Looking back on electronic components & manufacturing stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Flex (NASDAQ: FLEX) and its peers.

The sector could see higher demand as the prevalence of advanced electronics increases in industries such as automotive, healthcare, aerospace, and computing. The high-performance components and contract manufacturing expertise required for autonomous vehicles and cloud computing datacenters, for instance, will benefit companies in the space. However, headwinds include geopolitical risks, particularly U.S.-China trade tensions that could disrupt component sourcing and production as the Trump administration takes an increasingly antagonizing stance on foreign relations. Additionally, stringent environmental regulations on e-waste and emissions could force the industry to pivot in potentially costly ways.

The 9 electronic components & manufacturing stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.4% while next quarter’s revenue guidance was 1.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.2% since the latest earnings results.

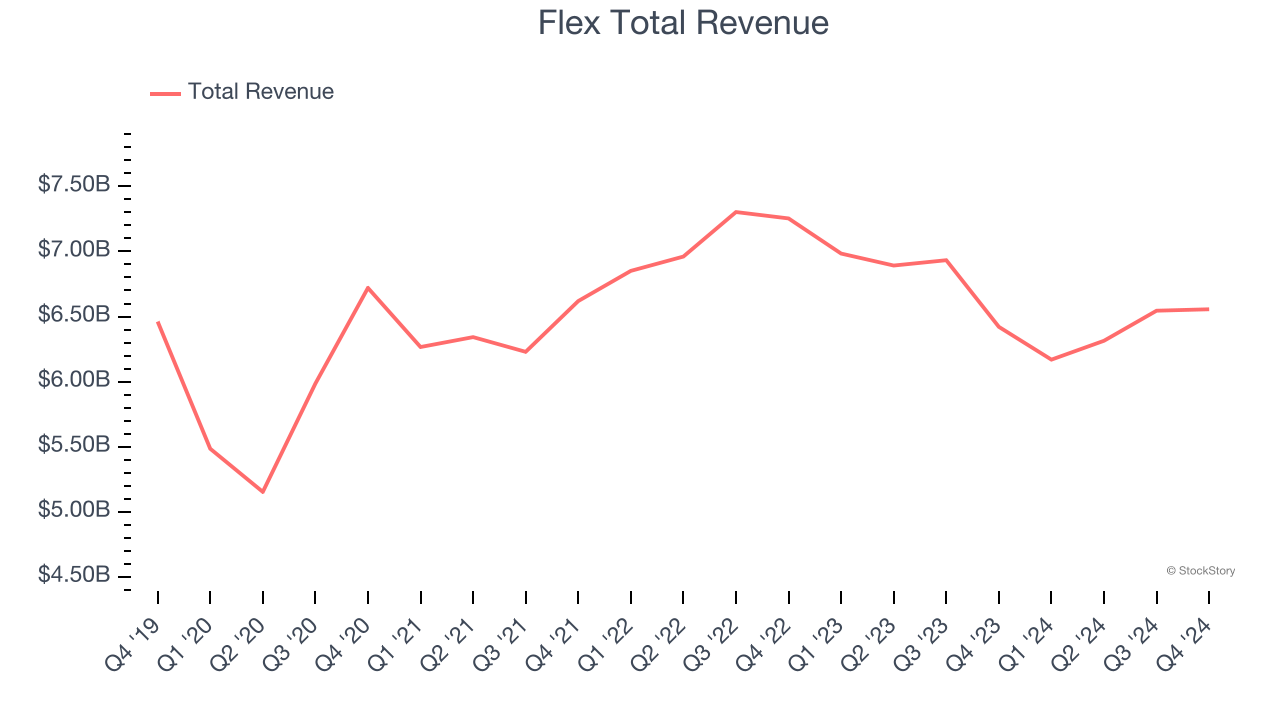

Best Q4: Flex (NASDAQ: FLEX)

Originally known as Flextronics until its 2016 rebranding, Flex (NASDAQ: FLEX) is a global manufacturing partner that designs, engineers, and builds products for companies across industries from medical devices to solar trackers.

Flex reported revenues of $6.56 billion, up 2.1% year on year. This print exceeded analysts’ expectations by 5.7%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ EPS estimates.

Flex pulled off the highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 9.6% since reporting and currently trades at $36.74.

Is now the time to buy Flex? Access our full analysis of the earnings results here, it’s free.

