Golden, Colorado-based Molson Coors Beverage Company (TAP) manufactures, markets, distributes, and sells beer and other malt beverage products. Valued at a market cap of $7.8 billion, the company offers flavored malt beverages, including hard seltzers, craft spirits, and ready-to-drink beverages. It also provides non-alcoholic beverages, including premium mixers and energy drinks.

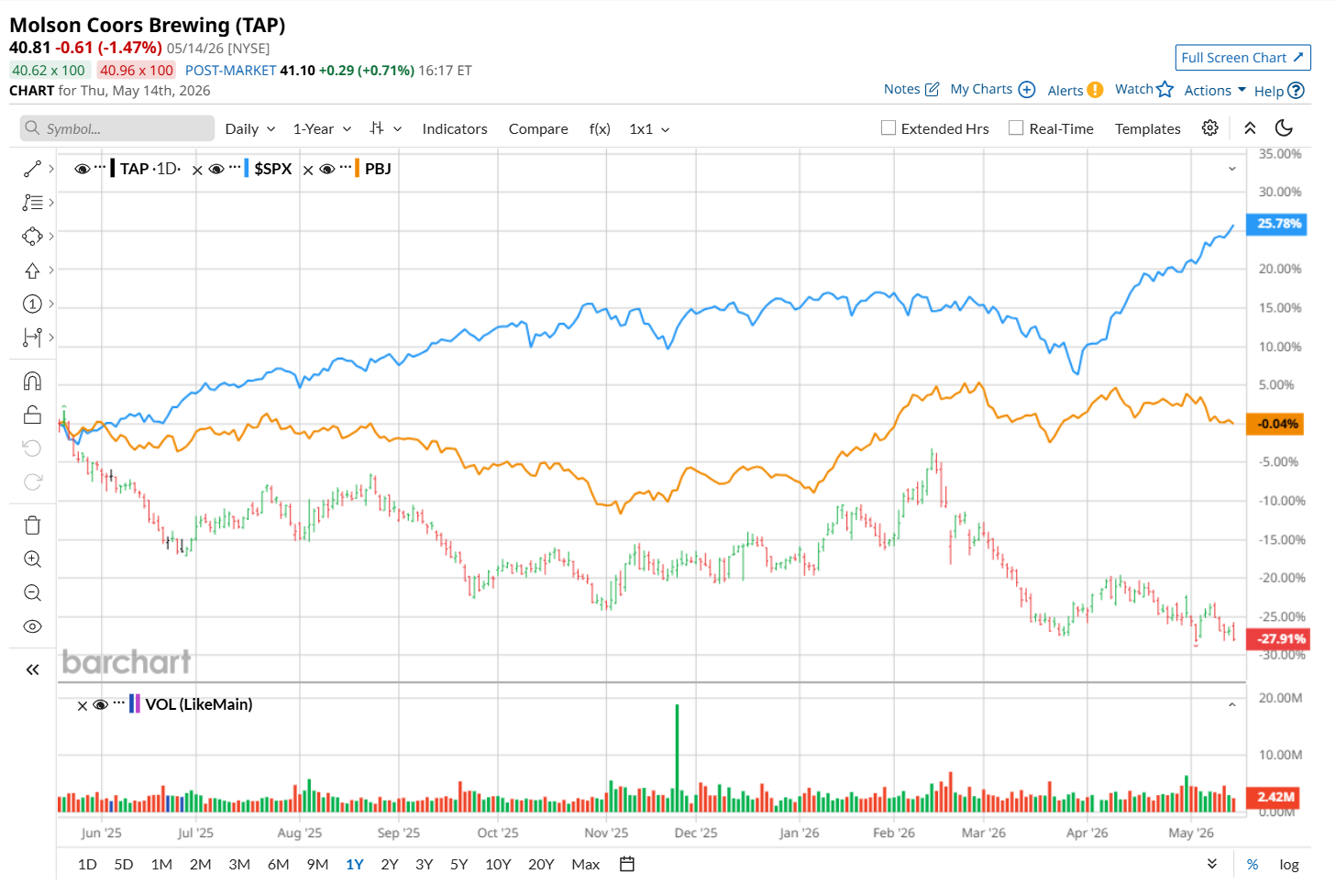

This beverage company has considerably lagged the broader market over the past 52 weeks. Shares of TAP have declined 26.5% over this time frame, while the broader S&P 500 Index ($SPX) has gained 26.5%. Moreover, on a YTD basis, the stock is down 12.6%, compared to SPX’s 8.1% rise.

Narrowing the focus, TAP has also underperformed the Invesco Food & Beverage ETF’s (PBJ) 2.8% rise over the past 52 weeks and 7.9% uptick on a YTD basis.

TAP shares closed up marginally on Apr. 30 after its better-than-expected Q1 earnings results. The company’s revenue increased 2% year-over-year to $2.35 billion, topping analyst estimates by a slight margin. Moreover, its adjusted EPS of $0.62 handily exceeded consensus expectations of $0.36. The quarter saw volume declines offset by gains in on-premise channels and early success with new products like Fever Tree and the reintroduction of Keystone Ice.

