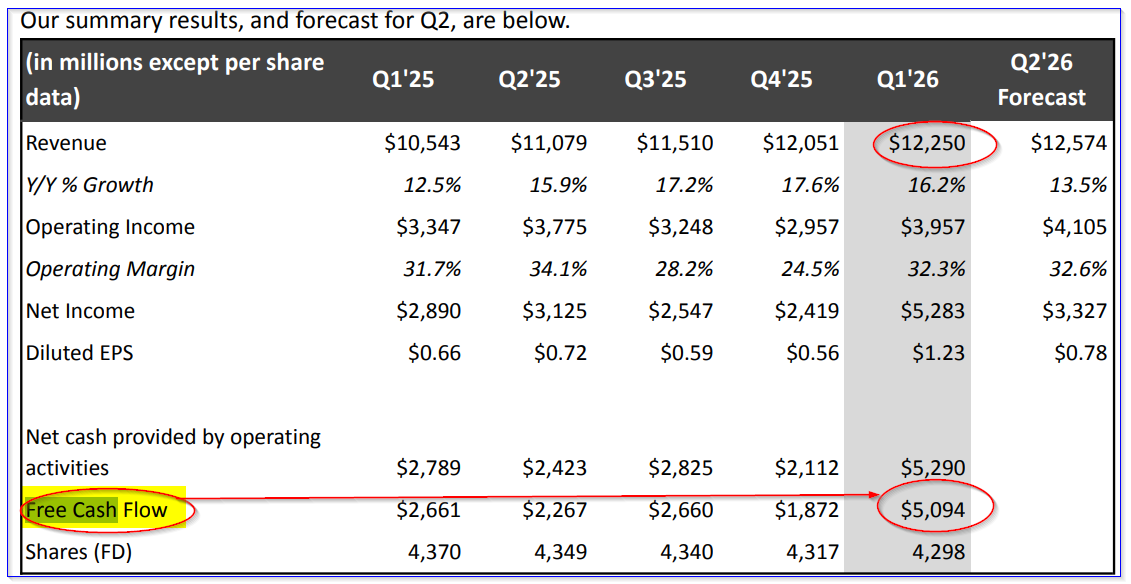

Netflix, Inc. (NFLX) generated $5.1 billion in free cash flow (FCF) in Q1, including a $2.8 billion deal termination fee. Adjusted FCF margins are still high, implying NFLX is worth $119, +22%. One attractive play is to short OTM puts.

NFLX closed at $97.31 on Friday, April 17, down 9.7% after releasing its Q1 results after the market close on April 16. This is still above a recent low of $75.86 on Feb. 12, right before the company walked away on Feb. 26 from its attempt to buy Warner Bros. Discovery (WBD).

Strong FCF and FCF Margin Results

Even after deducting the $2.8 billion cash termination fee, Netflix still generated $2.25 billion in operational free cash flow in Q1. That represented 18.4% of its revenue and was higher than the prior quarter's FCF of $2.11 billion (17.5% FCF margin).

Moreover, over the trailing 12 months (TTM), its adjusted FCF was over 19.4%. This can be seen from Stock Analysis data, which shows that its TTM revenue was $46.8 billion, and its TTM FCF was $1.894 billion:

$11.894b - $2.8 billion fee = $9.094 billion adj. TTM FCF

$9.094 b / $46.8 billion revenue = .1943 = 19.43%

That was only slightly down from its 20.94% FCF margin last quarter for all of 2025, as shown in Stock Analysis data.

Projecting Strong FCF

Moreover, management has guided that it expects to hit $12.5 billion in FCF for 2026, which equals $9.7 billion on an adjusted basis. It also forecasted revenue between $50.7 billion and $51.7 billion for 2026.

That works out to a projected adj. FCF margin for 2026 of 18.95% (i.e., $9.7/$51.2b avg revenue).

However, if Netflix can generate an average 20% margin over the next 12 months (NTM), and using analysts' revenue estimates, Netflix could generate much higher FCF:

0.20 x $52.41 billion (Stock Analysis revenue forecast) = $10.48 billion adj. FCF in 2026

0.20 x $58.56 billion = $11.71 billion adj. FCF 2027

Therefore, the NTM FCF forecast is $11.1 billion. That would be $1.64 billion more than the $9.46 billion Netflix generated in 2025. In other words, adj. FCF is set to rise +17.3% over the next year.

This could push NFLX stock's valuation much higher. Here's why.

