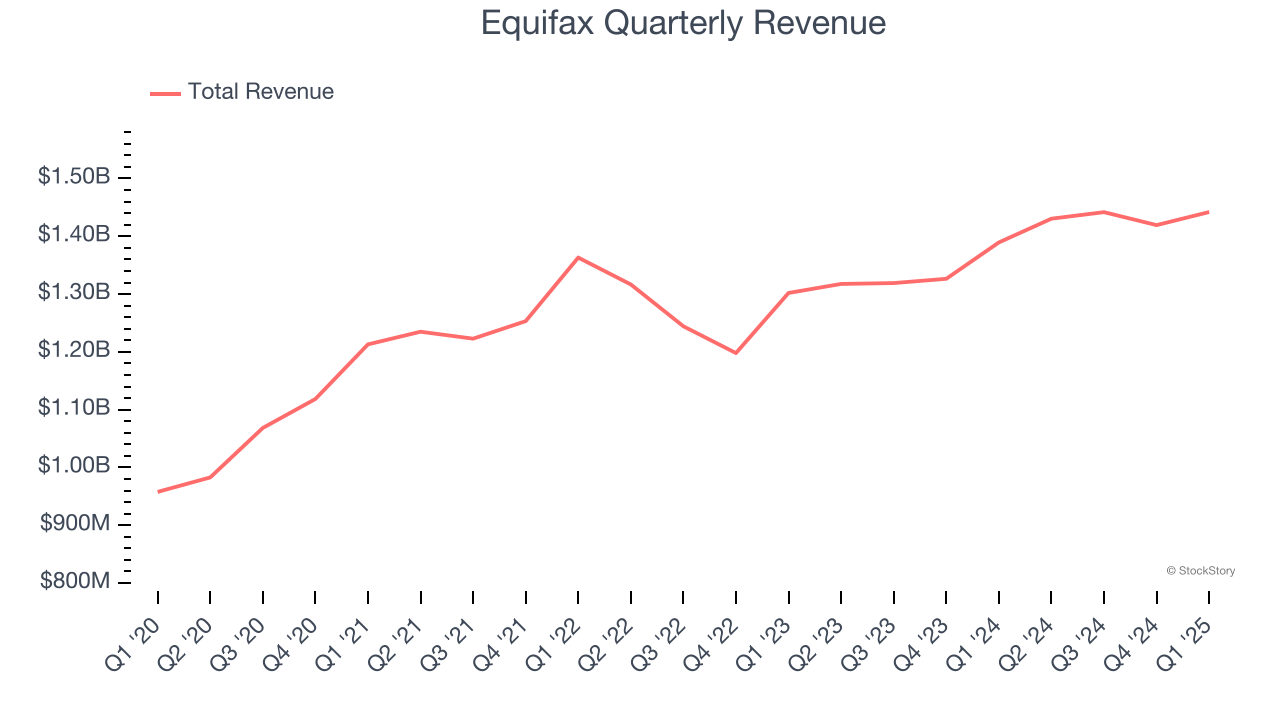

Credit reporting giant Equifax (NYSE: EFX) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, with sales up 3.8% year on year to $1.44 billion. Guidance for next quarter’s revenue was better than expected at $1.51 billion at the midpoint, 1.2% above analysts’ estimates. Its non-GAAP profit of $1.53 per share was 9% above analysts’ consensus estimates.

Is now the time to buy Equifax? Find out by accessing our full research report, it’s free.