For the current fiscal year, ending in December, analysts expect TAP’s EPS to decline 12.6% year over year to $4.74. The company’s earnings surprise history is mixed. It topped the consensus estimates in three of the last four quarters, while missing on another occasion.

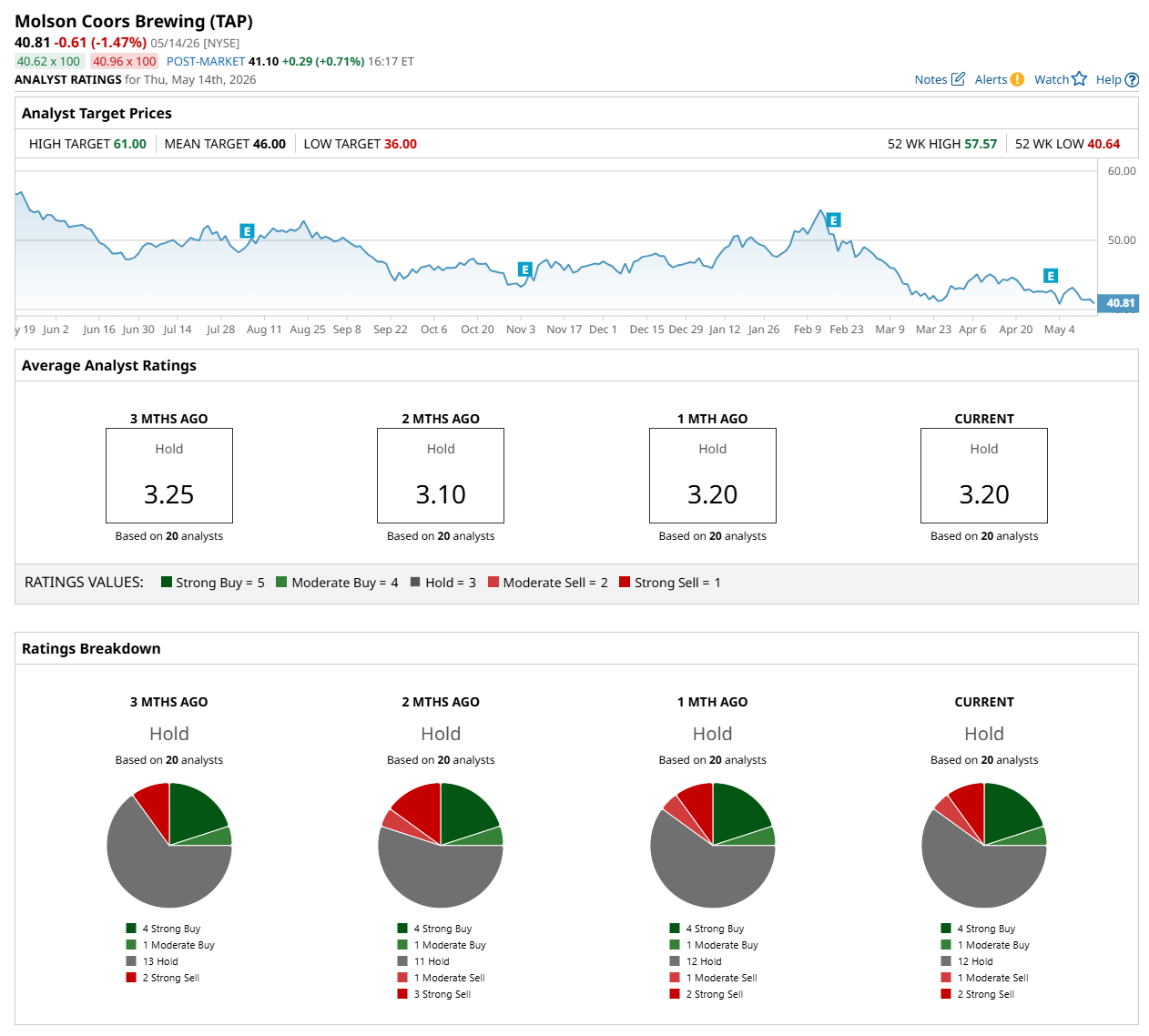

Among the 20 analysts covering the stock, the consensus rating is a "Hold," which is based on four “Strong Buy,” one “Moderate Buy,” 12 "Hold,” one "Moderate Sell,” and two “Strong Sell” ratings.

The configuration is less bearish than two months ago, with three analysts suggesting a “Strong Sell” rating.

On May 13, Evercore ISI analyst Robert Ottenstein maintained a “Buy” rating on TAP and set a price target of $47, indicating a 15.2% potential upside from the current levels.

The mean price target of $46 suggests a 12.7% premium to its current price levels, while its Street-high price target of $61 implies a 49.5% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- More Than 1,000 Corporate Positions Hit at Walmart in Latest Restructuring. What This Means for WMT Stock.

- Cisco (CSCO) Stock Just Hit a Record High Amid Layoffs Announcement

- Ukraine Will Leverage Palantir’s AI Capabilities In Its War With Russia. This Helps Prove PLTR Stock Will Never Be Irrelevant.

- 2 Reasons Quantum Cyber Has More Than Doubled Today