The EV market is getting tougher, and Chinese carmakers are a big reason why. In March 2026, China’s passenger car exports jumped 82.4% year-over-year (YOY) to about 748,000 vehicles, while new energy vehicle exports rose more than 140%.

At the same time, car sales inside China fell 19.2%, making it five straight months of yearly declines. That matters because Chinese brands are pushing harder into overseas markets just as demand at home weakens.

Tesla (TSLA) is right in the middle of that pressure. This January, Xiaomi’s YU7 SUV outsold Tesla’s Model Y by more than 2-to-1 in China, selling 37,869 units versus Tesla’s 16,845. Chinese EVs are also selling for as little as $10,000 to $20,000, and brands like BYD (BYDDF), Xiaomi (XIACF), and Geely (GELYF) are expanding into Europe, Latin America, Southeast Asia, and even parts of North America.

That helps explain why Tesla’s latest numbers landed badly. The company delivered 358,023 vehicles in Q1 2026, missing Wall Street estimates, and now looks headed for a third straight year of weaker delivery growth. Now, recent reports say Tesla is working on a smaller, cheaper electric SUV, about 14 feet long, with production expected to start in China before expanding to the U.S. and Europe. With TSLA still well below its December 2025 peak, will that lower-cost model be the real turning point, or just another headline? Let’s find out.

Tesla’s Financial Pulse

Tesla is no longer just a car company that makes EVs. It also earns money from battery storage and software, which are becoming more important parts of the business.

