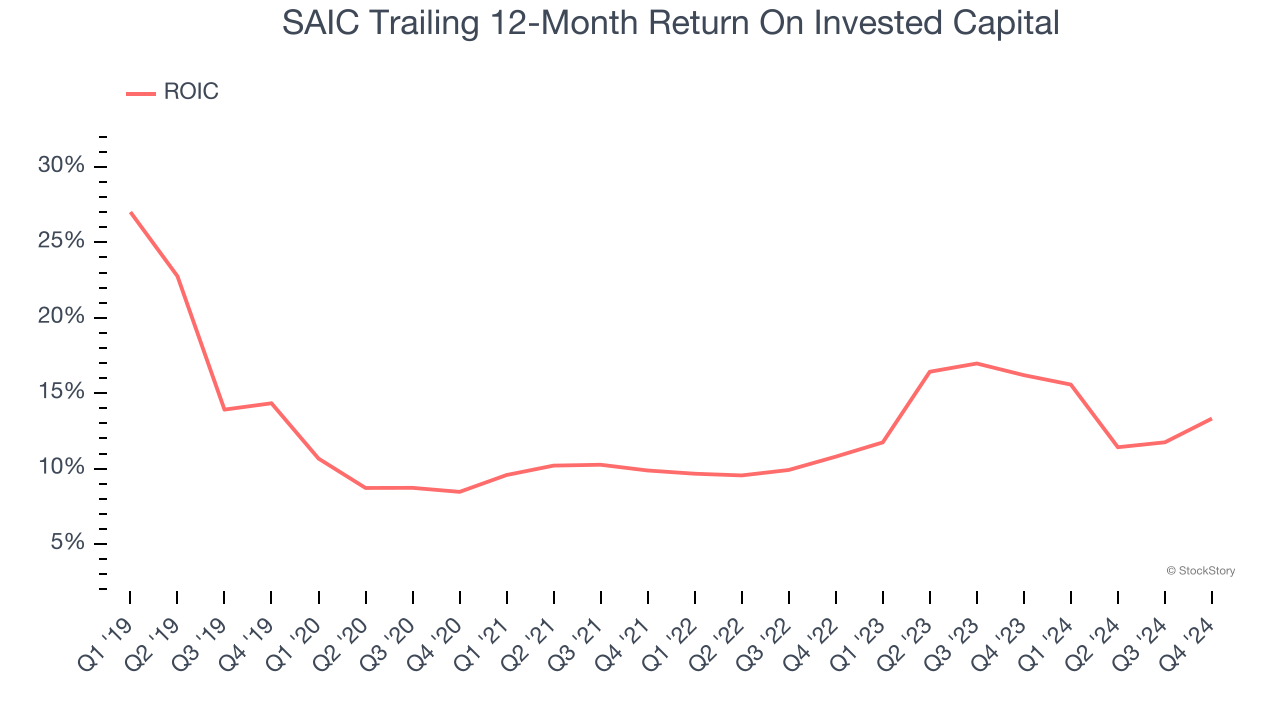

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

SAIC historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 11.7%, somewhat low compared to the best business services companies that consistently pump out 25%+.

Final Judgment

We see the value of companies helping consumers, but in the case of SAIC, we’re out. Following the recent decline, the stock trades at 13× forward P/E (or $115.71 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than SAIC

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today.