Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at Applied Industrial (NYSE: AIT) and its peers.

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 13 engineered components and systems stocks we track reported a satisfactory Q4. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 0.5% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.5% since the latest earnings results.

Applied Industrial (NYSE: AIT)

Formerly called The Ohio Ball Bearing Company, Applied Industrial (NYSE: AIT) distributes industrial products–everything from power tools to industrial valves–and services to a wide variety of industries.

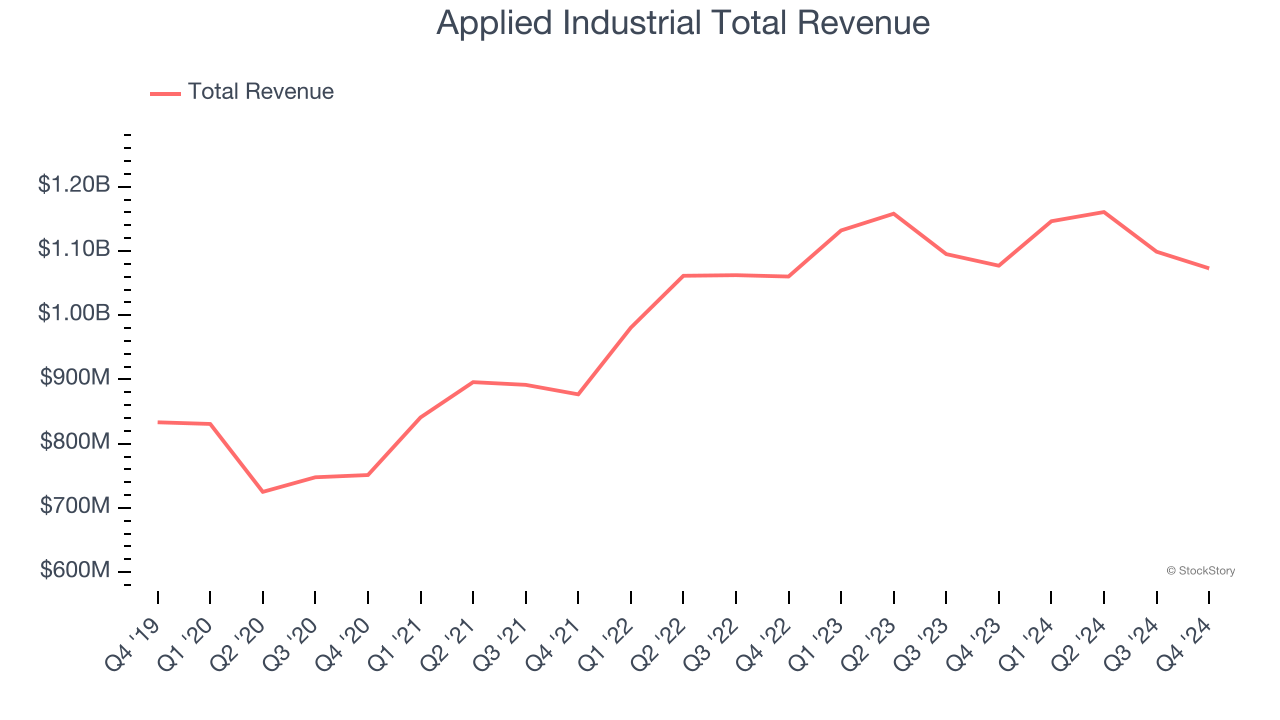

Applied Industrial reported revenues of $1.07 billion, flat year on year. This print was in line with analysts’ expectations, and overall, it was a strong quarter for the company with an impressive beat of analysts’ adjusted operating income estimates.

Neil A. Schrimsher, Applied’s President & Chief Executive Officer, commented, “Fiscal second quarter EBITDA and EPS exceeded our expectations, increasing a respective 3% and 7% year over year on relatively unchanged sales. Demand remained mixed during the quarter with seasonal factors and holiday timing limiting customer activity in December. That said, our team continued to execute well with organic sales trends inline with our guidance, while strong gross margin performance and cost controls drove solid EBITDA margin expansion during the quarter. Additionally, the closing of our Hydradyne acquisition at the end of December represents another notable milestone in our story and provides solid growth and operational momentum moving forward. Overall, we had a productive second quarter that highlights our business resilience, self-help opportunities, and favorable industry position.”

The stock is down 10% since reporting and currently trades at $226.61.

Is now the time to buy Applied Industrial? Access our full analysis of the earnings results here, it’s free.

Best Q4: ESCO (NYSE: ESE)

A developer of the communication systems used in the Batmobile of “The Dark Knight,” ESCO (NYSE: ESE) is a provider of engineered components for the aerospace, defense, and utility sectors.

ESCO reported revenues of $247 million, up 13.2% year on year, outperforming analysts’ expectations by 2.8%. The business had a stunning quarter with EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EPS estimates.

ESCO achieved the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 22.4% since reporting. It currently trades at $161.90.

Is now the time to buy ESCO? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Regal Rexnord (NYSE: RRX)

Headquartered in Milwaukee, Regal Rexnord (NYSE: RRX) provides power transmission and industrial automation products.

Regal Rexnord reported revenues of $1.46 billion, down 9.1% year on year, falling short of analysts’ expectations by 1.9%. It was a disappointing quarter as it posted full-year EPS guidance missing analysts’ expectations.

As expected, the stock is down 20.6% since the results and currently trades at $123.

Read our full analysis of Regal Rexnord’s results here.

Graham Corporation (NYSE: GHM)

Founded when its founder patented a unique design for a vacuum system used in the sugar refining process, Graham (NYSE: GHM) provides vacuum and heat transfer equipment for the energy, petrochemical, refining, and chemical sectors.

Graham Corporation reported revenues of $47.04 million, up 7.3% year on year. This number lagged analysts' expectations by 5%. Aside from that, it was a mixed quarter as it also produced an impressive beat of analysts’ EPS estimates but full-year revenue guidance slightly missing analysts’ expectations.

Graham Corporation had the weakest performance against analyst estimates and weakest full-year guidance update among its peers. The stock is down 34.2% since reporting and currently trades at $31.

Read our full, actionable report on Graham Corporation here, it’s free.

Mayville Engineering (NYSE: MEC)

Originally founded solely on tool and die manufacturing, Mayville Engineering Company (NYSE: MEC) specializes in metal fabrication, tube bending, and welding to be used in various industries.

Mayville Engineering reported revenues of $121.3 million, down 18.4% year on year. This print came in 2.3% below analysts' expectations. Overall, it was a slower quarter as it also logged full-year EBITDA guidance missing analysts’ expectations.

Mayville Engineering had the slowest revenue growth among its peers. The stock is up 1.6% since reporting and currently trades at $13.99.

Read our full, actionable report on Mayville Engineering here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.