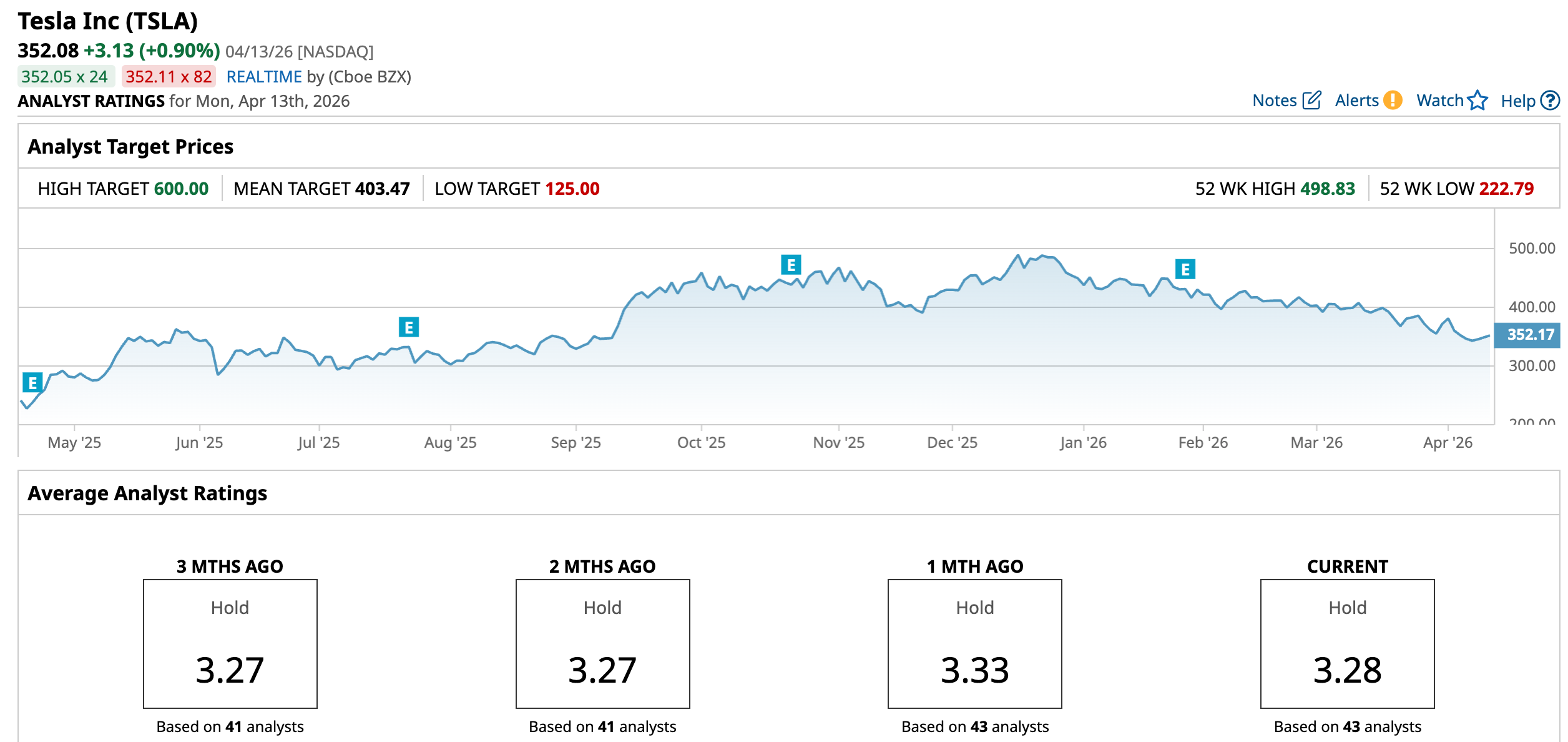

Over the past 52 weeks, TSLA is up about 40.15%, but it’s still down 21.37% so far this year.

Tesla trades at a forward P/E of 245.59 times versus about 15.37 times for the sector, so investors are clearly paying up for future growth, not current profits.

The latest numbers back that up. In Q4 2025, Tesla delivered 418,227 vehicles and pulled in $24.9 billion in revenue, both just under Wall Street estimates. Even so, it generated $1.41 billion in operating profit and non‑GAAP EPS of $0.50, beating forecasts and pointing to tighter cost control.

Automotive revenue reached $17.69 billion, while the energy business added $3.84 billion, showing real traction outside of cars. Gross margin improved to 20.1% from 16.3% a year earlier, a solid jump that shows those efficiency moves are starting to show up in the numbers.

What’s Driving Tesla’s Growth Story Now

Tesla is pushing growth from a few different angles. First, it plans to build a $4.3 billion battery plant in Lansing, Michigan, with LG Energy Solution. The factory is expected to start production in 2027 and will make battery cells for Tesla’s Megapack 3 systems, which utilities use to store power. Those cells will then be sent to Houston for Tesla’s energy storage business, showing the company wants a bigger role in the power market, not just in cars.

In addition, Tesla is trying to lock down more of its battery supply chain. Its new lithium refinery near Corpus Christi, Texas, is now up and running and turns spodumene ore into battery-grade lithium hydroxide. That gives Tesla more control over a key battery material, helps reduce dependence on China, and could lower costs over time.

Then there is the broader tech angle. Tesla’s $2 billion investment in xAI, which is now partly tied to SpaceX, shows it is thinking beyond vehicles. The company is already bringing Grok into its cars, with the idea that it could eventually help manage a large autonomous fleet. Add in the chip and infrastructure links with SpaceX, and Tesla is clearly building around energy, materials, and AI at the same time.

Wall Street’s Take: Is TSLA Still a Buy?

Analysts expect Tesla to earn $0.22 per share this quarter. That’s up from $0.15 a year ago, which is about 47% growth. The growth should keep going but slow down through 2026 and 2027. They’re looking for $0.31 in Q2 2026, up 15% from last year. For the full year 2026, it’s $1.40 versus $1.09 last year, that’s 28% growth. And 2027 is forecast at $1.95 compared to $1.40, or 39% growth.

On the bullish side, Wedbush analyst Dan Ives isn’t backing down. He called the Q1 deliveries underwhelming but said it wasn’t a surprise with the EV slowdown and Tesla’s bigger push into AI. He’s sticking with his $600 price target on TSLA, the highest on the Street, and still believes the cheaper next-gen EV and AI story is alive and well.

JPMorgan is on the opposite end. They kept their “Underweight” rating and $145 price target, which is roughly 60% below current levels. Analyst Ryan Brinkman says the 358,000 vehicles delivered in Q1 missed forecasts and will drag earnings lower. He already cut his Q1 EPS estimate to $0.30 from $0.43 and dropped the 2026 forecast to $1.80. He thinks the stock is betting on a demand rebound that won’t happen, especially with a record pile of unsold vehicles and 164,000 units sitting in inventory.

