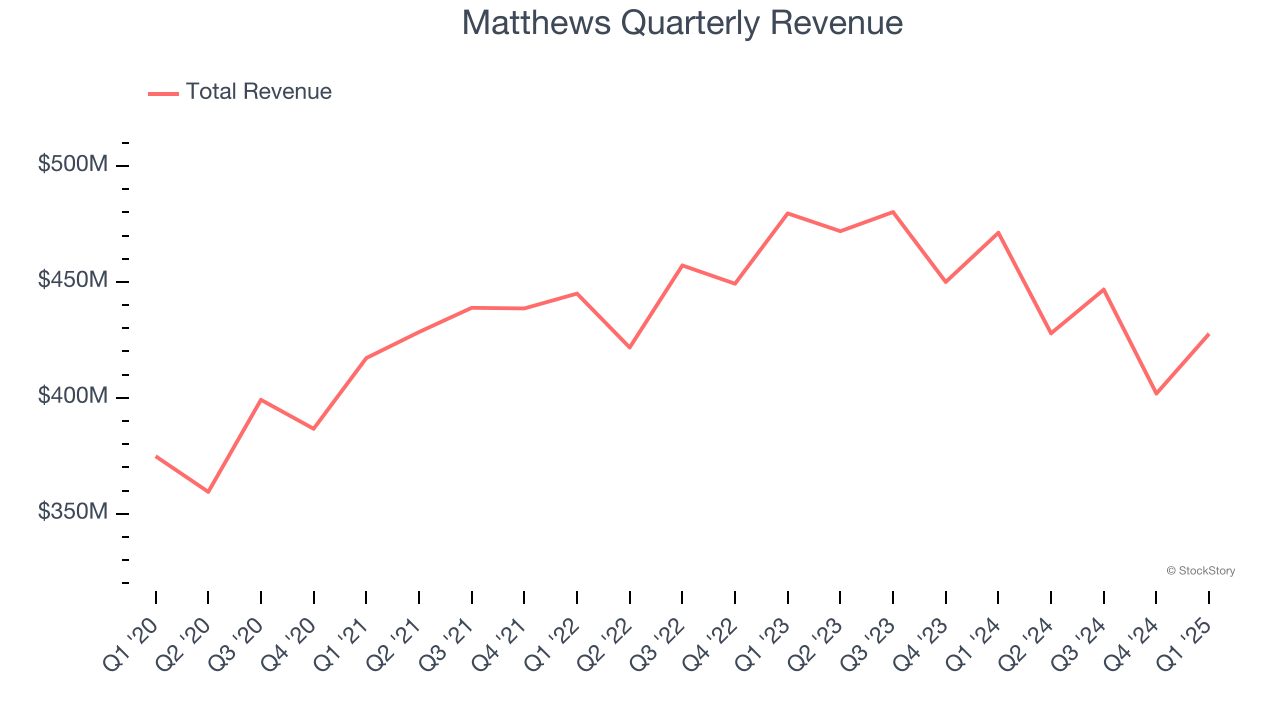

Diversified solutions provider Matthews International (NASDAQ: MATW) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 9.3% year on year to $427.6 million. Its non-GAAP profit of $0.34 per share was 10.5% below analysts’ consensus estimates.

Is now the time to buy Matthews? Find out by accessing our full research report, it’s free.

Matthews (MATW) Q1 CY2025 Highlights:

- Revenue: $427.6 million vs analyst estimates of $435.6 million (9.3% year-on-year decline, 1.8% miss)