Equifax (EFX) Q1 CY2025 Highlights:

- Revenue: $1.44 billion vs analyst estimates of $1.42 billion (3.8% year-on-year growth, 1.7% beat)

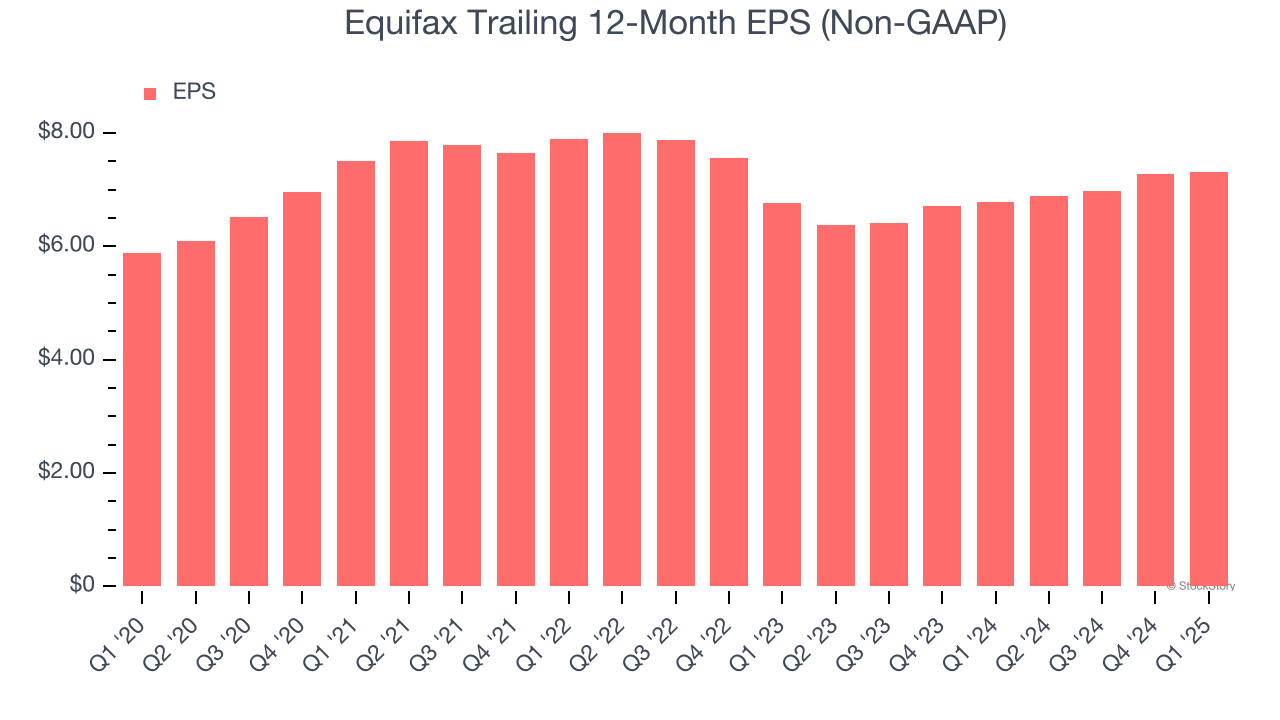

- Adjusted EPS: $1.53 vs analyst estimates of $1.40 (9% beat)

- Adjusted EBITDA: $423.1 million vs analyst estimates of $404.4 million (29.3% margin, 4.6% beat)

- The company slightly lifted its revenue guidance for the full year to $5.97 billion at the midpoint from $5.95 billion

- Management reiterated its full-year Adjusted EPS guidance of $7.45 at the midpoint