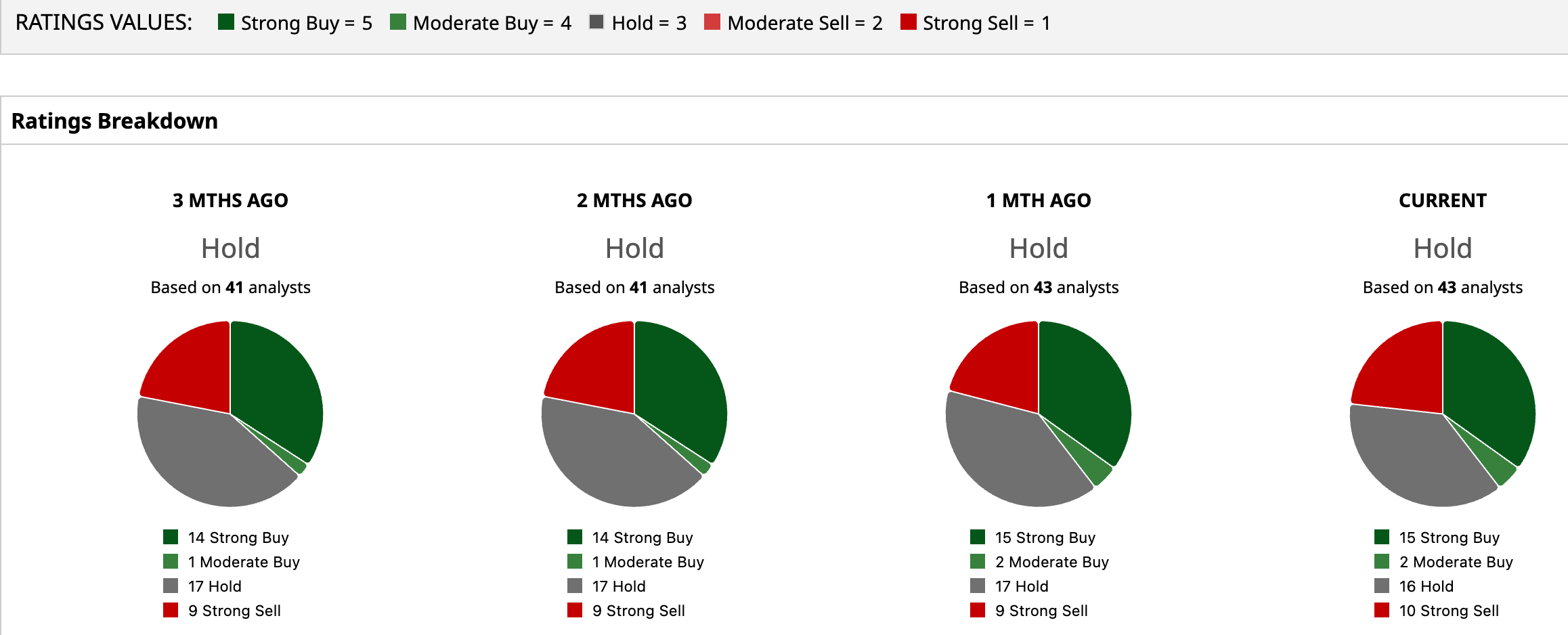

All 43 analysts covering the stock rate it a "Hold" on average. Their mean price target is $403.47, which only points to about 14.6% upside from here.

Conclusion

Put it all together, and TSLA doesn’t quite clear the bar for a clean “Buy” here. A cheaper SUV, deeper energy and AI optionality, and solid margin work all help, but they are colliding with weak deliveries, brutal Chinese competition, and a market that already values Tesla like a hyper‑growth story. With only mid‑teens upside to the Street’s target and a very split analyst tape, it looks more like a “Hold” for existing believers than a fresh entry point for new money. Over the next year, the path of least resistance is sideways‑to‑slightly‑higher trading rather than a sustained breakout.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart