What a brutal six months it’s been for Regeneron. The stock has dropped 39.3% and now trades at $662.80, rattling many shareholders. This might have investors contemplating their next move.

Is there a buying opportunity in Regeneron, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the more favorable entry price, we don't have much confidence in Regeneron. Here are three reasons why you should be careful with REGN and a stock we'd rather own.

Why Is Regeneron Not Exciting?

Founded by scientists who wanted to build a company where science could thrive, Regeneron Pharmaceuticals (NASDAQ: REGN) develops and commercializes medicines for serious diseases, with key products treating eye conditions, allergic diseases, cancer, and other disorders.

1. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Regeneron’s revenue to rise by 1.7%, a deceleration versus its 8% annualized growth for the past two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

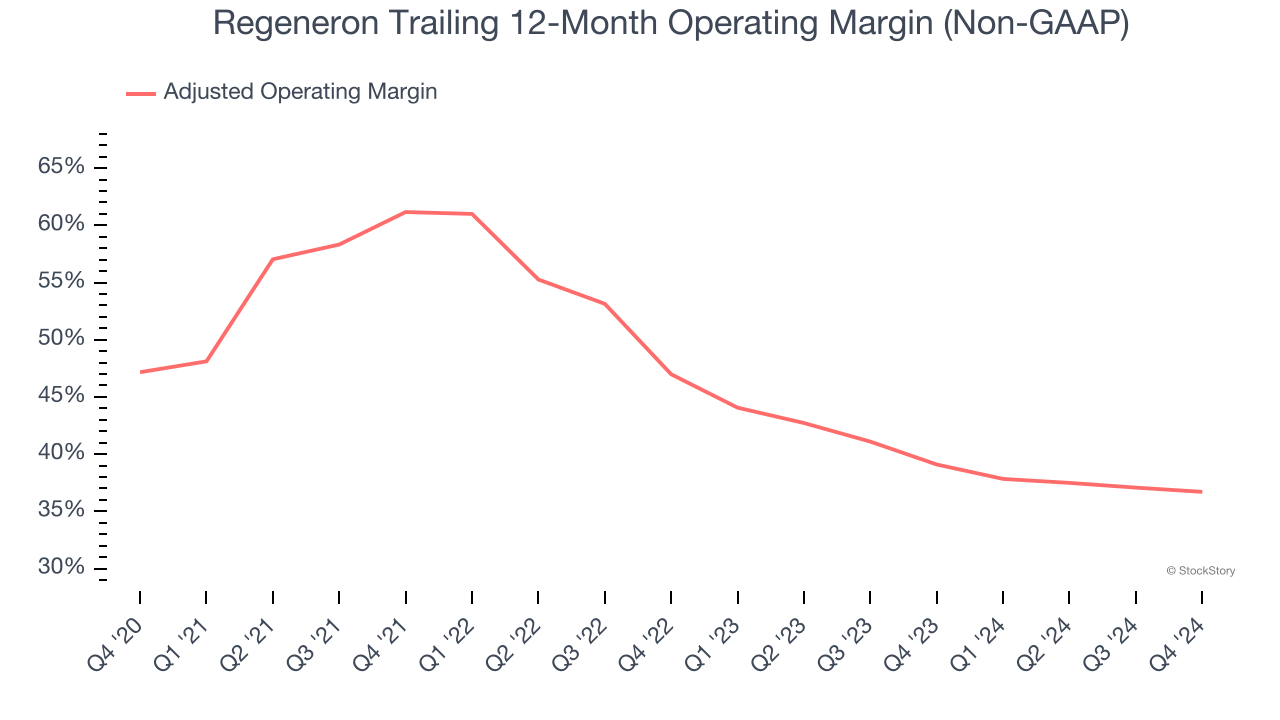

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Analyzing the trend in its profitability, Regeneron’s adjusted operating margin decreased by 10.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 36.7%.

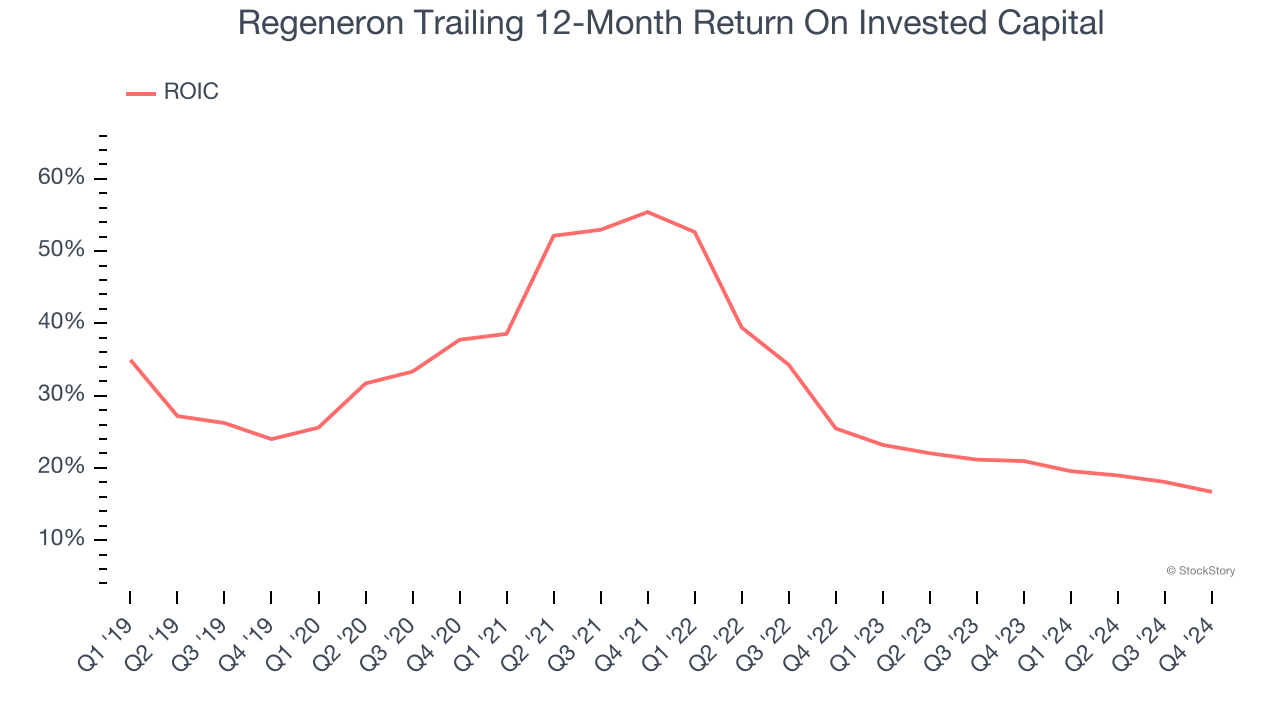

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Regeneron’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Regeneron isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 14.6× forward price-to-earnings (or $662.80 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Regeneron

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.