Wrapping up Q4 earnings, we look at the numbers and key takeaways for the building materials stocks, including Armstrong World (NYSE: AWI) and its peers.

Traditionally, building materials companies have built competitive advantages with economies of scale, brand recognition, and strong relationships with builders and contractors. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of building materials companies.

The 9 building materials stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 2% while next quarter’s revenue guidance was 1.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.3% since the latest earnings results.

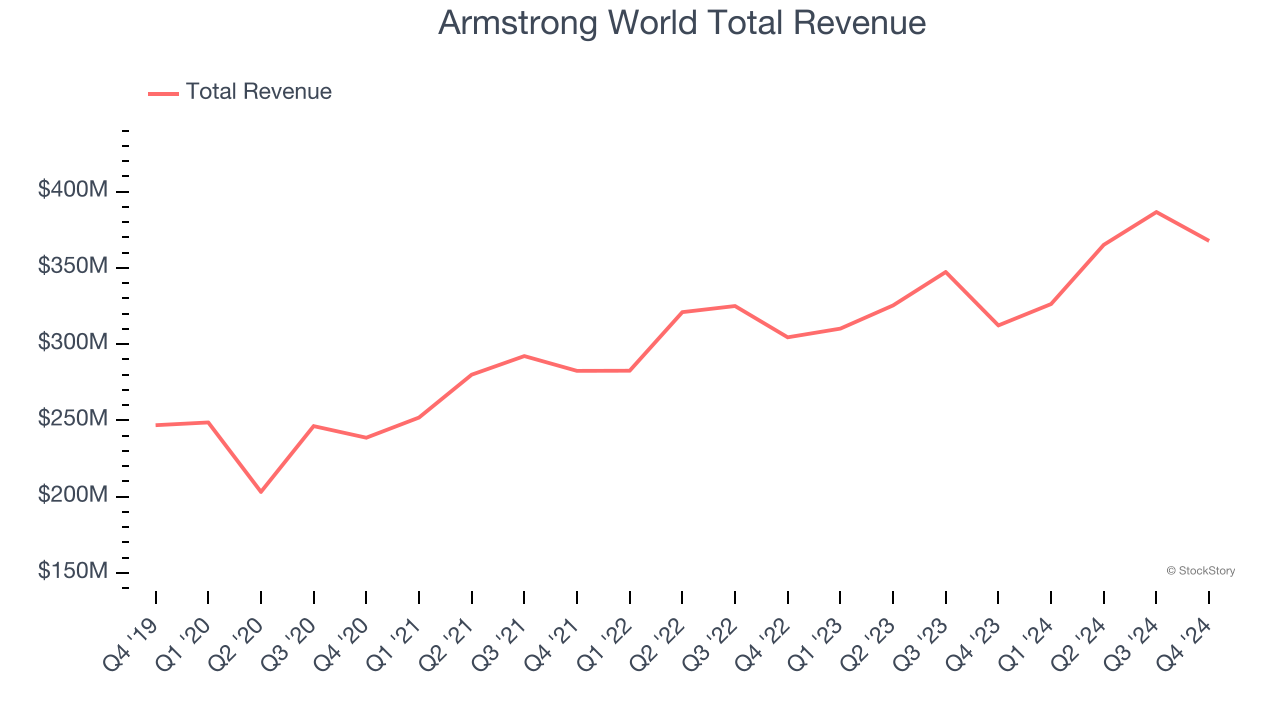

Armstrong World (NYSE: AWI)

Started as a two-man shop dating back to the 1860s, Armstrong (NYSE: AWI) provides ceiling and wall products to commercial and residential spaces.

Armstrong World reported revenues of $367.7 million, up 17.7% year on year. This print exceeded analysts’ expectations by 4.4%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ organic revenue estimates and full-year revenue guidance exceeding analysts’ expectations.

“These strong fourth-quarter results capped off another year of significant growth for Armstrong with record-setting sales and earnings, strong free cash flow generation, and two meaningful acquisitions to grow our Architectural Specialties capabilities,” said Vic Grizzle, President and CEO of Armstrong World Industries.

Armstrong World scored the highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 2.4% since reporting and currently trades at $142.39.

Is now the time to buy Armstrong World? Access our full analysis of the earnings results here, it’s free.

