San Jose, California-based PayPal Holdings, Inc. (PYPL) operates a technology platform that enables digital payments on behalf of merchants and consumers. Valued at $44.8 billion by market cap, the company offers online payment solutions worldwide.

Shares of this fintech giant have notably underperformed the broader market over the past year. PYPL has declined 23.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 29.1%. In 2026, PYPL stock is down 15%, compared to the SPX’s 4.3% rise on a YTD basis.

Narrowing the focus, PYPL has also lagged behind the Global X FinTech ETF (FINX). The exchange-traded fund has declined about 9.3% over the past year. Moreover, the ETF’s 13.5% losses on a YTD basis outshine the stock’s dip over the same time frame.

PayPal’s underperformance stems from slowing branded checkout growth amid macro and competitive headwinds. Its merchant base is exposed to discretionary spending, so softness among lower-income and middle-income U.S. consumers hurt transaction growth, and PayPal failed to gain share during peak retail periods. International pressure grew as Germany, a key market, cooled due to macro weakness and rival payment methods. Moreover, management admits execution missteps magnified these pressures, while rising competition and stepped-up investments are squeezing margins during this transition period.

For fiscal 2026, ending in December, analysts expect PYPL’s EPS to grow marginally to $5.32 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

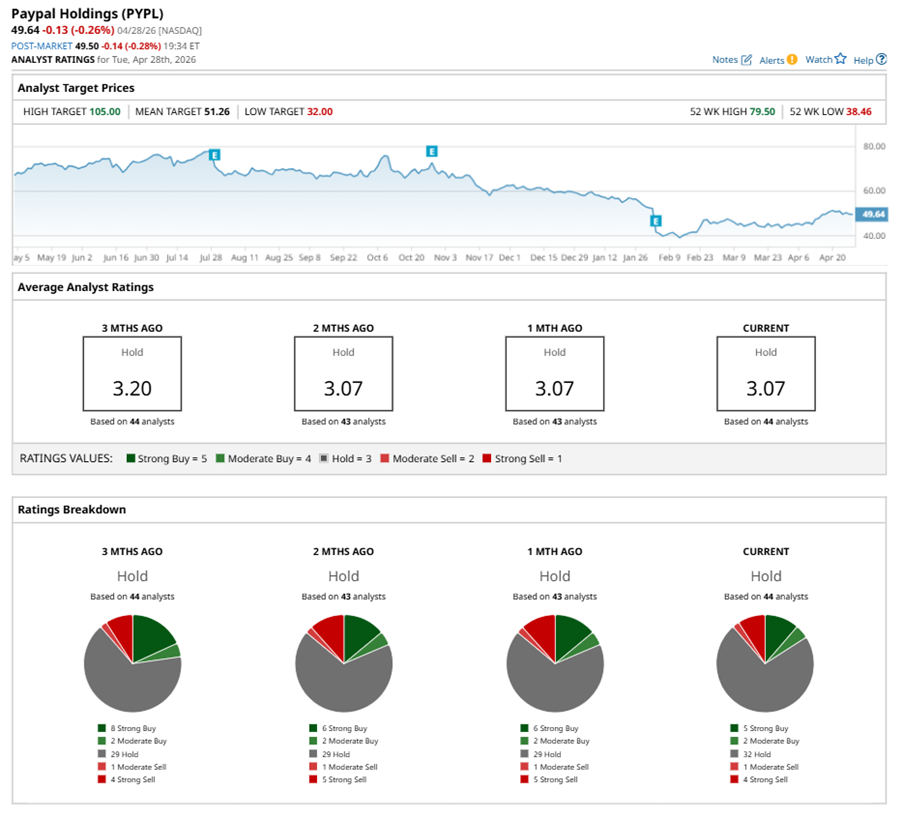

Among the 44 analysts covering PYPL stock, the consensus is a “Hold.” That’s based on five “Strong Buy” ratings, two “Moderate Buys,” 32 “Holds,” one “Moderate Sell,” and four “Strong Sells.”

This configuration is more bearish than a month ago, with six analysts suggesting a “Strong Buy,” and five recommending a “Strong Sell.”

On Apr. 27, BMO Capital analyst Andrew Bauch received a “Hold” rating on PYPL with a $52 price target, implying a potential upside of 4.8% from current levels.

The mean price target of $51.26 represents a 3.3% premium to PYPL’s current price levels. The Street-high price target of $105 suggests an ambitious upside potential of 111.5%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Super Micro Computer Expands Its Data Center Offerings, Should You Buy, Sell, or Hold SMCI Stock?

- Dan Ives’ Latest AI ETF Goes Beyond the Mag 7, Focusing on the ‘Circulatory System’ of a Tech Revolution

- Bloom Energy Just Hit an All-Time High. Should You Chase the Rally Here?

- Your Smartphone Could Soon Be an AI Agent, and Qualcomm Stock Is Positioned to Profit Big