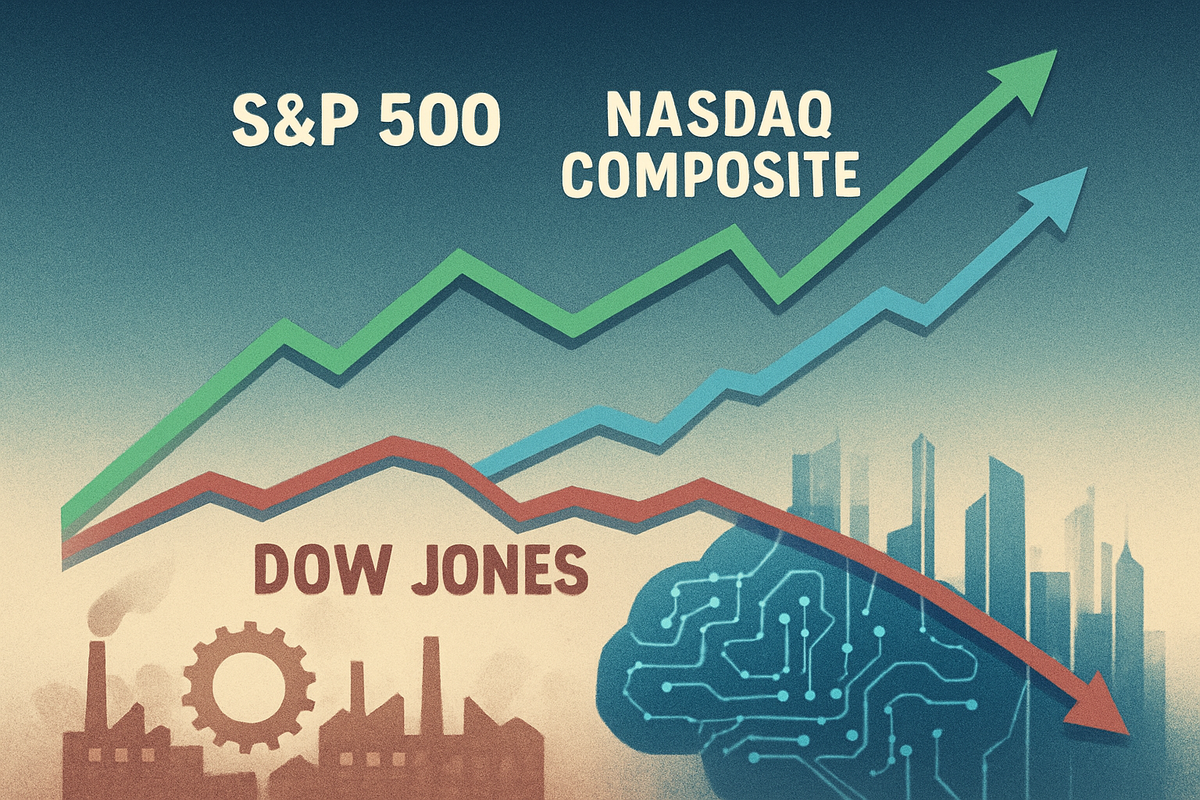

In a perplexing twist for market watchers in late 2025, the venerable Dow Jones Industrial Average (DJIA) (NYSE: ^DJI) has exhibited a noticeably more subdued performance, occasionally slipping or lagging, even as its counterparts, the S&P 500 (NYSE: ^GSPC) and the Nasdaq Composite (NASDAQ: ^IXIC), continue their robust ascent. This divergence paints a complex picture for investors, signaling a market driven by concentrated gains in specific sectors and prompting a re-evaluation of the health and breadth of the ongoing bull run. While the S&P 500 boasts a commendable over 12% year-to-date gain and the tech-heavy Nasdaq has surged past 15%, the Dow has managed a more modest 8%, highlighting a significant schism in market leadership.

