What a brutal six months it’s been for Omnicom Group. The stock has dropped 20.2% and now trades at $81.23, rattling many shareholders. This may have investors wondering how to approach the situation.

Is now the time to buy Omnicom Group, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even with the cheaper entry price, we're swiping left on Omnicom Group for now. Here are three reasons why you should be careful with OMC and a stock we'd rather own.

Why Is Omnicom Group Not Exciting?

With a vast network of creative agencies that helped craft some of the most memorable ad campaigns in history, Omnicom Group (NYSE: OMC) is a strategic holding company that provides advertising, marketing, and communications services to many of the world's largest companies.

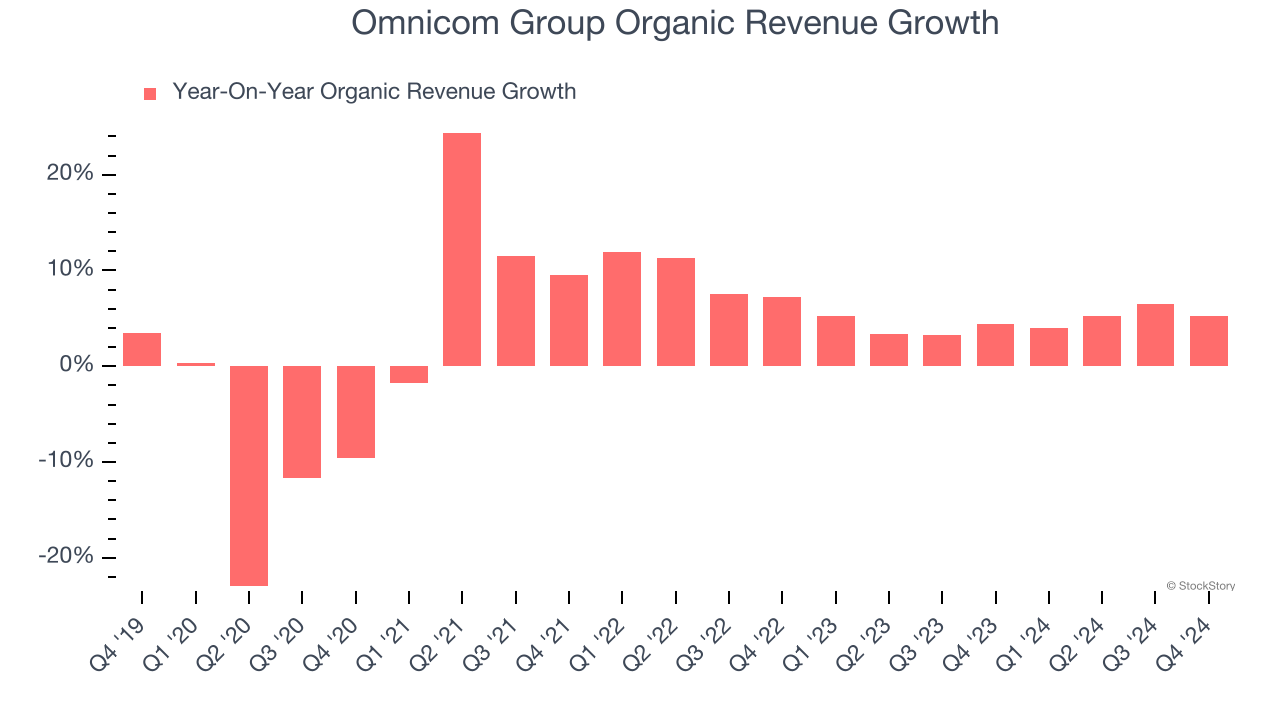

1. Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Advertising & Marketing Services companies should track organic revenue in addition to reported revenue. This metric gives visibility into Omnicom Group’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Omnicom Group’s organic revenue averaged 4.7% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

2. Free Cash Flow Margin Dropping

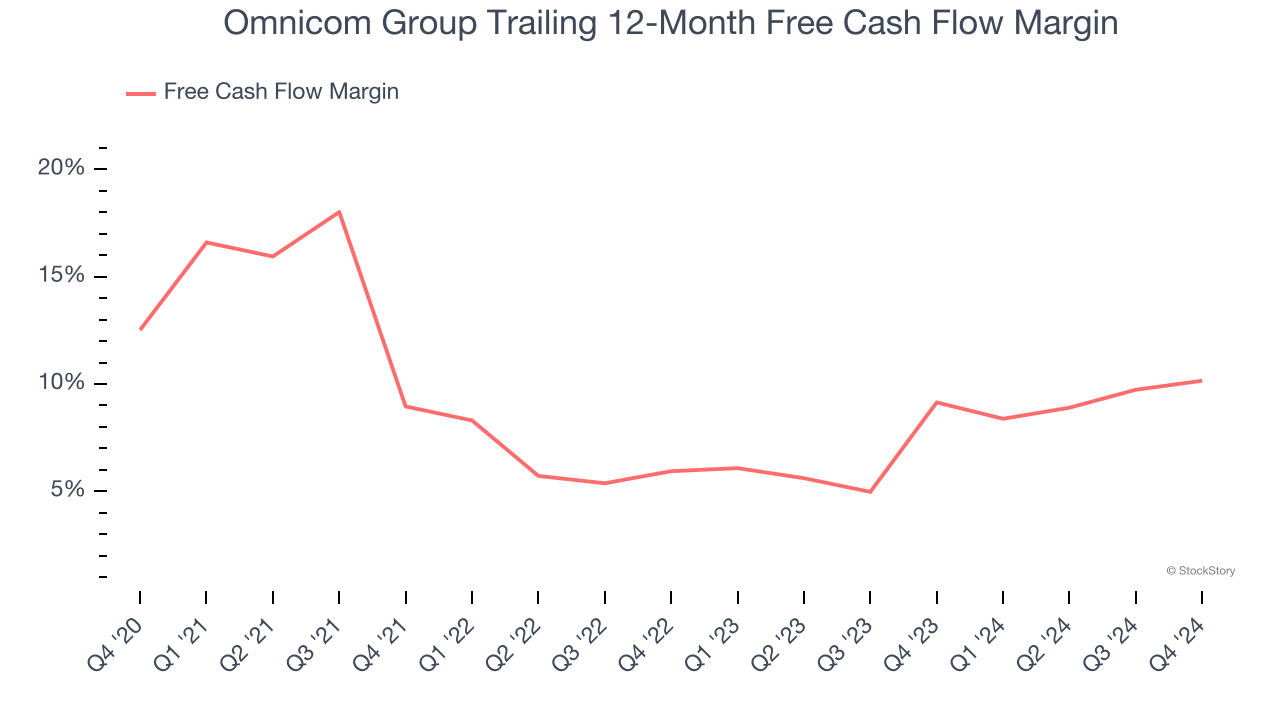

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Omnicom Group’s margin dropped by 2.4 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Omnicom Group’s free cash flow margin for the trailing 12 months was 10.2%.

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Omnicom Group’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Omnicom Group’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 9.5× forward price-to-earnings (or $81.23 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Omnicom Group

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.