Although the S&P 500 is down 1.4% over the past six months, Akamai’s stock price has fallen further to $81.54, losing shareholders 19% of their capital. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Akamai, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even with the cheaper entry price, we're swiping left on Akamai for now. Here are three reasons why there are better opportunities than AKAM and a stock we'd rather own.

Why Do We Think Akamai Will Underperform?

Founded in 1999 by two engineers from MIT, Akamai (NASDAQ: AKAM) provides software for organizations to efficiently deliver web content to their customers.

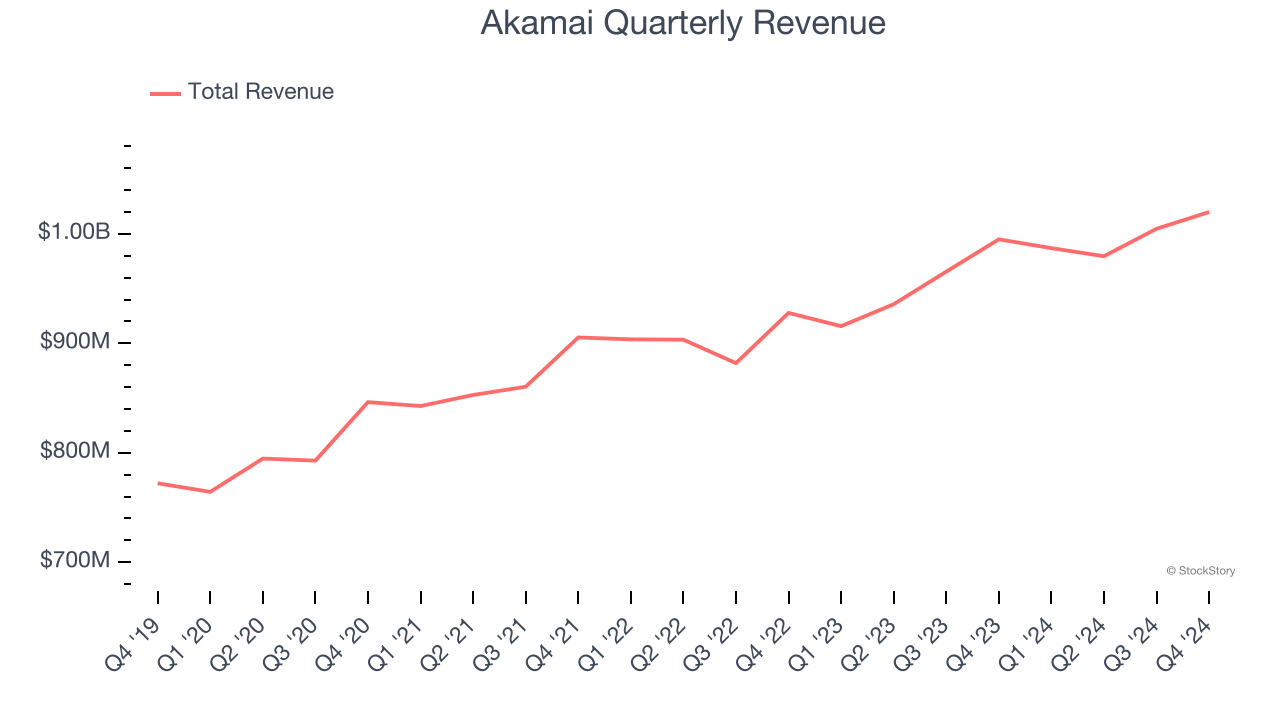

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Akamai’s sales grew at a weak 4.9% compounded annual growth rate over the last three years. This fell short of our benchmark for the software sector.

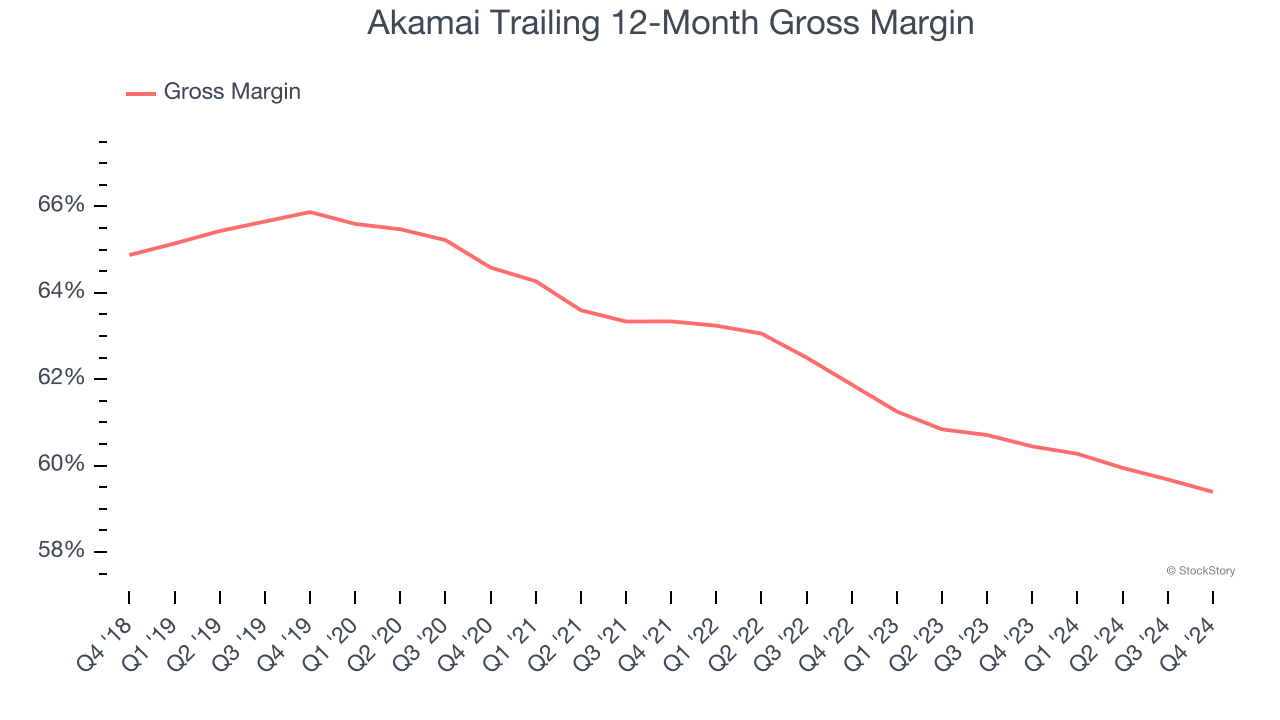

2. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Akamai, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Akamai’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 59.4% gross margin over the last year. Said differently, Akamai had to pay a chunky $40.61 to its service providers for every $100 in revenue.

3. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Akamai’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Akamai’s products and its peers.

Final Judgment

Akamai doesn’t pass our quality test. After the recent drawdown, the stock trades at 3× forward price-to-sales (or $81.54 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Akamai

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.