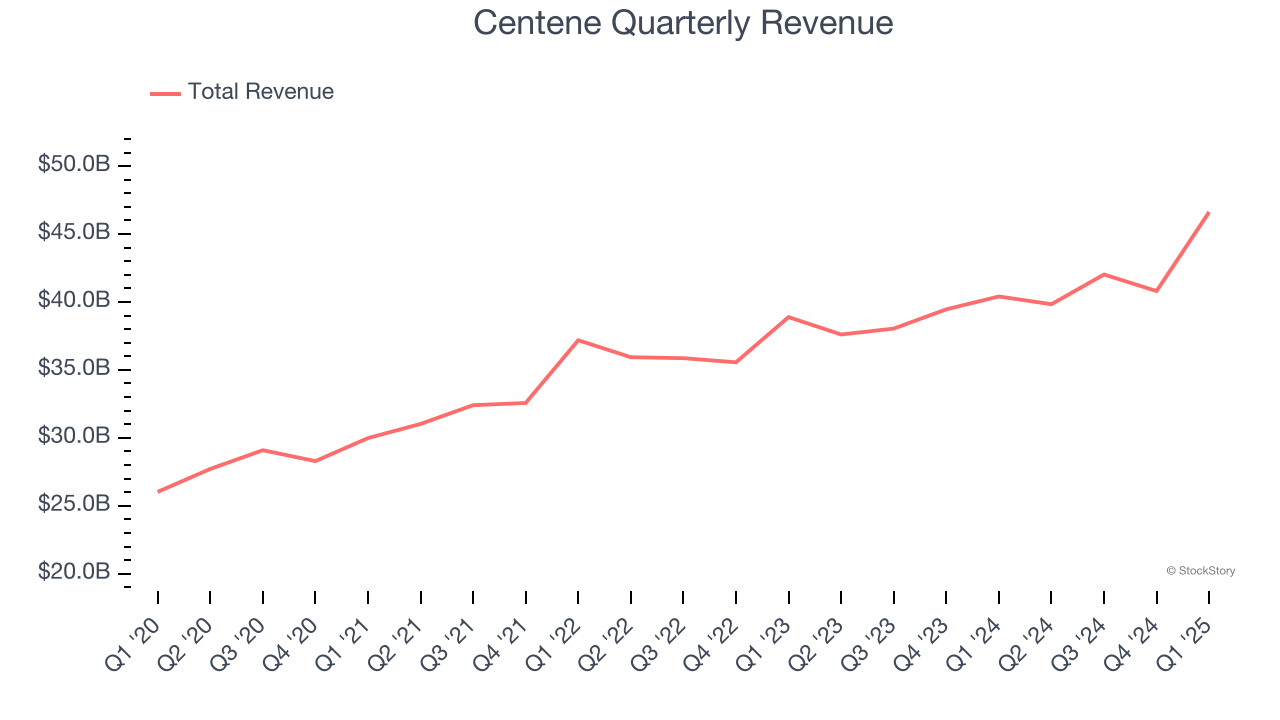

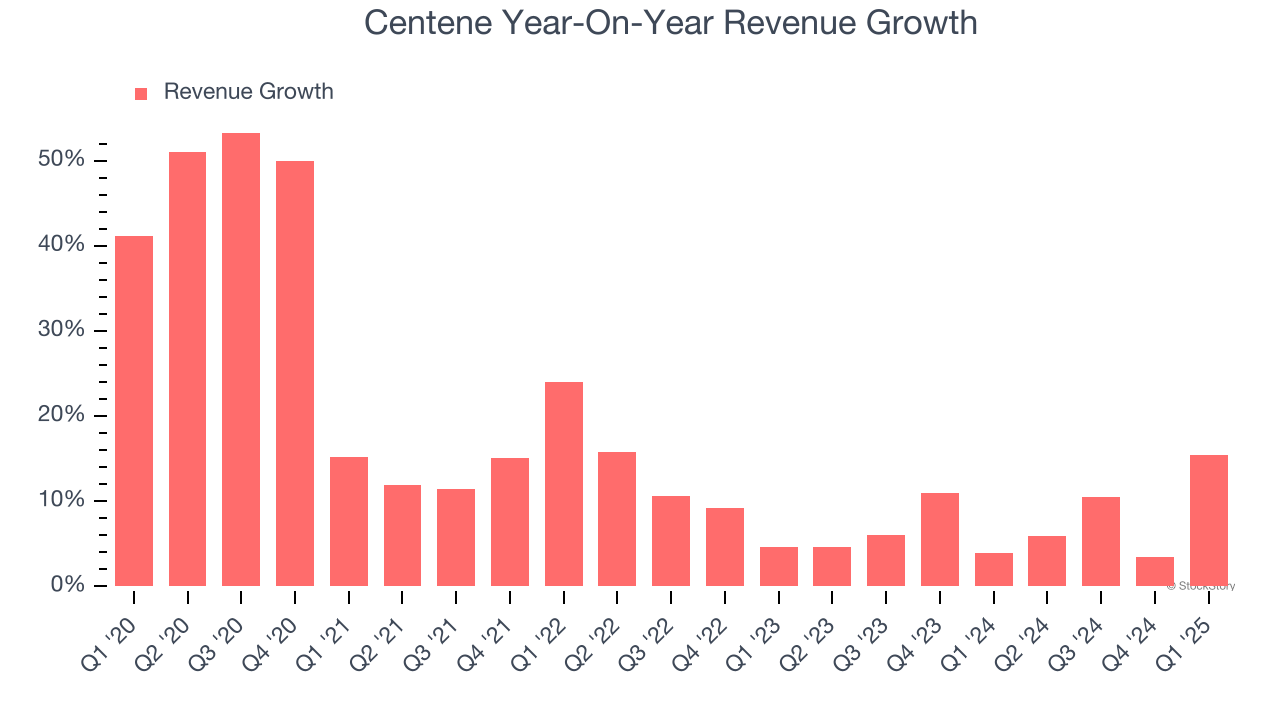

Health coverage company Centene (NYSE: CNC) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 15.4% year on year to $46.62 billion. The company’s full-year revenue guidance of $180 billion at the midpoint came in 4.2% above analysts’ estimates. Its non-GAAP profit of $2.90 per share was 15.3% above analysts’ consensus estimates.

Is now the time to buy Centene? Find out by accessing our full research report, it’s free.

Centene (CNC) Q1 CY2025 Highlights:

- Revenue: $46.62 billion vs analyst estimates of $43.03 billion (15.4% year-on-year growth, 8.3% beat)

- Adjusted EPS: $2.90 vs analyst estimates of $2.52 (15.3% beat)

- Adjusted EBITDA: $1.91 billion vs analyst estimates of $1.58 billion (4.1% margin, 20.9% beat)

- Management reiterated its full-year Adjusted EPS guidance of $7.25 at the midpoint