This uneven performance immediately casts a shadow of caution over market sentiment. The driving force behind the S&P 500 and Nasdaq's superior returns is largely attributed to the sustained "mania" around artificial intelligence (AI) technology and the outsized influence of mega-cap tech stocks, notably Nvidia (NASDAQ: NVDA). However, this concentration also breeds nervousness, with a significant portion of global fund managers identifying an "AI bubble" as a top market risk. Coupled with lingering uncertainties surrounding the Federal Reserve's interest rate policy and elevated volatility, this divergence suggests that while the bull run persists, it is becoming increasingly selective and demands a more discerning approach from investors.

The Bifurcated Market: Tech Dominance and Dow's Traditional Weight

The observable divergence in late 2025 stems fundamentally from the distinct weighting methodologies and sector compositions of the major indexes. The Dow Jones Industrial Average (NYSE: ^DJI), a price-weighted index of 30 established U.S. "blue-chip" companies, is heavily influenced by traditional sectors like industrials, financials, and consumer staples. Its price-weighted nature means that stocks with higher share prices disproportionately impact the index. In stark contrast, the S&P 500 (NYSE: ^GSPC) and particularly the Nasdaq Composite (NASDAQ: ^IXIC) are market-capitalization-weighted and heavily skewed towards technology and high-growth companies. This structural difference sets the stage for a market where a surge in a specific sector can propel some indexes while leaving others behind.

Throughout early to mid-2025, the market witnessed a persistent and escalating "AI-led technology cycle" that continued to funnel significant investment into the tech sector. Companies at the forefront of artificial intelligence, semiconductors, and cloud computing announced robust earnings and groundbreaking innovations, fueling an optimistic narrative around future growth. Concurrently, a backdrop of moderate economic growth and steady, or even slightly declining, interest rates further buoyed growth stocks. Lower borrowing costs tend to benefit companies with high future earnings potential, as their valuations become more attractive when discounted at lower rates, a dynamic less impactful for the more mature, value-oriented companies often found in the Dow.

However, as late Q3 and Q4 2025 unfolded, traditional sectors began to encounter headwinds. The industrial sector, for instance, faced challenges from escalating geopolitical tensions, which disrupted global supply chains and increased raw material costs, alongside signs of softening global demand for durable goods. Labor costs continued to rise, squeezing profit margins for labor-intensive manufacturing and logistics firms. The financial sector, while potentially benefiting from sustained net interest margins, also grappled with concerns over potential loan defaults in a slower economic environment and increased regulatory scrutiny. These pressures, often impacting several key Dow components, created a drag on the index.

The Q3 2025 earnings season crystallized this disparity. While major technology companies, many of which are heavily weighted in the S&P 500 and Nasdaq, reported stellar earnings, exceeding analyst expectations driven by insatiable demand for AI infrastructure and digital services, several prominent Dow components delivered disappointing results. These companies, primarily in the industrial, manufacturing, and traditional retail sectors, often cited increased operational costs, supply chain bottlenecks, or weakening consumer spending as reasons for missing forecasts or providing subdued guidance. This led to a visible rotation of investor capital, with a clear preference for companies perceived as having more resilient, innovation-driven business models. Initial market reactions included heightened volatility for Dow components, while the tech rally continued, albeit with growing scrutiny over its concentration and sustainability, fueling widespread discussions about a significant sector rotation.

Winners and Losers in a Divided Market

This pronounced market divergence in late 2025 creates a clear delineation between the companies and sectors poised to thrive and those likely to face significant headwinds. The winners are predominantly innovative, technology-driven, and growth-oriented firms, which constitute a substantial portion of the S&P 500 (NYSE: ^GSPC) and Nasdaq Composite (NASDAQ: ^IXIC). Conversely, the companies feeling the pinch are often the traditional, established "blue-chip" industrial companies, financials, and mature consumer staples that hold significant weight within the Dow Jones Industrial Average (NYSE: ^DJI).