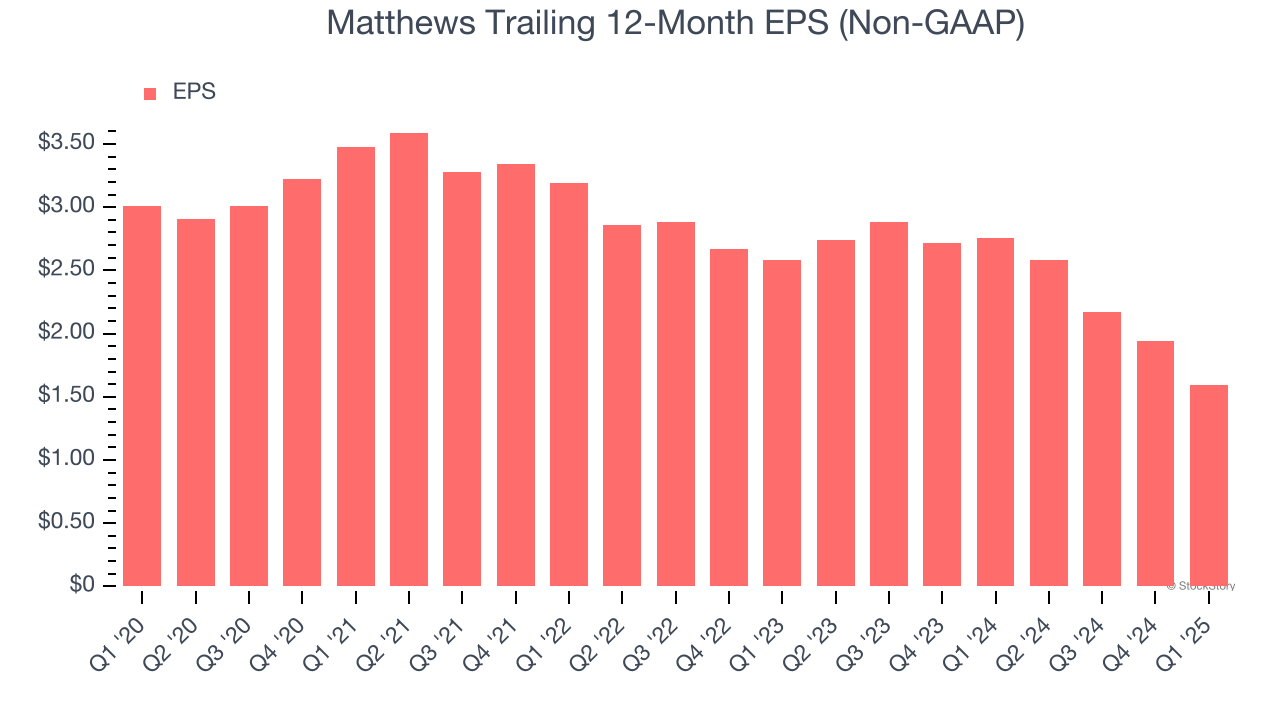

- Adjusted EPS: $0.34 vs analyst expectations of $0.38 (10.5% miss)

- Adjusted EBITDA: $51.4 million vs analyst estimates of $49.9 million (12% margin, 3% beat)

- EBITDA guidance for the full year is $190 million at the midpoint, below analyst estimates of $205.6 million