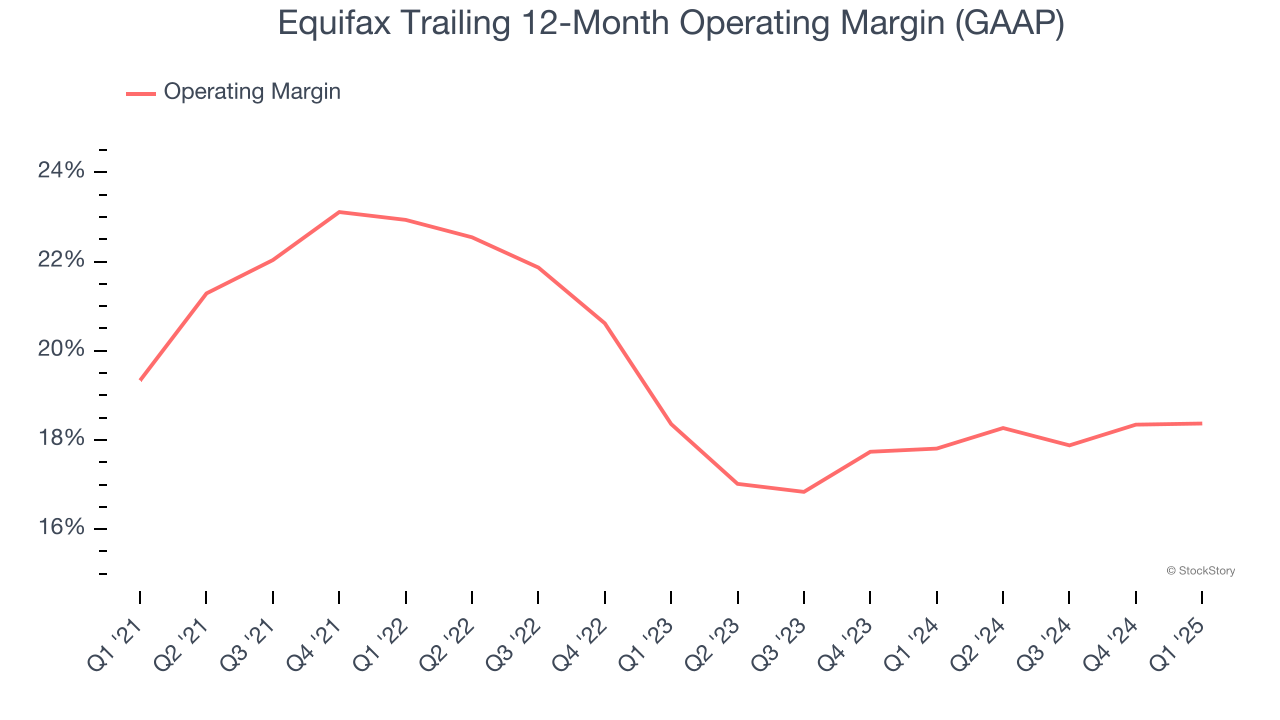

- Operating Margin: 16.4%, in line with the same quarter last year

- Free Cash Flow Margin: 8.1%, similar to the same quarter last year

- Market Capitalization: $26.87 billion

"Equifax delivered strong first quarter revenue of $1.442 billion, up 4% on a reported basis and 5% on a local currency basis that was $37 million above the mid-point of our February guidance, led by strong 7% U.S. Mortgage revenue growth and continued significant New Product Innovation performance with a Vitality Index of 11% despite headwinds from the U.S. Mortgage and Hiring markets. Workforce Solutions delivered 3% revenue growth, driven by Verification Services revenue growth of 5% led by Non-Mortgage revenue growth of 6% from strong growth in Talent Solutions and Consumer Lending businesses and better than expected Government growth. Mortgage revenue grew 3% despite continued weak Mortgage markets. USIS delivered strong revenue growth of over 7%, within their 6 to 8% Long Term Financial Framework. USIS revenue growth was led by very strong Mortgage revenue growth of 11% and Non-Mortgage revenue growth of 6%, led by strength in Card and Auto. International delivered strong 7% local currency revenue growth led by Latin America. We were pleased with the strong Equifax results in a challenging and uncertain market environment," said Mark W. Begor, Equifax Chief Executive Officer.

Company Overview

Holding detailed financial records on over 800 million consumers worldwide and dating back to 1899, Equifax (NYSE: EFX) is a global data analytics company that collects, analyzes, and sells consumer and business credit information to lenders, employers, and other businesses.

