Super Micro Computer (SMCI) builds the high-performance servers and infrastructure that sit at the heart of today’s artificial intelligence (AI) data centers (AIDC). And right now, speed matters across the industry. Customers increasingly prefer “Data Center Building Block” solutions because they allow faster deployment and quicker time to go live. These pre-designed, pre-validated infrastructure blocks also help lower costs through better workload optimization while minimizing power and water consumption.

That trend is exactly where Supermicro’s latest move fits in. At Mobile World Congress 2026, the company teamed up with SK Telecom (SKM) and Schneider Electric (SBGSF) (SBGSY) to push the next wave of AI data center builds. The trio plans to develop a pre-fabricated modular system that combines AI computing servers with the necessary power and cooling infrastructure into a single ready-to-deploy module. Instead of the traditional slow, step-by-step construction approach, these data centers can now be assembled like scalable building blocks.

SK Telecom will bring operational expertise, Super Micro will supply its high-performance GPU servers, and Schneider Electric will design the power and infrastructure backbone. With AI infrastructure demand exploding worldwide, this partnership could put Super Micro right in the middle of the next data center boom.

So, should investors buy SMCI stock now on this announcement?

About Super Micro Computer Stock

Founded in 1993 and headquartered in San Jose, California, Super Micro Computer is a powerhouse in server and storage solutions. Known for serving enterprise data centers and cloud giants, it has solidified its position as a key player in tech infrastructure. With a market cap of $19.6 billion, SMCI continues to innovate in the ever-evolving data and AI landscape.

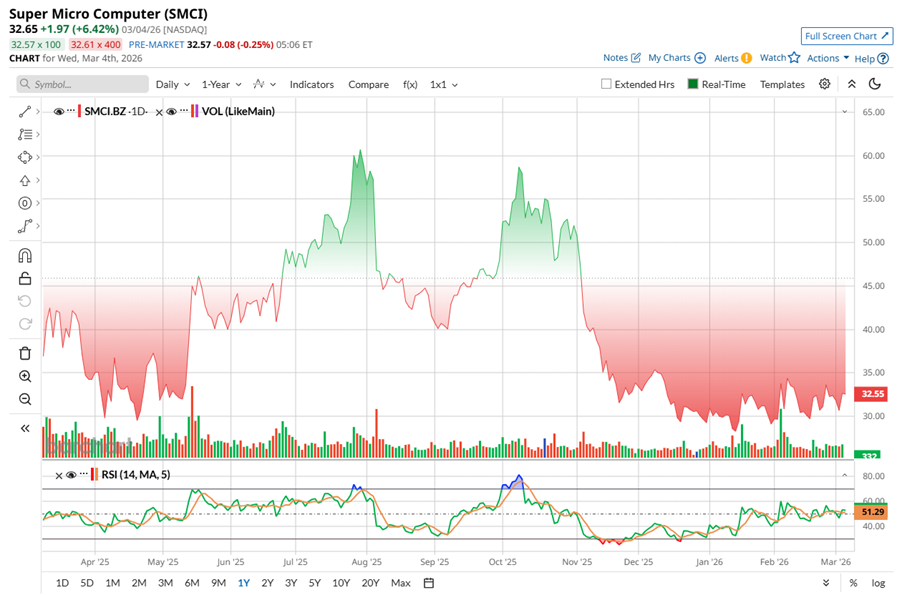

Shares of Super Micro Computer enjoyed a powerful rally last year as investors rushed to gain exposure to the booming AI server market. However, the momentum slowed after the company released its fiscal Q1 2026 results in early November. The report highlighted a clear trade-off between growth and profitability, which made investors cautious. The reaction was swift, and the stock slipped into the red through the final two months of 2025.

SMCI is down about 16.6% over the past 52 weeks and nearly 20% over the last six months. In fact, the stock has almost halved from its July peak of $62.36.

The tone entering 2026 is still cautious, though slightly improved. SMCI stock rose 10.9% year-to-date (YTD). Plus, following its strong Q2 report, the stock rose by mid-teens percentage.

Technically, trading activity hints at stabilizing sentiment. Volume has recently leaned toward the green side, suggesting renewed buying interest. Meanwhile, the 14-day RSI, which had slipped into oversold territory in November, has climbed back toward neutral levels and now sits at 52.67, indicating the stock may be slowly regaining balance rather than remaining under heavy selling pressure.

SMCI is not just riding positive business momentum, but its valuation is quietly turning heads, too. When CEO Charles Liang and CFO David Weigand bought shares in February, it signaled confidence from the inside. That kind of move usually speaks louder than headlines.

SMCI is priced at 14.59 times forward adjusted earnings and 0.47 times forward sales. It is trading cheaper than sector averages and its historical medians, and that’s pretty modest for a company deeply plugged into the AI infrastructure boom. For a business powering next-gen data centers, the stock looks less like hype and more like a value play hiding in plain sight.

Super Micro Surges on Q2 Beats

Super Micro Computer released its second-quarter report of fiscal 2026 on Feb. 3, which felt like a turning point. After a few quarters where growth had started to cool, investors were waiting for proof that the AI story still had legs. The numbers impressed investors, and the stock jumped nearly 14% in the next trading session as confidence returned.

The company raked in $12.68 billion in revenue, up by an impressive 123.4% year-over-year (YOY) and 153% from the prior quarter. It easily cleared Wall Street’s expectations and even beat management’s own guidance range of $10 billion to $11 billion. Non-GAAP EPS rose to $0.69 from $0.59 last year, again topping estimates.