Higher Price Targets for NFLX Stock

I discussed Netflix's valuation in a March 27 Barchart article, “Netflix Is Attractive to Value Buyers - Shorting Puts Can Set a Lower Buy-In Point.” For example, over the last 12 months, Netflix's $9.09 billion adj. FCF works out to 2.21% of its present market cap of $410.9 billion, taken from Yahoo! Finance calculations:

$9.09/ $410.9 billion = 0.0221 = 2.21%

That is the same as multiplying its adj. FCF by about 45x (i.e., 1/0.021 = 45.3x) . Therefore, using our NTM FCF multiple, Netflix could be worth over $500 billion, or +22% more :

$11.1 NTM FCF x 45 = $502.86 billion market cap

$502.86 b / $410.86 = 1.224 -1 = +22.4% upside

That implies the NFLX price target (PT) is worth over 22% more per share:

1.224 x $97.31 = $119.10 PT

That's higher than my prior $114.79 price target last month. Moreover, analysts have raised their price targets.

For example, Yahoo! Finance's survey PT is now $114.53, up from $113.21 three weeks ago, as I reported in my prior article. In addition, Barchart's mean analyst survey PT is now $115.63, up from $114.67, and AnaChart's average analyst price target is now $120.16, vs. $110.53 three weeks ago.

The bottom line is that Netflix is set to generate strong FCF over the next two years with higher revenue forecasts. That means NFLX stock is still deeply undervalued.

However, it could take a while to rise. One way to play NFLX to set a lower buy-in price while also generating yield income is to sell-short out-of-the-money (OTM) puts.

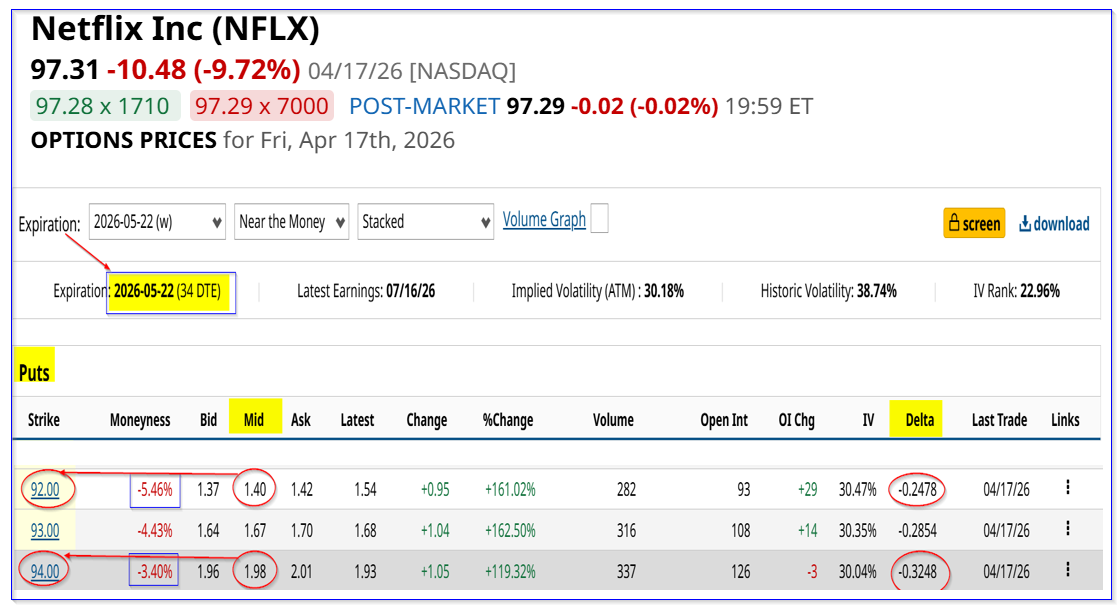

Shorting OTM NFLX Puts

I discussed this in my prior Barchart article at the end of March. I suggested shorting the $88.00 and $89.00 strike price puts expiring May 1, 35 days away. At the time, the premiums were $2.59 and $2.90, yielding 2.94% and 3.26% respectively (and 5% to 6% lower than the NFLX price, i.e., “out-of-the-money.”)

Today, those premiums have shrunk to just 18 cents and 23 cents, so this play has been very profitable. It makes sense to repeat this one-month away puts at OTM prices.

For example, the May 22 expiry period (34 days to expiry) has attractive short-put premiums at strike prices 3.4% to 5.4% lower than Friday's close.

For example, the $94.00 strike price (3.4% lower) has a midpoint premium of $1.98 for a 2.106% one-month yield (i.e., $1.98/$94.00), and the $92 strike price, 5.4% lower, has a 1.52% yield (i.e., $1.40/$92.00).

The bottom line is that investors can make an attractive income waiting to buy NFLX if it falls to these lower put option strike prices.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Netflix Generates Massive FCF and FCF Margins - NFLX Price Targets Are Higher

- Nike Stock Options Alert: LEAPS Buying Hints at a Bull Call Spread

- Microsoft Stock Could Be 25% Undervalued Based on Its FCF and Analysts' Estimates

- Unusual Options Activity Hints That a Big Fish Is Rolling Covered Calls on Shopify Stock