The financial world turned its collective gaze toward the Bureau of Labor Statistics this morning, April 14, 2026, as the March Producer Price Index (PPI) data hit the wires. In a climate defined by geopolitical instability and a "no-landing" economic trajectory, this report was widely viewed as the ultimate litmus test for the Federal Reserve’s restrictive policy stance. While a massive energy shock stemming from the ongoing conflict in the Middle East threatened to derail the disinflationary trend, the final numbers offered a surprising—if complicated—sigh of relief for Wall Street.

The immediate market reaction was a sharp, albeit cautious, relief rally in the equity and bond markets. With headline PPI rising 0.5% month-over-month (MoM) against a feared 1.2% spike, the data suggests that while the "energy tax" is real, the dreaded "second wave" of broad-based wholesale inflation has yet to fully manifest in the services sector. For the Federal Reserve, this data validates their current "hawkish hold," but does little to accelerate the timeline for long-awaited rate cuts.

Energy Spikes and Core Calm: Inside the March Numbers

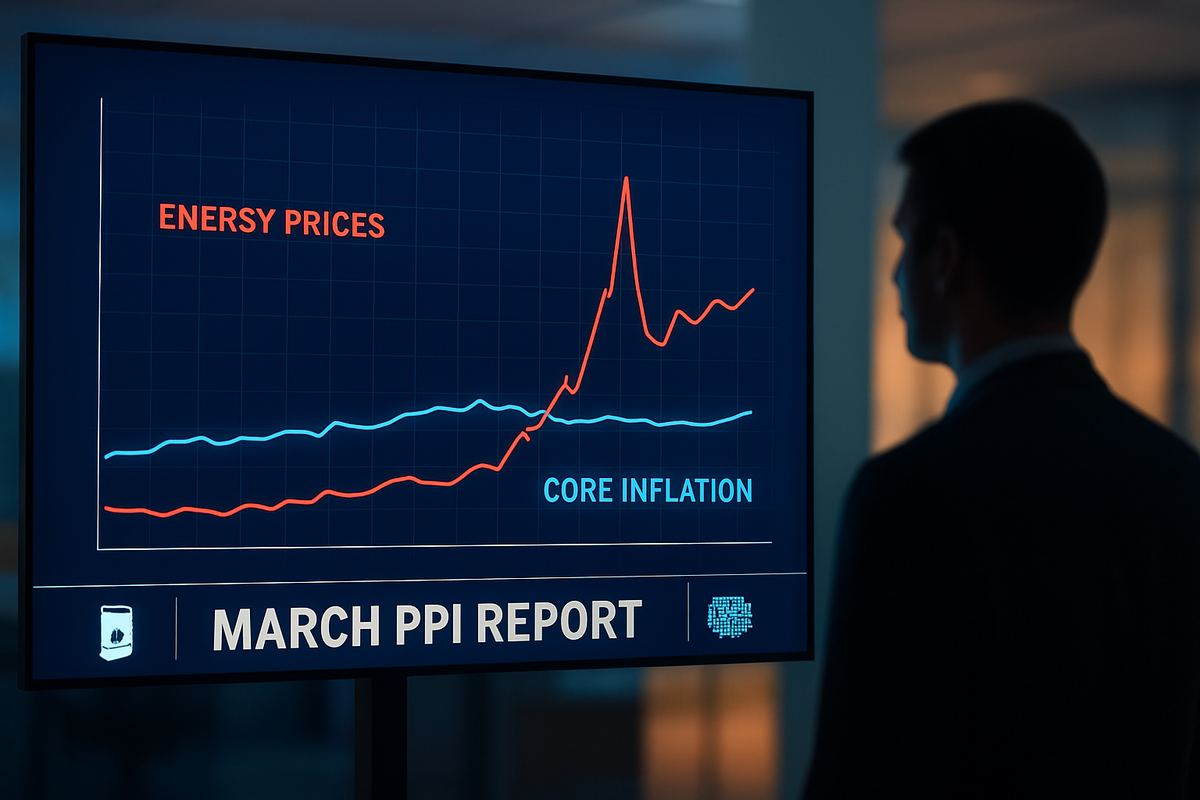

The March PPI report arrived against a backdrop of intense anxiety. Following the escalation of the War in Iran earlier this year, Brent crude oil prices breached the $100-per-barrel mark for the first time in years, leading analysts to brace for a catastrophic "hot" print. The consensus forecast had factored in a 1.2% MoM increase; however, the actual 0.5% figure indicates that the inflationary pressure remains largely isolated within the goods and energy sectors. Headline PPI now sits at 4.0% on a year-over-year (YoY) basis, a figure that would have been unthinkable a year ago but represents a cooling from the peaks of late 2025.

Drilling down into the report, the energy component was the undisputed driver of the headline figure. Final demand goods rose 1.6%, the largest gain in nearly three years, fueled by a staggering 15% jump in gasoline prices and an 8.5% overall increase in energy costs. Conversely, the Core PPI—which excludes the volatile food and energy categories—rose a mere 0.1% MoM, significantly undershooting the 0.5% estimate. This "core calm" suggests that manufacturers and service providers are currently absorbing higher energy costs rather than passing them immediately to consumers, a trend that the Fed will monitor with extreme scrutiny.

The timeline leading to this morning’s release has been one of extreme volatility. Since the March 17–18 FOMC meeting, where the Federal Reserve maintained interest rates at 3.50%–3.75%, the narrative has shifted from a "soft landing" to a "no-landing" scenario, driven by a resilient 4.3% GDP growth rate. Stakeholders, from retail investors to institutional hedge funds, had been pricing in a scenario where the Fed might even be forced to raise rates again if the PPI showed signs of a wage-price spiral. Today’s data effectively takes that "emergency hike" scenario off the table for now.

