Over the last six months, Quanta’s shares have sunk to $271.32, producing a disappointing 9% loss while the S&P 500 was flat. This might have investors contemplating their next move.

Following the drawdown, is now a good time to buy PWR? Find out in our full research report, it’s free.

Why Are We Positive On Quanta?

A construction engineering services company, Quanta (NYSE: PWR) provides infrastructure solutions to a variety of sectors, including energy and communications.

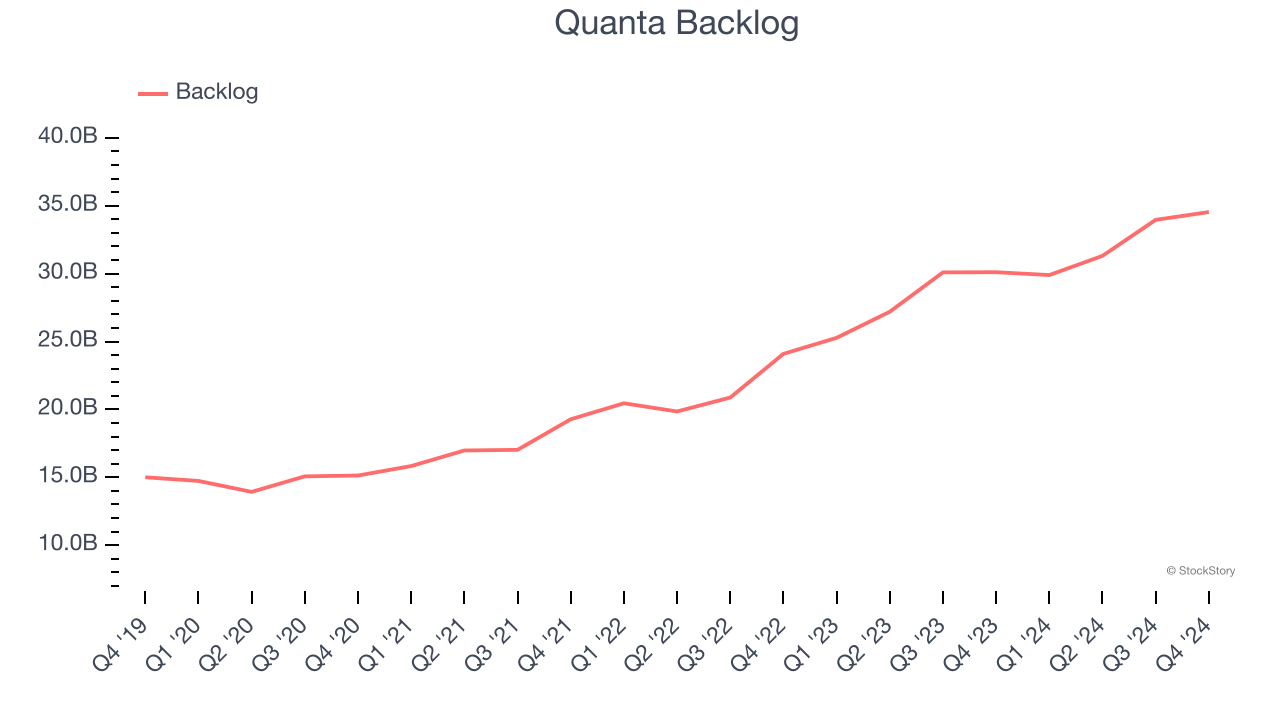

1. Surging Backlog Locks In Future Sales

We can better understand Energy Products and Services companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Quanta’s future revenue streams.

Quanta’s backlog punched in at $34.54 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 23.8%. This performance was fantastic and shows the company has a robust sales pipeline because it is accumulating more orders than it can fulfill. Its growth also suggests that customers are committing to Quanta for the long term, enhancing the business’s predictability.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Quanta’s revenue to rise by 13.5%. While this projection is below its 17.7% annualized growth rate for the past two years, it is particularly noteworthy for a company of its scale and implies the market is baking in success for its products and services.

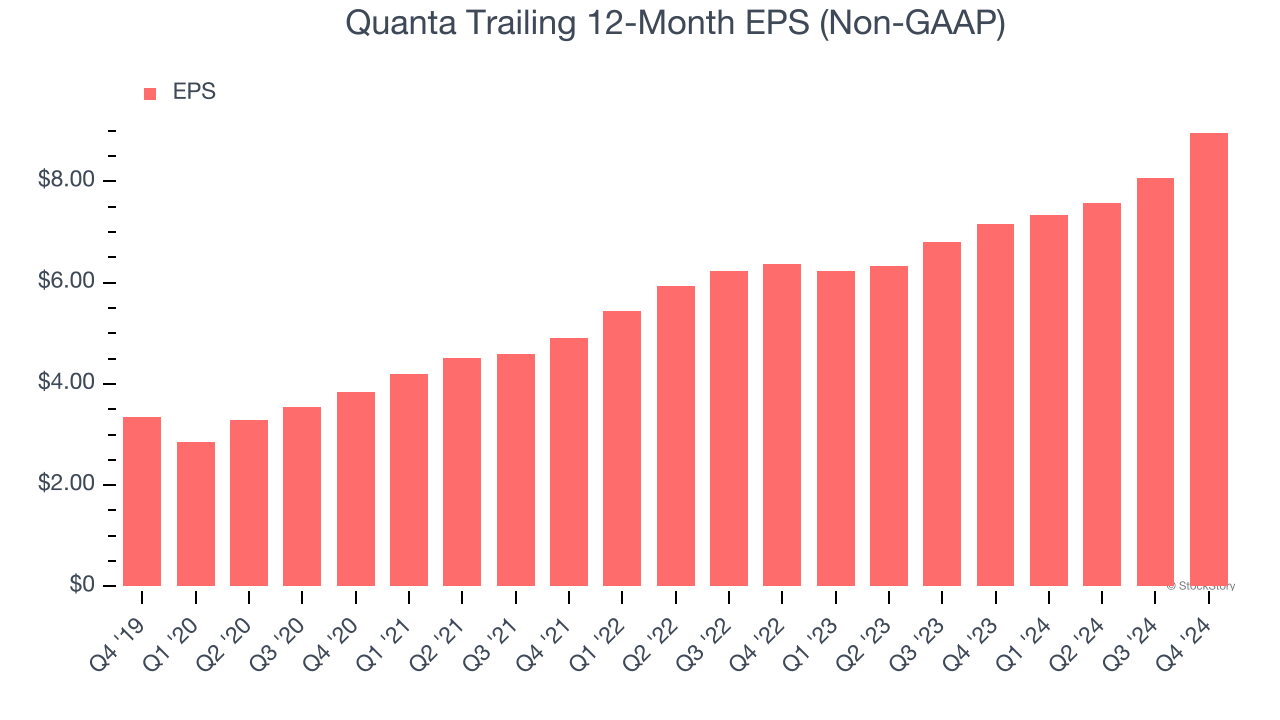

3. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Quanta’s EPS grew at an astounding 21.8% compounded annual growth rate over the last five years, higher than its 14.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we're bullish on Quanta. With the recent decline, the stock trades at 25.9× forward price-to-earnings (or $271.32 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Quanta

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.