Leading the charge among the beneficiaries are the giants of the Information Technology sector, including titans like Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN), Nvidia (NASDAQ: NVDA), Alphabet (NASDAQ: GOOGL), and Meta Platforms (NASDAQ: META). These companies, deeply embedded in artificial intelligence, cloud computing, advanced software, and digital services, are experiencing sustained demand and robust earnings growth. Their stock performance is expected to continue its upward trajectory, with investors justifying higher price-to-earnings multiples based on strong innovation and market leadership. Their business strategies are focused on aggressive research and development, strategic acquisitions of cutting-edge startups, and expanding into new digital markets, further consolidating their market share and maintaining a competitive edge through relentless innovation. Semiconductor companies like Nvidia (NASDAQ: NVDA), Broadcom (NASDAQ: AVGO), and AMD (NASDAQ: AMD), foundational to the AI revolution, are also seeing soaring demand and strong revenue growth, reinforcing their position as market darlings.

On the other side of the spectrum, traditional Heavy Industrials such as Caterpillar (NYSE: CAT), Boeing (NYSE: BA), and 3M (NYSE: MMM), mainstays of the Dow, are feeling the brunt of global supply chain disruptions, rising input costs, and softening international demand. Their stock performance is likely to stagnate or decline, potentially leading to lower valuations and pressure on dividend yields. These firms are compelled to focus on stringent cost-cutting, operational efficiencies, and supply chain optimization, rather than aggressive growth initiatives. Similarly, Traditional Financial Institutions like JPMorgan Chase (NYSE: JPM) and Goldman Sachs (NYSE: GS), while diversified, face challenges from macroeconomic factors and the market's preference for growth over value, potentially leading to lagging stock prices. Even robust Consumer Staples companies such as Walmart (NYSE: WMT) and Procter & Gamble (NYSE: PG), while stable, offer lower growth profiles that are less appealing in a market seeking disruptive returns, pushing them to double down on digital transformation and efficiency to fend off agile online competitors.

This market divergence underscores a significant structural shift, where investor capital is increasingly flowing towards companies that demonstrate high-margin growth through technological advancement and innovation, often at the expense of established firms more susceptible to traditional economic cycles and slower adaptation.

Broader Implications and Historical Parallels

The late 2025 divergence, where the Dow Jones Industrial Average (NYSE: ^DJI) falters while other major indices surge, represents more than a mere statistical anomaly; it signals a profound shift in market dynamics with far-reaching implications for industries, policy, and the long-term economic outlook. This trend points to a significant sector rotation, where capital is migrating from traditional "old economy" blue-chip companies, heavily represented in the Dow, towards innovation-driven growth sectors, particularly technology, which dominate the Nasdaq Composite (NASDAQ: ^IXIC) and hold substantial weight in the S&P 500 (NYSE: ^GSPC). This shift is fueled by continued excitement around artificial intelligence (AI), even amidst some "AI bubble" concerns, and an economic reassessment that questions the resilience of traditional industrial production against the backdrop of more robust, digitally-driven segments of the economy. The narrowing market breadth, with fewer stocks driving overall market gains, also raises concerns about underlying market health.

The ripple effects across industries are substantial. Companies heavily weighted in the Dow, such as those in manufacturing, aerospace, and certain financial services, face increased pressure on stock performance, higher costs of capital, and diminished capacity for expansion. Competitors within these traditional sectors are grappling with similar headwinds, while their counterparts in the ascendant technology sector benefit from heightened investor confidence and capital inflows, enabling greater investment in R&D and market expansion. Furthermore, partners and participants within traditional industrial and manufacturing supply chains, particularly those with weaker balance sheets, are finding it increasingly difficult to compete, potentially leading to disruptions, higher component prices, and an acceleration of trends like "reshoring" to build more resilient, albeit potentially costlier, domestic supply chains.