Winners and Losers in the Wholesale Arena

The surge in energy prices combined with the stagnation in service costs has created a fragmented landscape for public companies. ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have emerged as the clear beneficiaries of the PPI’s energy component. With wholesale gasoline and diesel prices up nearly 14% this month, these integrated oil giants are seeing massive margin expansion in their refining and marketing segments, even as higher input costs squeeze the broader economy.

On the other side of the ledger, the transportation and logistics sectors are feeling the heat. FedEx (NYSE: FDX) and United Parcel Service (NYSE: UPS) are grappling with the 13.9% jump in diesel fuel costs. While these companies typically employ fuel surcharges, the lag in implementation means that their Q1 and Q2 margins are likely to face temporary compression. Furthermore, the manufacturing sector remains under pressure; the manufacturing price index reached 78.3 this month, its highest level since 2022. Companies like Ford Motor Company (NYSE: F) are particularly vulnerable, as the PPI for "intermediate demand" of metals and electronics continues to climb, threatening to keep new vehicle prices elevated.

Technology "hyperscalers" such as Microsoft (NASDAQ: MSFT) and Amazon (NASDAQ: AMZN) are also navigating a complex PPI environment. While they are less sensitive to gasoline prices, the PPI report highlighted a persistent shortage in memory chips and rising costs for data center infrastructure. These "hidden" wholesale costs are essential components of the AI revolution, and any sustained increase in the producer price for electronic components could eventually dampen the record-breaking capital expenditure levels these companies have maintained through early 2026.

The 'No-Landing' Narrative and Geopolitical Ripple Effects

The March PPI data fits into a broader, more complex industrial trend: the decoupling of goods inflation from services inflation. Historically, a 15% spike in gasoline would lead to a rapid contagion of price hikes across the economy. However, in the post-2025 economy, the increased efficiency of supply chains and a shift toward domestic manufacturing have somewhat insulated the services sector from immediate energy shocks. This report mirrors the "supply-side shock" era of the late 1970s, but with a modern twist—a labor market that remains historically tight despite higher rates.

From a policy perspective, the Fed is trapped in a "geopolitical vice." The War in Iran is a supply-side disruption that interest rate hikes cannot solve. If the Fed raises rates to combat energy-driven PPI, they risk crushing the "no-landing" growth that has kept the U.S. economy afloat. Conversely, if they cut rates too soon, they risk fueling a core inflation rebound. This puts the Fed’s "soft landing" goal in a precarious position, as they must now account for a "permanently" higher energy floor in their 2% inflation calculations.

The broader significance of this release also touches on global trade. With wholesale food prices rising 2.4%—driven by a 50% spike in fresh vegetable costs—the global supply chain for perishables is showing signs of extreme stress. This regionalized inflation may force the U.S. government to reconsider certain trade tariffs to alleviate the "upstream" pressure on producers, marking a potential shift in industrial policy heading into the latter half of 2026.

What Lies Ahead: The Path to the May FOMC

In the short term, the relief rally following today's PPI release may be short-lived. Investors will now pivot toward the upcoming Consumer Price Index (CPI) data to see if the 1.6% rise in goods PPI has already begun to leak into retail shelves. If the core "pipeline" inflation remains at 0.1%, markets may begin to price back in the possibility of a single 25-basis-point rate cut in late 2026. However, if the "energy tax" starts to sap consumer spending power, the narrative could quickly shift from "no-landing" to "stagflation."

Strategic pivots are already underway in the corporate world. Many manufacturers are expected to increase their hedging activities on energy and raw materials to combat the volatility seen in March. We may also see a flurry of "efficiency-focused" AI investments as companies seek to offset rising wholesale input costs with automated labor and optimized logistics. The market opportunity here lies in companies that provide these deflationary technologies, potentially benefiting firms in the automation and software-as-a-service (SaaS) sectors.

Looking further out, the potential for a "commodity super-cycle" remains a dominant scenario. If geopolitical tensions in the Middle East do not subside, the PPI for energy could stay at these elevated levels for the remainder of the year, forcing a structural re-rating of the entire energy sector. Investors should prepare for a volatile summer, where "sticky" wholesale prices become the primary barrier to the Fed's pivot.

Conclusion: A Delicate Balance for Investors

The March PPI report is a reminder that the road to price stability is rarely a straight line. While the headline figures were distorted by a massive energy shock, the underlying core data suggests that the U.S. economy still possesses a remarkable degree of resilience. The "soft landing" remains the base case for many, but the emergence of the "no-landing" scenario—and its accompanying high-for-longer interest rate environment—means that the margin for error has never been thinner.

Moving forward, the market will likely reward companies with strong pricing power and low energy intensity. Investors should move away from speculative growth and toward firms with "inflation-proof" balance sheets. The primary takeaways from this morning are clear: the Fed is not in a rush to cut, the energy market is the new wildcard, and the "pipeline" of inflation is behaving better than the "pump" price would suggest.

In the coming months, watch for the "lag effect" of these energy prices on the services sector and the Fed’s June "Dot Plot" for signs of a policy shift. For now, the MarketMinute remains one of cautious optimism, as the economy successfully navigated one of the most feared data releases of 2026 without triggering a total market meltdown.

This content is intended for informational purposes only and is not financial advice