New York-based Take-Two Interactive Software, Inc. (TTWO) is a global video-game holding company that develops, publishes, and markets interactive entertainment across console, PC, and mobile platforms. Valued at $43.8 billion by market cap, the firm operates primarily through its major publishing labels Rockstar Games, 2K, and Zynga, each managing internal studios and flagship franchises.

The video games giant’s shares have tanked marginally over the past 52 weeks, compared to the S&P 500 Index’s ($SPX) 25.1% gains. On a YTD basis, the TTWO is down 7.6%, trailing $SPX’s 8.6% rise.

Narrowing the focus, Take-Two has surpassed the industry-focused VanEck Video Gaming and eSports ETF’s (ESPO) 9.8% fall over the past year and 12.5% dip in 2026.

Take-Two Interactive has underperformed the S&P 500 Index over the past year primarily due to investor concerns surrounding near-term profitability and uncertainty tied to its future game release pipeline. Much of the company’s long-term valuation is heavily dependent on the highly anticipated launch of Grand Theft Auto VI, and any uncertainty around the game’s timing, development progress, or monetization potential has weighed on market sentiment.

For the fiscal 2026 that ended in March, analysts expect TTWO to deliver an adjusted EPS of $2.44, up 335.7% year-over-year. Further, the company has a solid earnings surprise history. It has surpassed the Street’s bottom-line projections in each of the past four quarters.

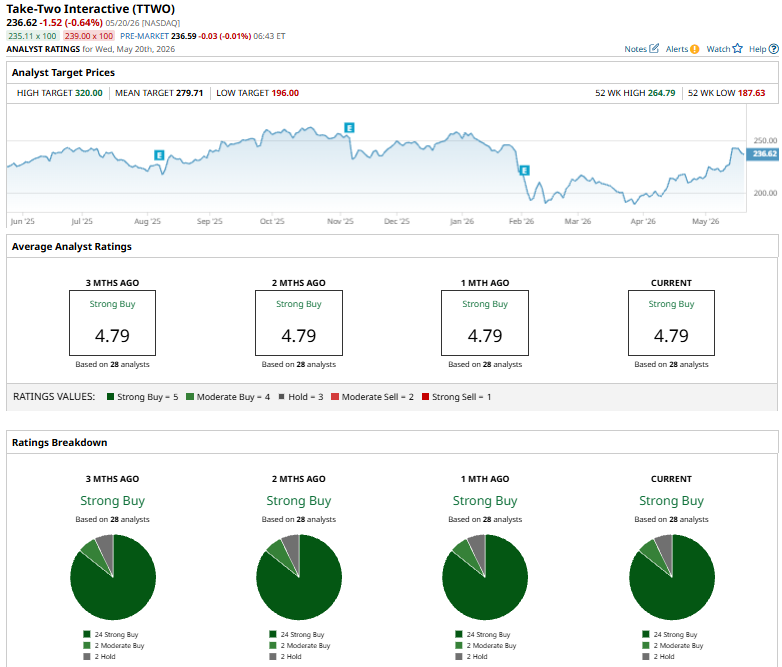

Among the 28 analysts covering the TTWO stock, the consensus rating is a “Strong Buy.” That’s based on 24 “Strong Buys,” two “Moderate Buys,” and two “Holds.”

On Apr. 6, Wells Fargo slightly lowered its price target on Take-Two Interactive Software to $293 from $295 while maintaining an “Overweight” rating on the stock. The firm said concerns surrounding third-party mobile gaming data appear overdone, though it expects a challenging near-term setup as the company’s initial fiscal 2027 earnings guidance is likely to be conservative.

TTWO’s mean price target of $279.71 represents a 18.2% premium to current price levels. Meanwhile, the Street-high target of $320 suggests a notable 35.2% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Sandisk Stock Is Up 535% in 2026. That Didn’t Stop Billionaire David Tepper from Buying 281,250 Shares.

- Nvidia Delivered a Stellar Quarter. Its Unusual Options Activity Points to 2 Asymmetric Bets on NVDA Stock.

- An Apparent Short Squeeze Is Brewing in T1 Energy Stock

- Intuit Is Slashing More Than 3,000 Jobs. Why Wall Street Is Punishing INTU Stock for the AI Pivot.