Tesla (TSLA) will release its first-quarter earnings on April 22. Although TSLA stock has recovered modestly in recent sessions, it remains down about 11% year-to-date (YTD), reflecting persistent investor concerns about weakness in its core electric vehicle (EV) business and the absence of a clear near-term catalyst.

A key overhang is the company’s lower-than-expected vehicle deliveries in Q1, which shows slowing demand and increased competition. At the same time, Tesla has not provided any significant update on its physical AI initiatives, which are critical to sustaining its long-term growth premium. Without fresh developments on these fronts, the investment case in the short term appears constrained, especially relative to elevated expectations already embedded in Tesla’s valuation.

That said, the upcoming earnings call could still give TSLA stock a lift. Management's positive commentary around AI initiatives, most notably Full Self-Driving (FSD), the robotaxi platform, and humanoid robotics, will likely be in focus. Any credible roadmap, clear timeline, or evidence of monetization potential in these areas could shift sentiment and support its share price.

Notably, options pricing suggests a post-earnings move of approximately 5.5% in either direction for contracts expiring shortly after the release. The expected move is slightly higher than the average 4.8% over the past four quarters.

Tesla’s Q1 Deliveries Fell Short

Ahead of the Q1 earnings, the EV giant missed the street’s forecast on deliveries. Tesla delivered 358,023 vehicles during the quarter, a 6.3% year-over-year (YoY) increase, but missed consensus estimates. While the growth rate remains positive, the miss signals a more challenging demand environment.

A key headwind has been the expiration of the $7,500 U.S. federal tax credit, which had previously acted as a meaningful demand catalyst. Elevated interest rates continue to weigh on affordability, particularly for big-ticket purchases such as vehicles. Competitive pressures are also intensifying, weighing on pricing and volumes.

Nonetheless, the high gasoline prices offer some respite to the EV makers. However, it is not likely to provide an immediate boost to quarterly deliveries.

Tesla Q1: Here’s What to Expect

Tesla will report its first-quarter earnings release with a mixed set of underlying drivers. Although the company’s Q1 delivery numbers fell short of analysts’ expectations, YoY increases in vehicle deliveries and average selling prices are likely to support revenue growth. Moreover, the contributions from the services segment should further drive its revenue.

However, a decline in regulatory credit revenue represents a notable headwind. At the same time, reduced energy storage deployments in Q1 may weaken momentum in a segment that is seen as a long-term growth pillar. These factors suggest that while revenue may grow, the pace of expansion could remain low.

On the profitability side, higher delivery volumes should provide some operating leverage, supporting margins. That said, external pressures, particularly tariffs, introduce cost uncertainty and could erode margin gains. The expected decline in regulatory credit revenue further complicates the earnings picture.

Analysts expect Tesla to report earnings of $0.21 per share, implying a 40% increase YoY. While this signals strong growth, Tesla has missed Street earnings expectations for four consecutive quarters.

Is TSLA Stock a Buy Ahead of Q1 Earnings?

Tesla continues to derive the bulk of its revenue and profitability from its EV segment. However, quarterly delivery fluctuations are no longer the primary drivers behind TSLA stock’s trajectory. The market is more focused on Tesla’s long-term growth drivers than on short-term automotive metrics.

Tesla’s investment case rests on emerging opportunities. The company’s energy storage systems, autonomous driving software, and humanoid robotics are seen as the primary catalysts. Each of these verticals has the potential to generate solid revenue and margins. Moreover, these segments could meaningfully diversify Tesla’s earnings base and support its share price.

As Tesla is in a transition phase, near-term risks include demand uncertainty and margin compression. Moreover, newer business lines remain early-stage and have yet to contribute materially to financial results. For investors with a long-term outlook, Tesla’s innovation pipeline may still justify a buy. However, in the short term, limited catalysts, soft EV demand, and an elevated valuation weaken the case for a bullish stance.

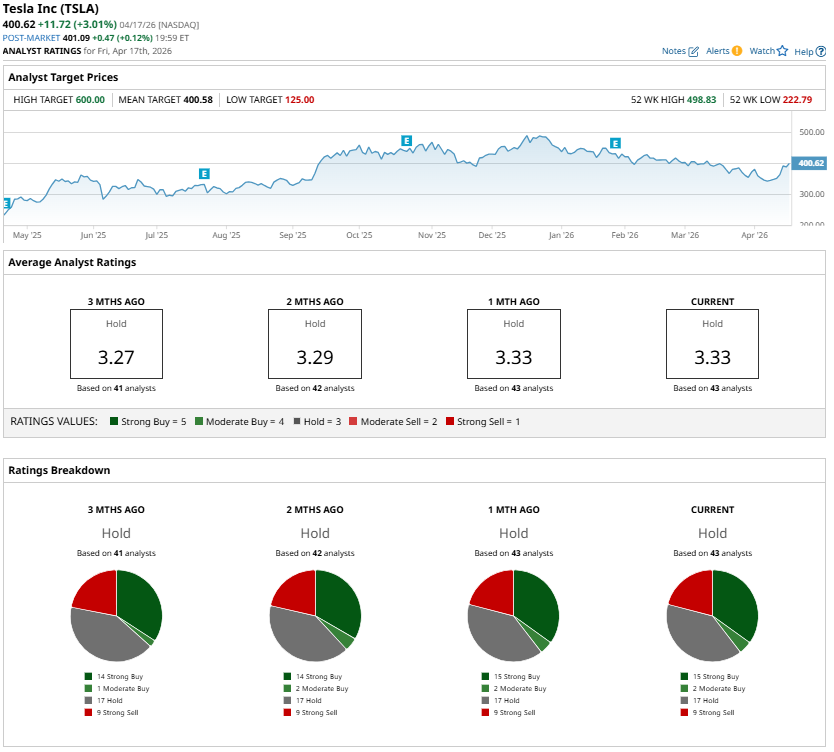

Analysts currently maintain a “Hold” consensus rating on TSLA stock heading into the first-quarter release.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tilray Stock Pops on New Trump-Driven Cannabis Hopes. Should You Chase the Rally?

- Tim Cook Is Stepping Down as Apple CEO, AAPL Stock Dips in After-Hours Trading

- Save This Psychedelic Stock Watchlist After Trump’s Latest Executive Order

- BlackBerry Stock Is Soaring on a New Nvidia Deal. Does That Make BB a Buy Here?