Now, part of that surge was timing. About $1.5 billion in shipments were pushed from Q1 into Q2 due to customer readiness issues. But even adjusting for that, demand looks real and broad-based. The biggest driver continues to be the rapid ramp of Rack Scale AI systems, as companies race to build out AI infrastructure despite ongoing supply chain constraints.

The customer base tells the same story. Large global data center operators and enterprise buyers remain the core engines. AI GPU platforms accounted for the majority of Q2 revenue, highlighting how central they have become to the mix. Enterprise/channel revenue hit $2 billion, up 42% YOY and 29% sequentially. Meanwhile, the OEM appliance and large data center segment generated $10.7 billion (about 84% of total revenue), and grew 151% annually, more than tripling from the previous quarter.

Looking ahead, management expects the momentum to carry into Q3, guiding for at least $12.3 billion in sales and around $0.60 in non-GAAP EPS. If delivered, that would mean another triple-digit growth quarter and keep the AI narrative firmly intact.

Meanwhile, analysts tracking SMCI project its Q3 revenue to be around $12.5 billion, while profit is expected to be $0.54 per share. For fiscal 2026, EPS is expected to rise 4.7% YOY to $1.80, and then surge by 43.9% annually to $2.59 in fiscal 2027.

What Do Analysts Expect for Super Micro Stock?

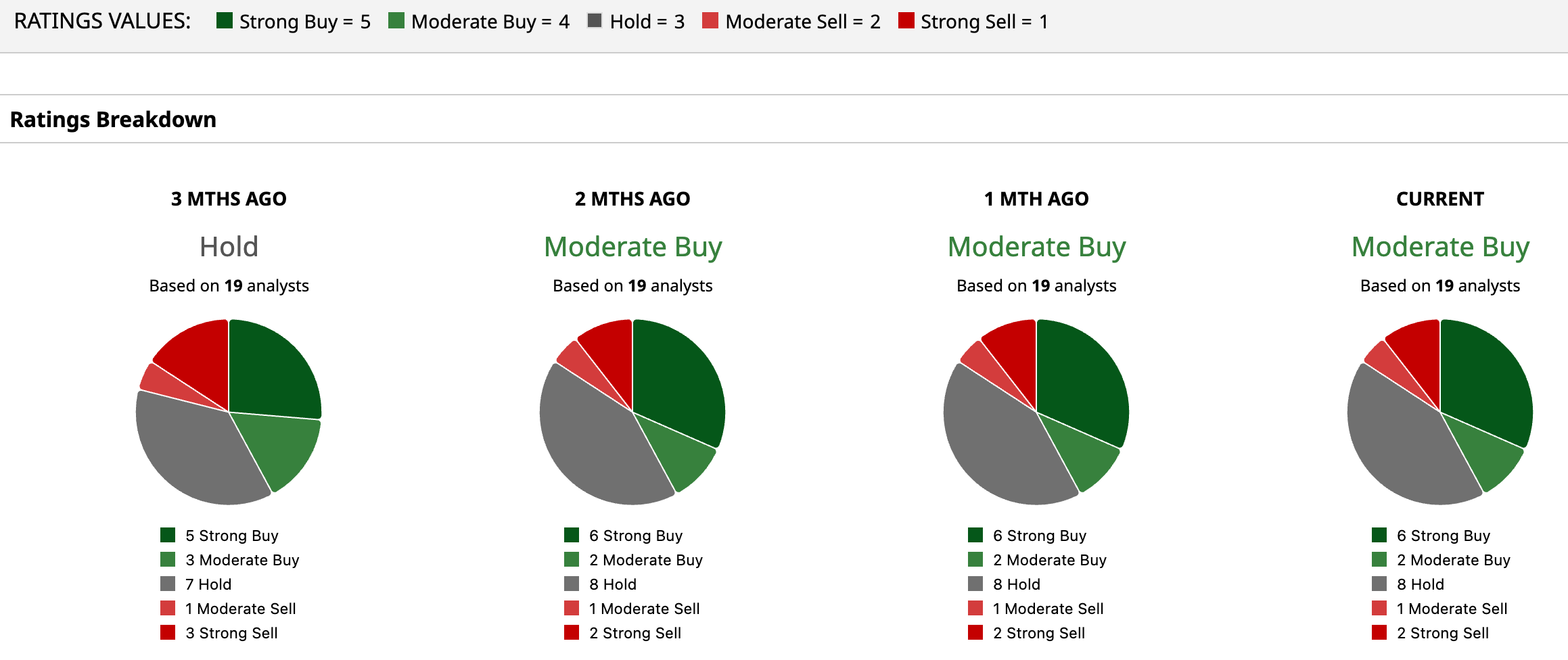

Overall, SMCI has a consensus rating of “Moderate Buy,” upgraded from the “Hold” rating three months ago. Out of 19 analysts, six advise a “Strong Buy,” two suggest a “Moderate Buy,” eight analysts are playing it safe with a “Hold,” one has a “Moderate Sell,” and the remaining two analysts are outright skeptical, recommending a “Strong Sell.”

The mean price target of $42.76 implies that SMCI has upside potential of 34.7% from the current price levels. The Street-high target of $64 suggest the stock could rally as much as 101.6%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart