Boot Barn has gotten torched over the last six months - since September 2024, its stock price has dropped 33.7% to $102.45 per share. This might have investors contemplating their next move.

Is there a buying opportunity in Boot Barn, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even though the stock has become cheaper, we don't have much confidence in Boot Barn. Here are three reasons why BOOT doesn't excite us and a stock we'd rather own.

Why Is Boot Barn Not Exciting?

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE: BOOT) is a western-inspired apparel and footwear retailer.

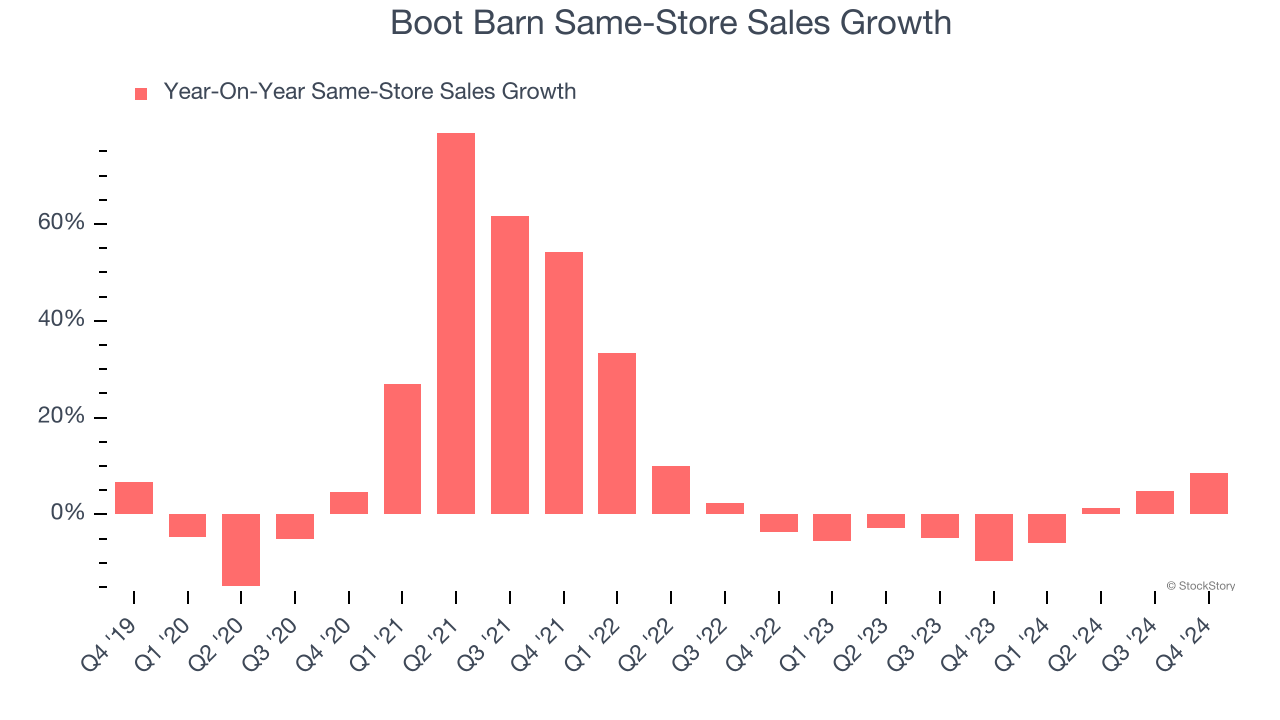

1. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Boot Barn’s demand has been shrinking over the last two years as its same-store sales have averaged 1.7% annual declines.

2. Fewer Distribution Channels Limit its Ceiling

With $1.85 billion in revenue over the past 12 months, Boot Barn is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers. On the bright side, it can grow faster because it has more white space to build new stores.

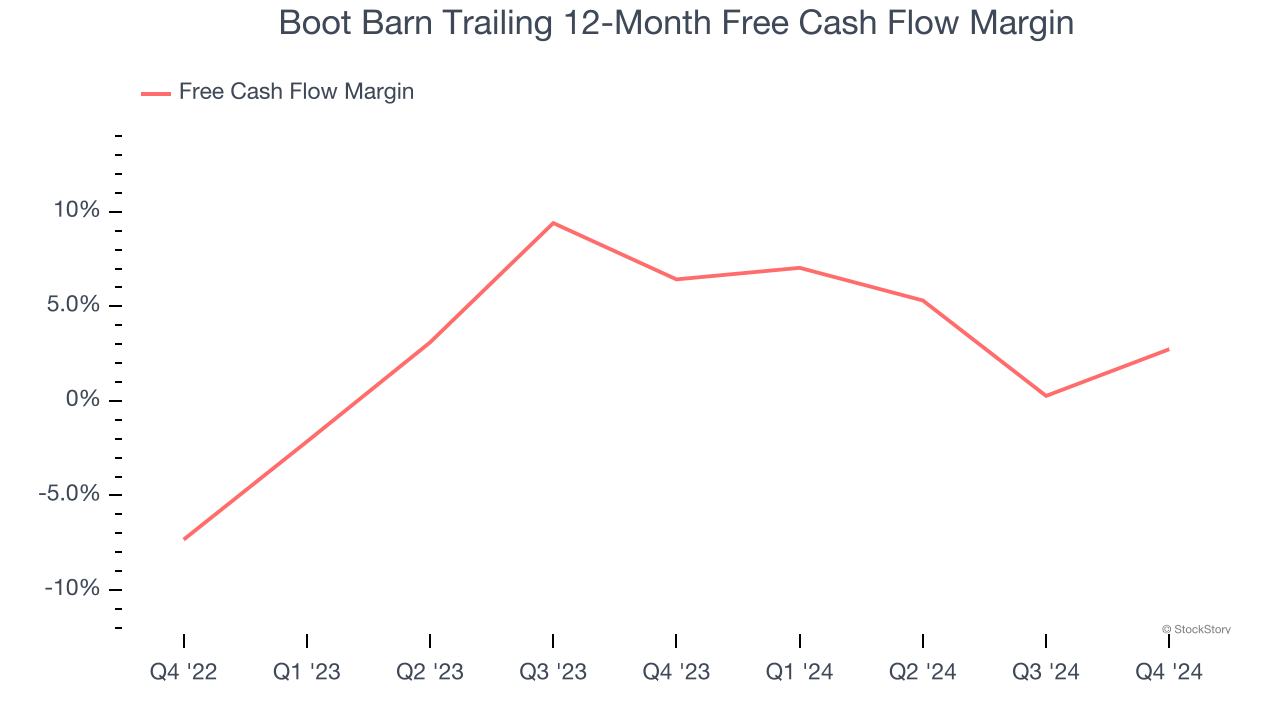

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Boot Barn’s margin dropped by 3.7 percentage points over the last year. This decrease came from the higher costs associated with opening more stores.

Final Judgment

Boot Barn isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 15.6× forward price-to-earnings (or $102.45 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Boot Barn

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.