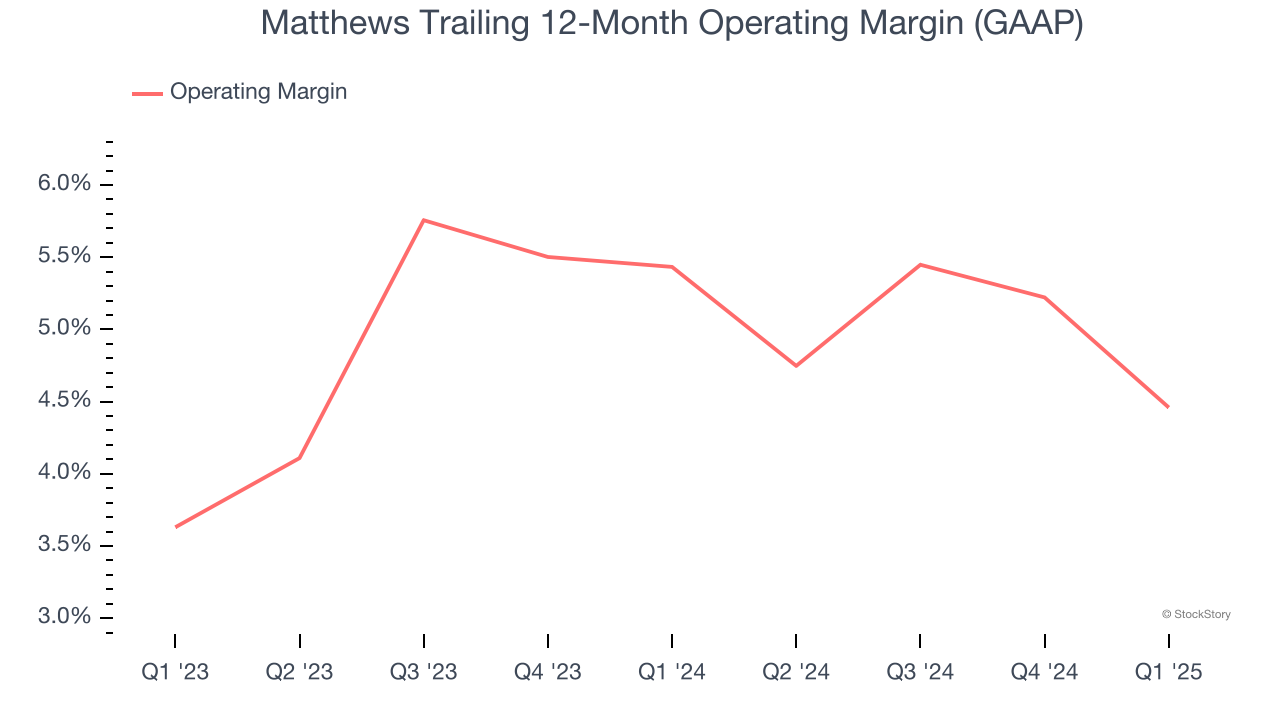

- Operating Margin: 1.4%, down from 4.5% in the same quarter last year

- Free Cash Flow was -$2.41 million, down from $47.15 million in the same quarter last year

- Market Capitalization: $665.2 million

Company Overview

Originally a death care company, Matthews International (NASDAQ: MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

Sales Growth

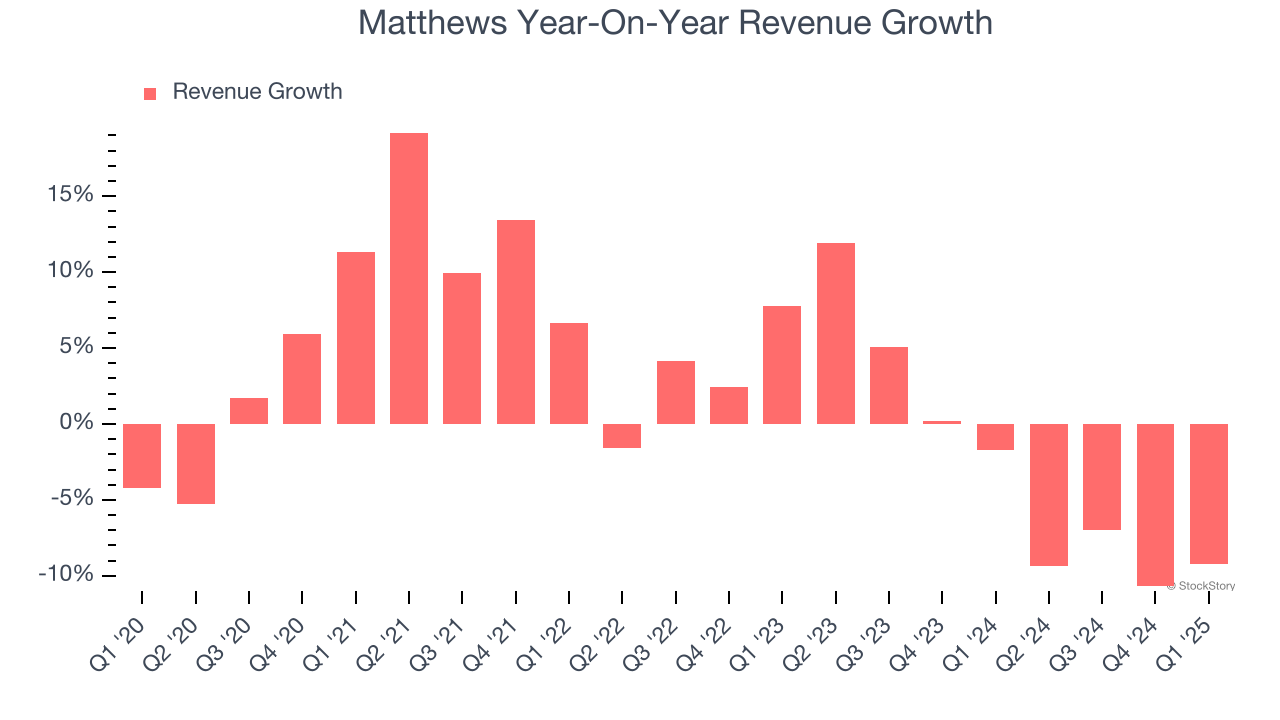

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Matthews’s sales grew at a weak 2.4% compounded annual growth rate over the last five years. This was below our standards and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Matthews’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.9% annually.

This quarter, Matthews missed Wall Street’s estimates and reported a rather uninspiring 9.3% year-on-year revenue decline, generating $427.6 million of revenue.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Matthews’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 5% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, Matthews generated an operating profit margin of 1.4%, down 3.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Matthews, its EPS declined by 12% annually over the last five years while its revenue grew by 2.4%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

In Q1, Matthews reported EPS at $0.34, down from $0.69 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Matthews’s Q1 Results

It was encouraging to see Matthews beat analysts’ revenue and EBITDA expectations this quarter. On the other hand, its EPS missed significantly and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.4% to $20.18 immediately after reporting.

Matthews’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.