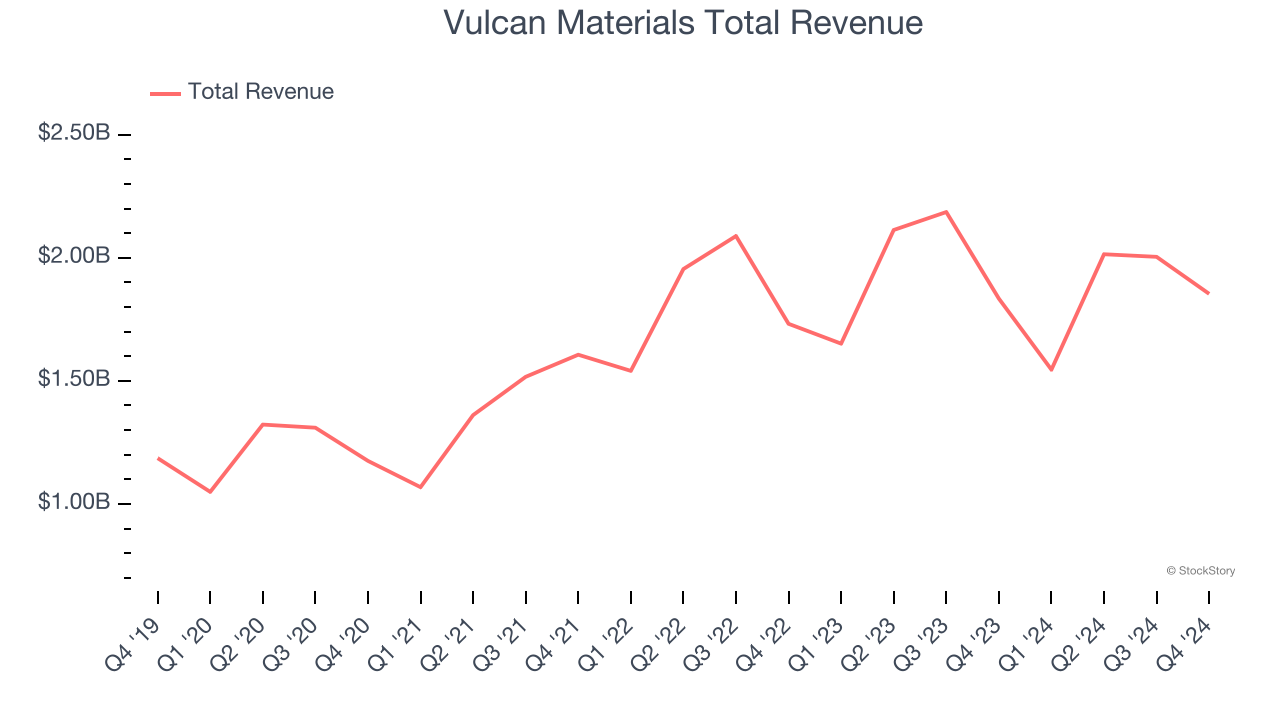

Best Q4: Vulcan Materials (NYSE: VMC)

Founded in 1909, Vulcan Materials (NYSE: VMC) is a producer of construction aggregates, primarily crushed stone, sand, and gravel.

Vulcan Materials reported revenues of $1.85 billion, up 1.1% year on year, outperforming analysts’ expectations by 2.1%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 11.8% since reporting. It currently trades at $238.50.

Is now the time to buy Vulcan Materials? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Carlisle (NYSE: CSL)

Originally founded as Carlisle Tire and Rubber Company, Carlisle Companies (NYSE: CSL) is a multi-industry product manufacturer focusing on construction materials and weatherproofing technologies.

Carlisle reported revenues of $1.12 billion, flat year on year, falling short of analysts’ expectations by 1.9%. It was a slower quarter as it posted a miss of analysts’ EBITDA and organic revenue estimates.

Carlisle delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 9.1% since the results and currently trades at $341.79.

Read our full analysis of Carlisle’s results here.

Tecnoglass (NYSE: TGLS)

The first-ever Colombian company to trade on the NASDAQ, Tecnoglass (NYSE: TGLS) is a manufacturer of architectural glass, windows, and aluminum products.

Tecnoglass reported revenues of $239.6 million, up 23.1% year on year. This print was in line with analysts’ expectations. Aside from that, it was a mixed quarter as it also recorded a narrow beat of analysts’ adjusted operating income estimates but full-year EBITDA guidance missing analysts’ expectations.

Tecnoglass achieved the fastest revenue growth among its peers. The stock is flat since reporting and currently trades at $69.36.

Read our full, actionable report on Tecnoglass here, it’s free.

Sherwin-Williams (NYSE: SHW)

Widely known for its success in the paint industry, Sherwin-Williams (NYSE: SHW) is a manufacturer of paints, coatings, and related products.

Sherwin-Williams reported revenues of $5.30 billion, flat year on year. This result met analysts’ expectations. Taking a step back, it was a slower quarter as it recorded full-year EPS guidance missing analysts’ expectations.

The stock is down 6.8% since reporting and currently trades at $336.06.

Read our full, actionable report on Sherwin-Williams here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.