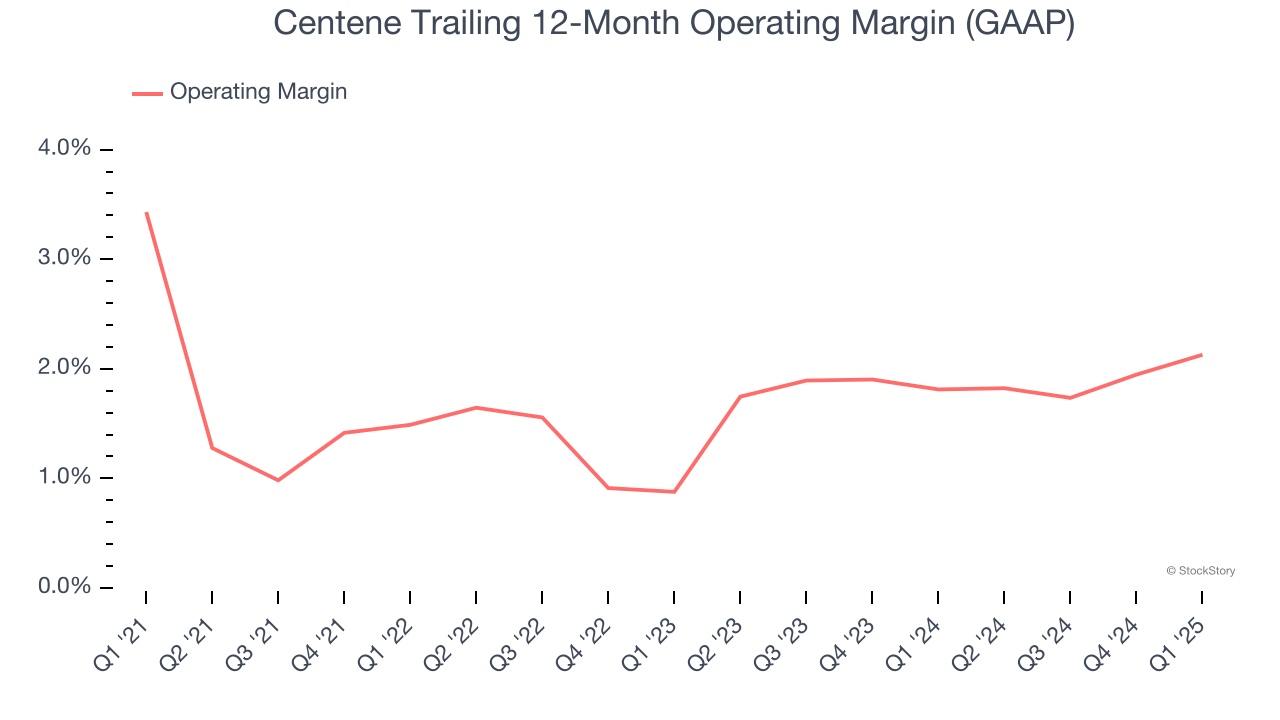

- Operating Margin: 3.3%, in line with the same quarter last year

- Free Cash Flow was $1.38 billion, up from -$607 million in the same quarter last year

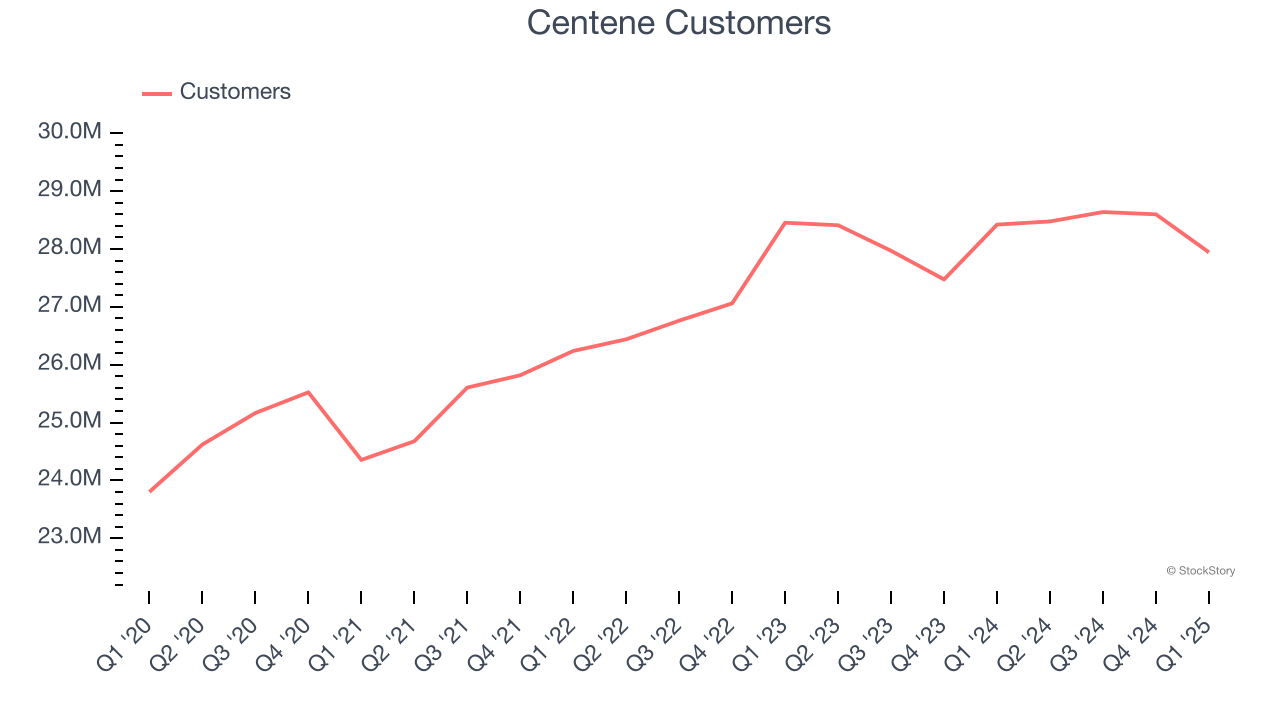

- Customers: 27.94 million, down from 28.6 million in the previous quarter

- Market Capitalization: $30.55 billion

"Our first quarter results demonstrate the resiliency of Centene's platform and the progress we are making as an organization while navigating a dynamic policy landscape," said Chief Executive Officer of Centene, Sarah M. London.

Company Overview

Serving nearly 1 in 15 Americans through its government healthcare programs, Centene (NYSE: CNC) is a healthcare company that manages government-sponsored health insurance programs like Medicaid and Medicare for low-income and complex-needs populations.