From a regulatory and policy standpoint, a sustained divergence could trigger several considerations. Regulators might express concerns about market concentration risk if the rally is driven by a narrow set of mega-cap tech stocks, potentially leading to calls for interventions to safeguard market stability. Governments, particularly if focused on domestic economic activity, might implement industrial policies aimed at supporting traditional industries through deregulation and tax incentives to mitigate their decline. Conversely, the booming tech sector may face increased technology regulation, with governments worldwide grappling with the ethical deployment of AI, data privacy, and potential antitrust concerns, which could impact the profitability and growth trajectories of leading tech firms. Central banks might also reassess monetary and fiscal policies if the Dow's decline signals broader economic stress not fully captured by the tech-driven indices.

Historically, this scenario draws parallels to the Dot-com Bubble of the late 1990s and early 2000s, a period characterized by an unprecedented boom in technology stocks and lagging "old economy" companies. While today's leading tech firms often possess stronger fundamentals, the "AI bubble" fears and the concentrated rally in a few "Magnificent Seven" stocks echo the speculative enthusiasm of that era. Moreover, such divergences align with historical sector rotations observed during different economic cycles and serve as a potential bearish market breadth divergence, where a lack of broad participation in a market rally can signal underlying weakness and increased risk for a future pullback.

What Comes Next: Navigating a Shifting Landscape

The market's current divergence points to a future defined by continued volatility and significant strategic adjustments for both companies and investors. In the short term (late 2025 - early 2026), expect ongoing sector rotations as "smart money" rebalances portfolios, potentially leading to a continued shift of capital from high-flying technology and AI stocks towards more traditional, fundamentally strong industries often represented in the Dow Jones Industrial Average (NYSE: ^DJI). This "Great Rotation" means investors should brace for potential pullbacks in growth-oriented equities and a reallocation to value stocks, international equities, financials, and industrials. Macroeconomic data, including persistent inflation reports and central bank policy statements, will heavily influence market sentiment, maintaining a "risk-off" environment. Despite these pressures, record amounts of cash in money market funds suggest that any significant dips are likely to be met with buying activity, indicating underlying confidence in the long-term trajectory.

Looking long term (2026 and beyond), the market may be transitioning out of a "Goldilocks" era of low inflation and strong growth, potentially ushering in stagflationary pressures. Companies that genuinely integrate AI into their core operations to drive efficiency and create new revenue streams are poised to emerge stronger, as the AI investment cycle is still in its nascent stages, promising sustained momentum for corporate earnings and a potential productivity boom. Market leadership is expected to broaden beyond a few mega-cap tech stocks, with value stocks and previously underperforming sectors taking on a larger role. While the pace of U.S. stock market gains may moderate, overall returns are anticipated to remain positive, with earnings growth, rather than further valuation expansion, doing the "heavy lifting."

To navigate this evolving landscape, companies must prioritize robust financial planning, maintaining healthy cash reserves, and managing debt wisely. Diversification of revenue streams, agile supply chain management, and strategic AI integration that focuses on genuine efficiency and new revenue streams are critical. Investors must embrace broad diversification across asset classes, geographies (including international markets which are showing outperformance), and even alternative investments. Rigorous bottom-up analysis, focusing on mid- and small-cap companies with reasonable valuations, will be crucial. Maintaining higher cash reserves for "dry powder" during volatility and adopting a long-term perspective will be paramount, alongside considering allocations to value and defensive sectors like utilities and healthcare.

Several scenarios could unfold. The most likely outcome is a continued divergence and sector rotation, leading to a complex, non-uniform market performance. A "hard landing" could occur if sticky inflation forces central banks to maintain restrictive policies, triggering a recession and a broader market downturn. Conversely, an "AI bubble" burst could significantly impact AI-centric companies if investments fail to yield corresponding revenue growth. On a more optimistic note, a "market melt-up" or "soft landing" could see equities continue to scale new heights, supported by benign economic conditions and rapid technological advancements. Finally, a stagflationary environment, characterized by moderate growth and persistent inflation, would necessitate a focus on resilience and income generation.