Data & Business Process Services

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $5.73 billion in revenue over the past 12 months, Equifax is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

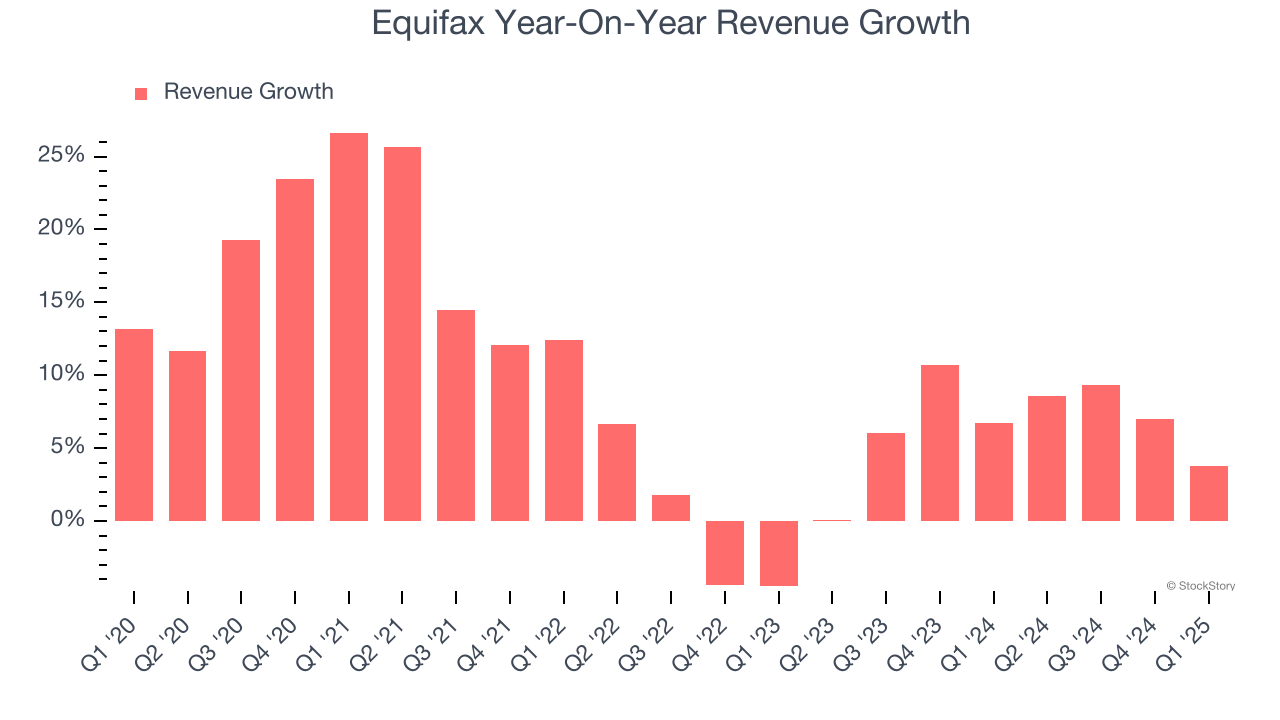

As you can see below, Equifax’s 9.5% annualized revenue growth over the last five years was impressive. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Equifax’s annualized revenue growth of 6.4% over the last two years is below its five-year trend, but we still think the results were respectable.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Workforce Solutions and U.S. Information Solutions, which are 42.9% and 34.7% of revenue. Over the last two years, Equifax’s Workforce Solutions revenue (HR services) averaged 4% year-on-year growth while its U.S. Information Solutions revenue (credit services) averaged 8.2% growth.

This quarter, Equifax reported modest year-on-year revenue growth of 3.8% but beat Wall Street’s estimates by 1.7%. Company management is currently guiding for a 5.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and implies its newer products and services will help support its recent top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Equifax has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 19.3%.