Health Insurance Providers

Upfront premiums collected by health insurers lead to reliable revenue, but profitability ultimately depends on accurate risk assessments and the ability to control medical costs. Health insurers are also highly sensitive to regulatory changes and economic conditions such as unemployment. Going forward, the industry faces tailwinds from an aging population, increasing demand for personalized healthcare services, and advancements in data analytics to improve cost management. However, continued regulatory scrutiny on pricing practices, the potential for government-led reforms such as expanded public healthcare options, and inflation in medical costs could add volatility to margins. One big debate among investors is the long-term impact of AI and whether it will help underwriting, fraud detection, and claims processing or whether it may wade into ethical grey areas like reinforcing biases and widening disparities in medical care.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Centene’s sales grew at a solid 15.5% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Centene’s annualized revenue growth of 7.6% over the last two years is below its five-year trend, but we still think the results were respectable.

We can dig further into the company’s revenue dynamics by analyzing its number of customers, which reached 27.94 million in the latest quarter. Over the last two years, Centene’s customer base averaged 2.3% year-on-year growth. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Centene reported year-on-year revenue growth of 15.4%, and its $46.62 billion of revenue exceeded Wall Street’s estimates by 8.3%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Centene was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.9% was weak for a healthcare business.

Analyzing the trend in its profitability, Centene’s operating margin decreased by 1.3 percentage points over the last five years, but it rose by 1.3 percentage points on a two-year basis. We like Centene and hope it can right the ship.

In Q1, Centene generated an operating profit margin of 3.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

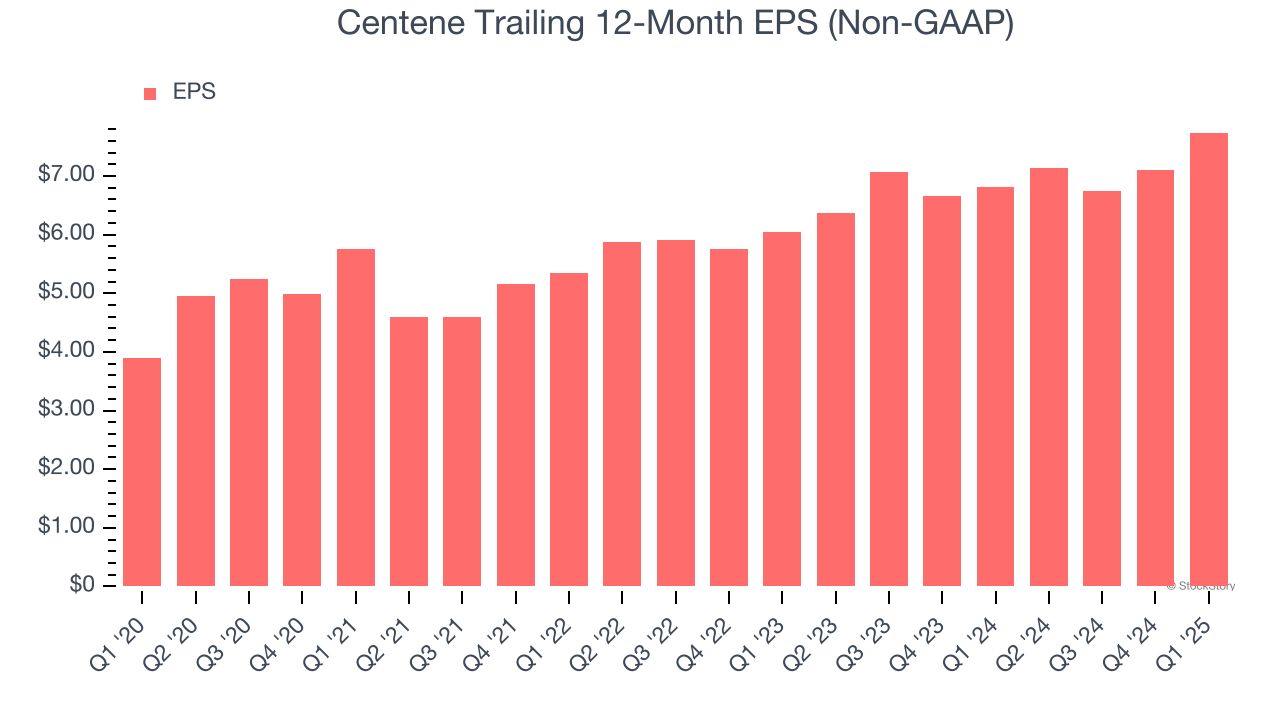

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Centene’s spectacular 14.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Centene reported EPS at $2.90, up from $2.26 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Centene’s full-year EPS of $7.74 to stay about the same.

Key Takeaways from Centene’s Q1 Results

We were impressed by how significantly Centene blew past analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. On the other hand, its customer base missed and its full-year EPS guidance fell slightly short of Wall Street’s estimates. Overall, we think this was a mixed quarter. The stock remained flat at $61.58 immediately after reporting.

Sure, Centene had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.