Comprehensive Wrap-Up and Forward Outlook

Late 2025 has seen the Dow Jones Industrial Average (NYSE: ^DJI) enter a corrective phase after a prolonged rally, reflecting a broad risk-averse sentiment impacting its specific constituents. Simultaneously, the S&P 500 (NYSE: ^GSPC) and Nasdaq Composite (NASDAQ: ^IXIC) have shown resilience, propelled by strong performance in select sectors and large-cap growth stocks. This disparity underscores a growing fragmentation within the market, where "the market" can no longer be defined by a single index's performance.

Key Takeaways: The divergence highlights that index construction matters, with the Dow's price-weighted nature making it highly sensitive to individual stock performance. Sectoral disparities, driven by a rotation away from some traditional industrial and discretionary sectors towards technology and growth, are evident. Idiosyncratic risks affecting highly-priced Dow components, coupled with macroeconomic headwinds like Federal Reserve policy uncertainty and a stronger U.S. dollar, are weighing more heavily on the Dow's constituents.

Assessing the Market Moving Forward: The market moving into early 2026 will likely be characterized by continued crosscurrents. This divergence could either be a temporary recalibration or a harbinger of a more sustained shift. Should the underlying economic picture continue its trajectory of slowing growth without a sudden deterioration, and inflation remains stubborn, we could see further rotation. Defensive sectors and those with robust, consistent earnings, often found within the Dow, might find renewed investor interest as a flight to quality. Conversely, a resurgence in risk appetite or clear signals of accelerated economic growth could reignite the momentum in growth and technology stocks, potentially widening the performance gap.

Final Thoughts on Significance and Lasting Impact: The late 2025 Dow divergence serves as a potent reminder that not all market benchmarks tell the same story. While the Dow has historically served as a bellwether for the industrial health of the nation, its limited scope and weighting methodology can sometimes misrepresent the broader market's vitality. This period of divergence underscores the critical importance of understanding index construction and the underlying economic forces at play. Its lasting impact may be a heightened awareness among investors about the nuances of market indices and the dangers of a "one-size-fits-all" approach to market analysis. It highlights that market strength can be concentrated, and a narrow view can lead to misinterpretations of overall market health.

Investor Advisory: What to Watch in Coming Months: Investors navigating this complex landscape should prioritize diversification and vigilance. Key areas to monitor include:

- Earnings Season: Pay close attention to corporate earnings reports, particularly forward guidance from Dow components. Look for signs of resilience in industrials and financials, and any shifts in consumer spending impacting retail and discretionary stocks.

- Federal Reserve Communications: The Fed's stance on interest rates, inflation, and economic growth will be paramount. Any clarity on a rate-cut path or changes in monetary policy could significantly impact market sentiment and sector performance.

- Sector Performance & Rotation: Monitor which sectors are leading and lagging. Periods of high sector dispersion indicate increased market volatility and opportunities for tactical shifts. Consider a sector rotation strategy that aligns with expected economic cycles, favoring defensive sectors during uncertainty and cyclical ones during expansion.

- Economic Indicators: Keep a close eye on inflation data, GDP growth, unemployment figures, and consumer confidence. Divergences between market performance and economic indicators can signal potential turning points.

- Global Developments: Geopolitical events and international trade policies can have ripple effects across global markets and specific industries.

- Index Composition and Valuation: Understand the biases of each index. If considering Dow-specific investments, be aware of the performance of its largest components and their individual valuations. Conversely, continue to evaluate the often-high valuations in the tech sector, which could be susceptible to corrections.

By remaining informed and adapting investment strategies to these evolving market conditions, investors can better navigate the complexities of late 2025 and position themselves for potential opportunities in the new year.

This content is intended for informational purposes only and is not financial advice