Shareholders of Tri Pointe Homes would probably like to forget the past six months even happened. The stock dropped 29% and now trades at $31.31. This might have investors contemplating their next move.

Is there a buying opportunity in Tri Pointe Homes, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even with the cheaper entry price, we're swiping left on Tri Pointe Homes for now. Here are three reasons why you should be careful with TPH and a stock we'd rather own.

Why Do We Think Tri Pointe Homes Will Underperform?

Established in 2009 in California, Tri Pointe Homes (NYSE: TPH) is a United States homebuilder recognized for its innovative and sustainable approach to creating premium, life-enhancing homes.

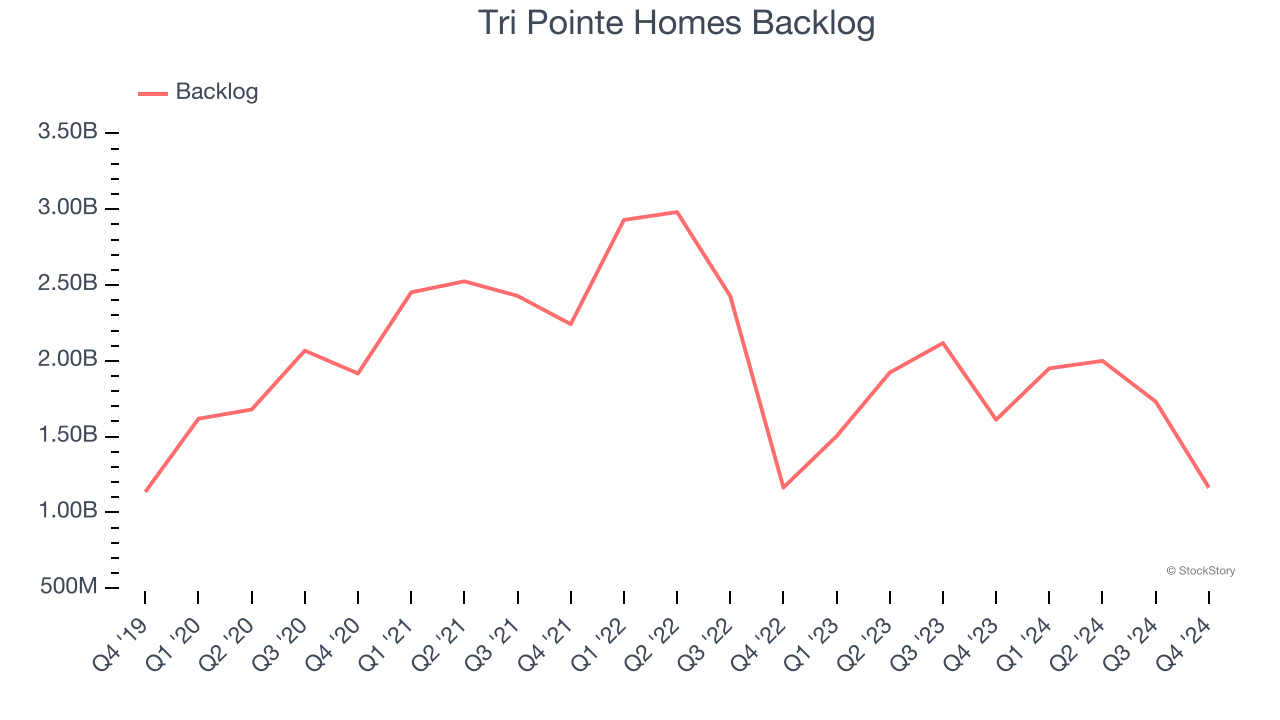

1. Backlog Declines as Orders Drop

We can better understand Home Builders companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Tri Pointe Homes’s future revenue streams.

Tri Pointe Homes’s backlog came in at $1.16 billion in the latest quarter, and it averaged 8.8% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Tri Pointe Homes’s revenue to drop by 14.5%, a decrease from its 1.6% annualized growth for the past two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

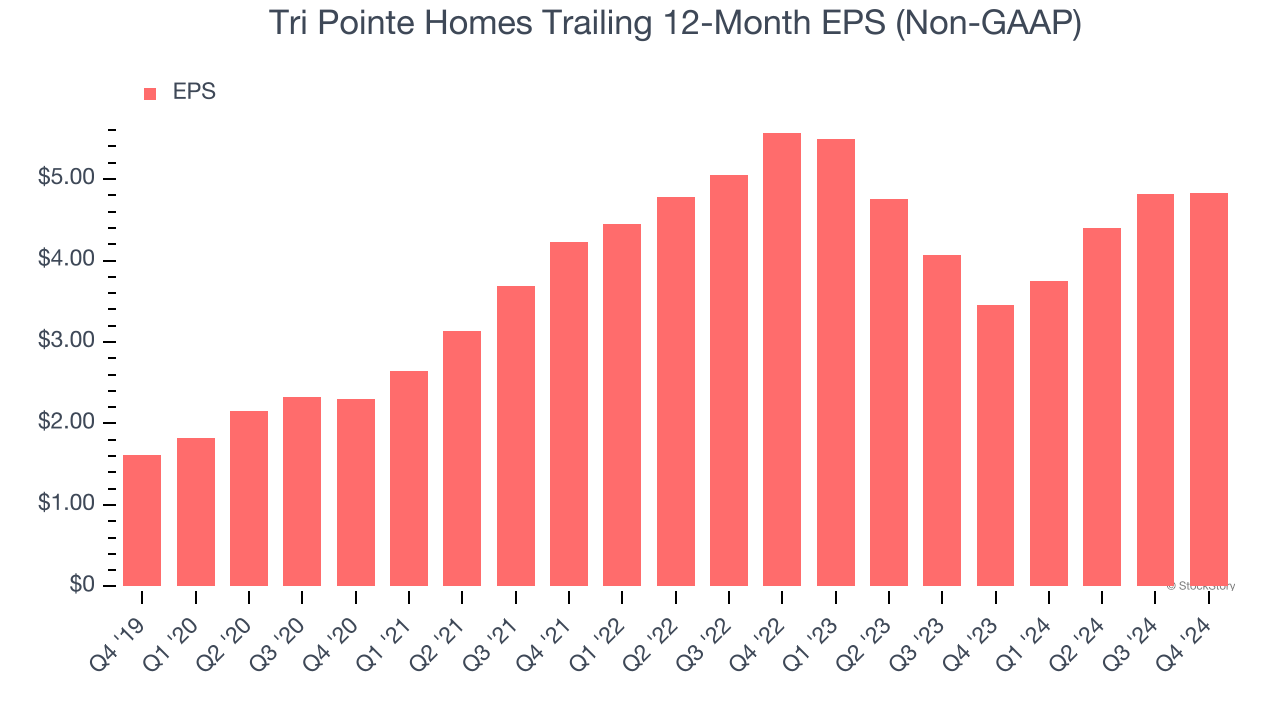

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Tri Pointe Homes, its EPS declined by 6.9% annually over the last two years while its revenue grew by 1.6%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

We see the value of companies helping their customers, but in the case of Tri Pointe Homes, we’re out. Following the recent decline, the stock trades at 7.2× forward price-to-earnings (or $31.31 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Tri Pointe Homes

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.