Looking back on heavy transportation equipment stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Trinity (NYSE: TRN) and its peers.

Heavy transportation equipment companies are investing in automated vehicles that increase efficiencies and connected machinery that collects actionable data. Some are also developing electric vehicles and mobility solutions to address customers’ concerns about carbon emissions, creating new sales opportunities. Additionally, they are increasingly offering automated equipment that increases efficiencies and connected machinery that collects actionable data. On the other hand, heavy transportation equipment companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the construction and transport volumes that drive demand for these companies’ offerings.

The 14 heavy transportation equipment stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.5%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.1% since the latest earnings results.

Trinity (NYSE: TRN)

Operating under the trade name TrinityRail, Trinity (NYSE: TRN) is a provider of railcar products and services in North America.

Trinity reported revenues of $629.4 million, down 21.1% year on year. This print exceeded analysts’ expectations by 6.8%. Overall, it was an exceptional quarter for the company with full-year EPS guidance exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

“Trinity Industries’ 2024 full year adjusted EPS of $1.82 represents a 32% increase over 2023, driven by higher lease rates, significantly improved margin performance, and a higher volume of external repairs. I extend my gratitude to the Trinity team for their outstanding efforts this year,” stated Trinity’s Chief Executive Officer and President Jean Savage.

The stock is down 12.8% since reporting and currently trades at $29.81.

Is now the time to buy Trinity? Access our full analysis of the earnings results here, it’s free.

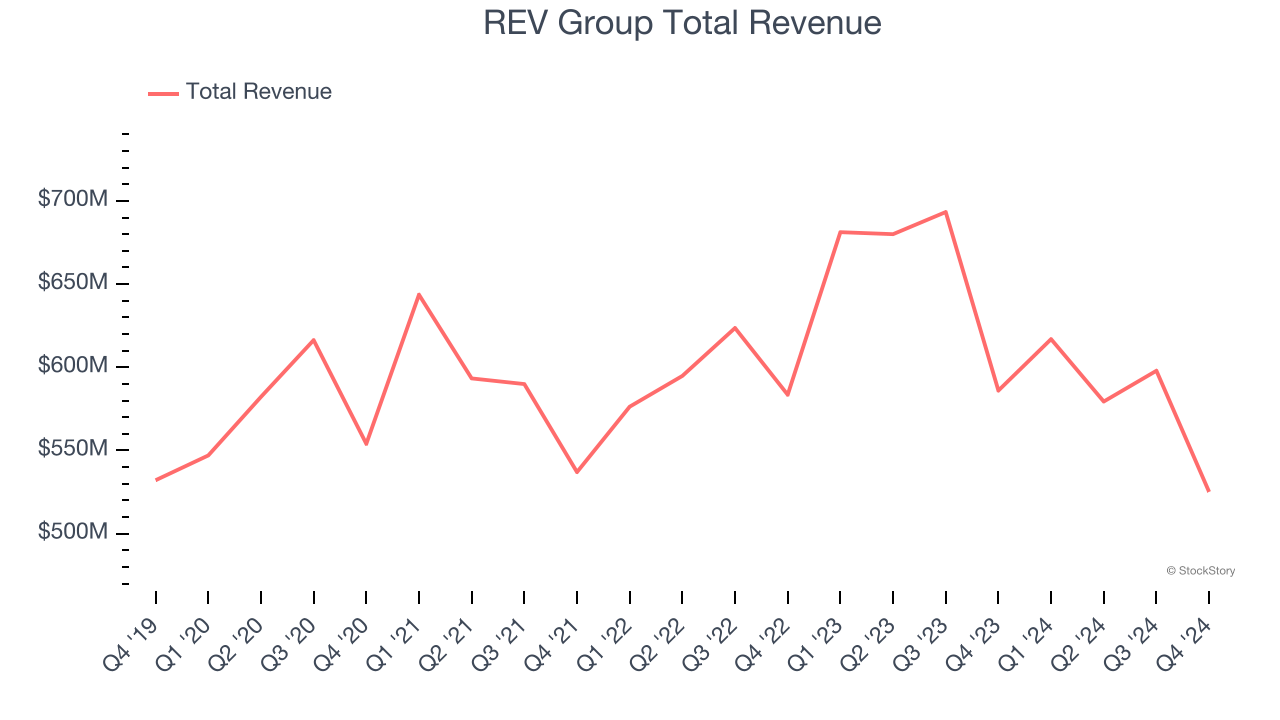

Best Q4: REV Group (NYSE: REVG)

Offering the first full-electric North American fire truck, REV (NYSE: REVG) manufactures and sells specialty vehicles.

REV Group reported revenues of $525.1 million, down 10.4% year on year, outperforming analysts’ expectations by 6.5%. The business had an incredible quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 19.2% since reporting. It currently trades at $32.53.

Is now the time to buy REV Group? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Wabtec (NYSE: WAB)

Also known as Wabtec, Westinghouse Air Brake Technologies (NYSE: WAB) provides equipment, systems, and related software for the railway industry.

Wabtec reported revenues of $2.58 billion, up 2.3% year on year, falling short of analysts’ expectations by 0.6%. It was a softer quarter as it posted a significant miss of analysts’ EBITDA estimates.

As expected, the stock is down 10.1% since the results and currently trades at $186.90.

Read our full analysis of Wabtec’s results here.

Cummins (NYSE: CMI)

With more than half of the heavy-duty truck market using its engines at one point, Cummins (NYSE: CMI) offers engines and power systems.

Cummins reported revenues of $8.45 billion, down 1.1% year on year. This result beat analysts’ expectations by 4.7%. Overall, it was a stunning quarter as it also logged a solid beat of analysts’ adjusted operating income estimates and an impressive beat of analysts’ Engine revenue estimates.

The stock is down 5.4% since reporting and currently trades at $329.37.

Read our full, actionable report on Cummins here, it’s free.

Greenbrier (NYSE: GBX)

Having designed the industry’s first double-decker railcar in the 1980s, Greenbrier (NYSE: GBX) supplies the freight rail transportation industry with railcars and related services.

Greenbrier reported revenues of $875.9 million, up 8.3% year on year. This print surpassed analysts’ expectations by 3.1%. It was a strong quarter as it also recorded an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Greenbrier delivered the fastest revenue growth among its peers. The stock is down 10.2% since reporting and currently trades at $54.30.

Read our full, actionable report on Greenbrier here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.