UniFirst currently trades at $198 per share and has shown little upside over the past six months, posting a middling return of 4.4%.

Is there a buying opportunity in UniFirst, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We don't have much confidence in UniFirst. Here are three reasons why you should be careful with UNF and a stock we'd rather own.

Why Is UniFirst Not Exciting?

With a fleet of trucks making weekly deliveries to over 300,000 customer locations, UniFirst (NYSE: UNF) provides, rents, cleans, and maintains workplace uniforms and protective clothing for businesses across various industries.

1. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect UniFirst’s revenue to stall, a deceleration versus its 8.9% annualized growth for the past two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

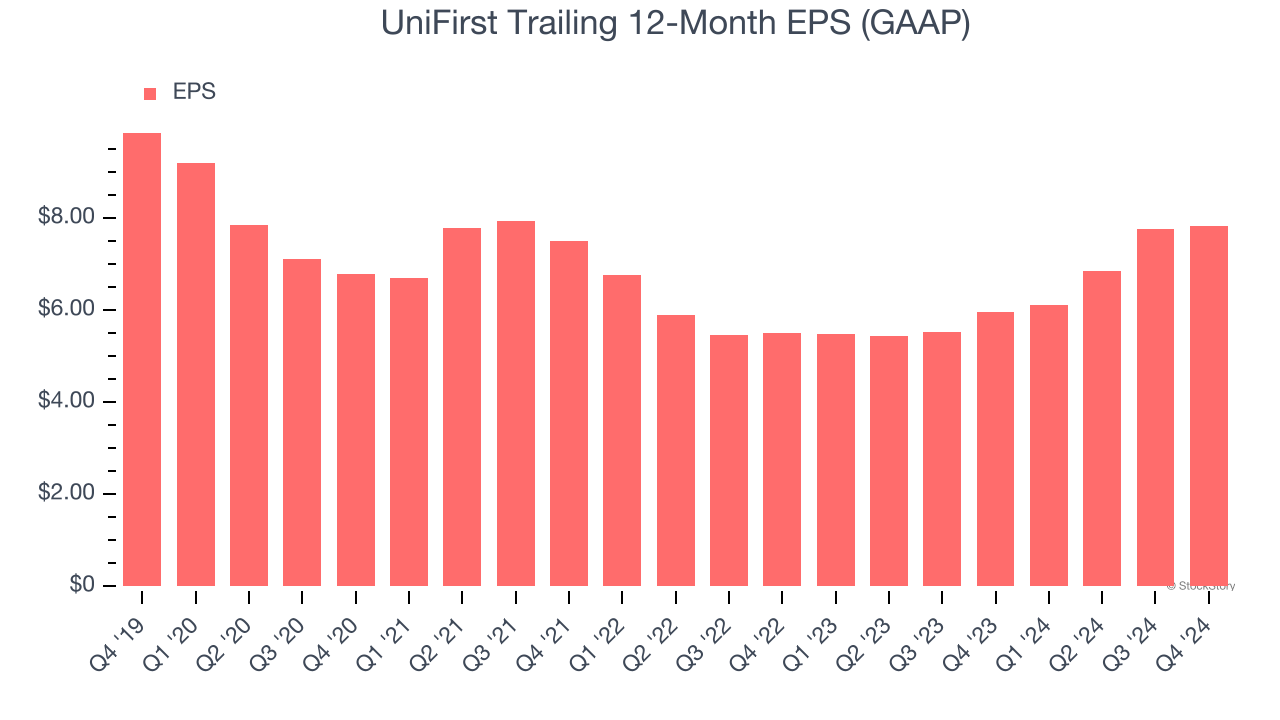

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for UniFirst, its EPS declined by 4.5% annually over the last five years while its revenue grew by 5.8%. This tells us the company became less profitable on a per-share basis as it expanded.

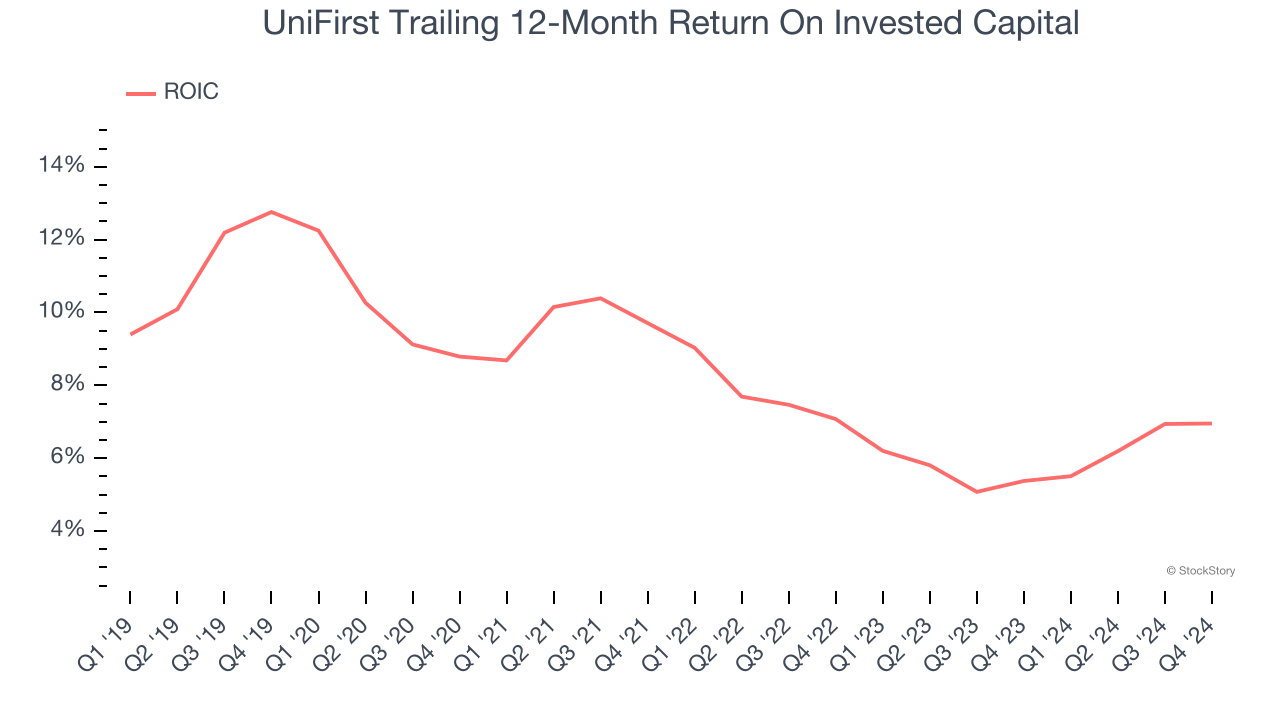

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

UniFirst historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.6%, somewhat low compared to the best business services companies that consistently pump out 25%+.

Final Judgment

UniFirst isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 25.6× forward price-to-earnings (or $198 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

Stocks We Would Buy Instead of UniFirst

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.