Looking at the trend in its profitability, Equifax’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Equifax generated an operating profit margin of 16.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Equifax’s EPS grew at an unimpressive 4.4% compounded annual growth rate over the last five years, lower than its 9.5% annualized revenue growth. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

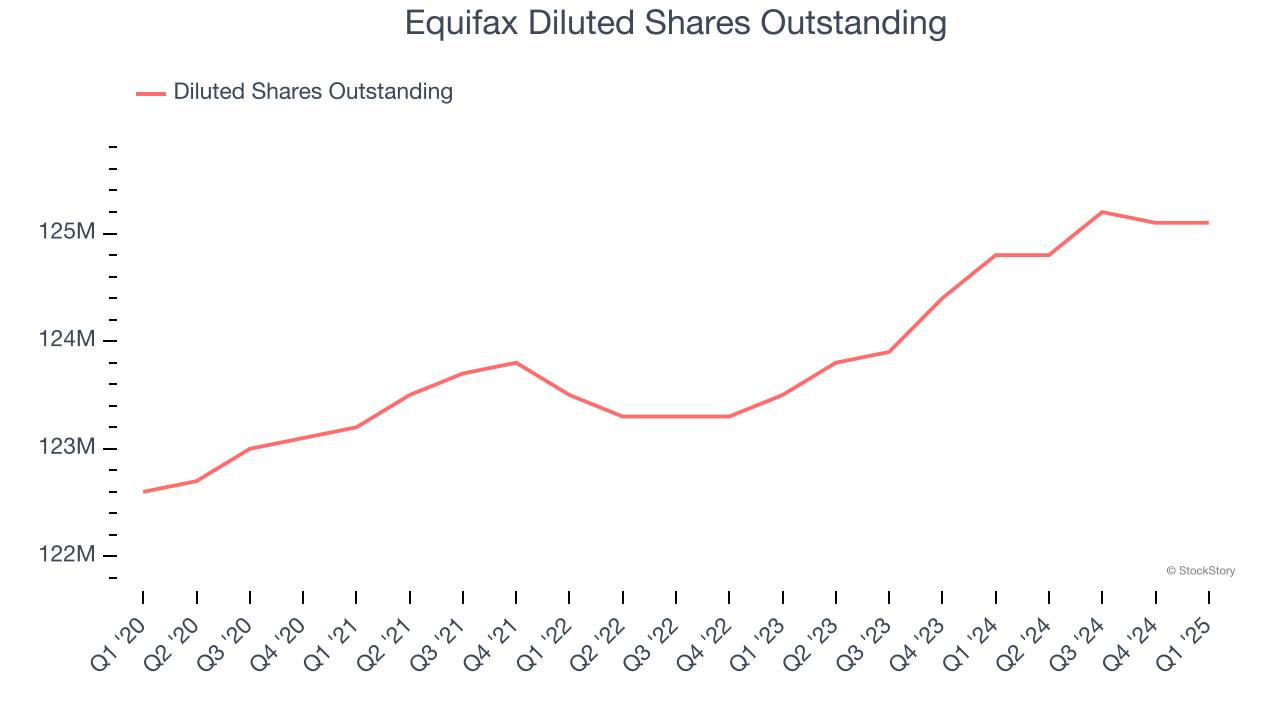

Diving into the nuances of Equifax’s earnings can give us a better understanding of its performance. A five-year view shows Equifax has diluted its shareholders, growing its share count by 2%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Equifax reported EPS at $1.53, up from $1.50 in the same quarter last year. This print beat analysts’ estimates by 9%. Over the next 12 months, Wall Street expects Equifax’s full-year EPS of $7.31 to grow 8.4%.

Key Takeaways from Equifax’s Q1 Results

We enjoyed seeing Equifax beat analysts’ EPS expectations this quarter. We were also glad its revenue guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance was in line. Overall, this quarter had some key positives. The stock traded up 4.2% to $224 immediately following the results.

Equifax may have had a good quarter, but does that mean you should invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.