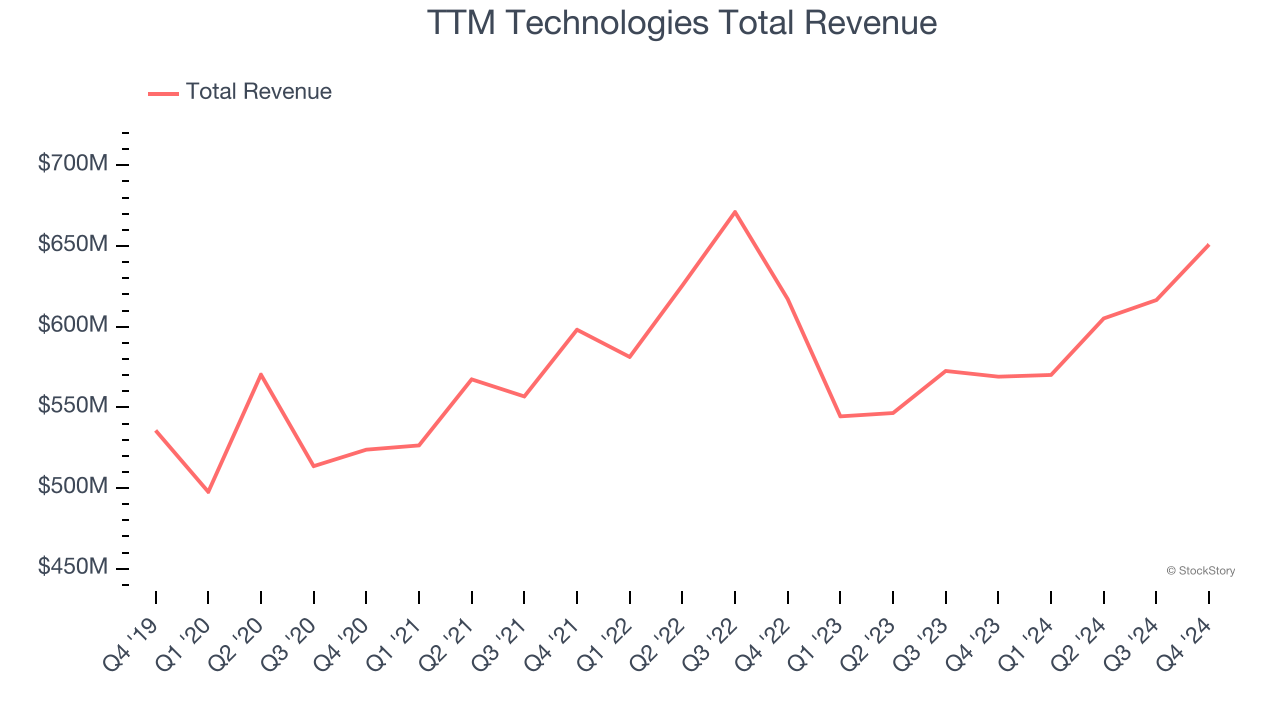

TTM Technologies (NASDAQ: TTMI)

As one of the world's largest printed circuit board manufacturers with facilities spanning North America and Asia, TTM Technologies (NASDAQ: TTMI) manufactures printed circuit boards (PCBs) and radio frequency (RF) components for aerospace, defense, automotive, and telecommunications industries.

TTM Technologies reported revenues of $651 million, up 14.4% year on year, outperforming analysts’ expectations by 2.9%. The business had a very strong quarter with a solid beat of analysts’ EPS estimates and revenue guidance for next quarter meeting analysts’ expectations.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 5.5% since reporting. It currently trades at $23.40.

Is now the time to buy TTM Technologies? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Knowles (NYSE: KN)

With roots dating back to 1946 and a focus on components that must perform flawlessly in critical situations, Knowles (NYSE: KN) designs and manufactures specialized electronic components like high-performance capacitors, microphones, and speakers for medical technology, defense, and industrial applications.

Knowles reported revenues of $142.5 million, down 33.8% year on year, falling short of analysts’ expectations by 2.4%. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations.

Knowles delivered the slowest revenue growth in the group. As expected, the stock is down 8.9% since the results and currently trades at $16.63.

Read our full analysis of Knowles’s results here.

Benchmark (NYSE: BHE)

Operating as a critical behind-the-scenes partner for complex technology products since 1979, Benchmark Electronics (NYSE: BHE) provides advanced manufacturing, engineering, and technology solutions for original equipment manufacturers across aerospace, medical, industrial, and technology sectors.

Benchmark reported revenues of $656.9 million, down 5% year on year. This number met analysts’ expectations. Overall, it was a strong quarter as it also put up a solid beat of analysts’ EPS estimates.

The stock is down 3.6% since reporting and currently trades at $42.06.

Read our full, actionable report on Benchmark here, it’s free.

CTS (NYSE: CTS)

With roots dating back to 1896 and a global manufacturing footprint, CTS (NYSE: CTS) designs and manufactures sensors, connectivity components, and actuators for aerospace, defense, industrial, medical, and transportation markets.

CTS reported revenues of $127.4 million, up 2.2% year on year. This print missed analysts’ expectations by 4%. It was a disappointing quarter as it also produced full-year revenue guidance missing analysts’ expectations.

CTS had the weakest performance against analyst estimates among its peers. The stock is down 11% since reporting and currently trades at $43.79.

Read our full, actionable report on CTS here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.