Prediction markets are stuck in a serious regulatory fight. In February, President Donald Trump's administration threw its weight behind Kalshi and Polymarket in a key court battle with states trying to shut these platforms down, with U.S. Commodities and Futures Trading Commission (CFTC) Chairman Michael Selig saying, “We will see you in court.” The numbers show why this fight matters; about 90% of Kalshi’s trading volume now comes from sports bets, and Kalshi alone handled more than $1 billion in volume on this year’s Super Bowl.

Just last week, Utah moved to enact legislation to clamp down on prediction markets, putting it directly at odds with both the federal push and the industry. Kalshi and Polymarket are now valued around $20 billion each after their latest funding rounds. In other words, this fight will help decide who gets to handle the next big wave of sports-betting activity — and the rich data business that comes with it.

Now, Palantir Technologies (PLTR) is stepping into the mix. On March 10, Polymarket announced a partnership with Palantir and TWG AI to build a "next-generation sports integrity platform" powered by the Vergence AI engine, a joint venture between Palantir and TWG AI that will monitor trades, flag suspicious activity, and screen banned bettors in real time. That fits what Palantir already does as a core data provider for defense agencies and large corporations that need tight controls and clean data in sensitive environments — and it turns PLTR stock into a direct way to play the tug-of-war around the next generation of sports betting.

So, does Palantir's new sports-betting angle add a real growth catalyst to an already explosive business? Let's find out.

What Do Palantir’s Latest Numbers Say?

At its core, Palantir is a software company that sells data analytics and AI platforms to governments and large businesses, helping them make decisions from messy, real-world data. PLTR stock has already had a big move — up 90% over the past 52 weeks even after dropping 15% year-to-date (YTD) — suggesting that investors are still adjusting after a sharp re-rating.

PLTR stock also trades at a forward price-to-earnings (P/E) ratio of 148.6 times versus 21.5 times for the sector. As such, the valuation still asks for near-perfect execution.

In the fourth quarter of 2025, revenue jumped 70% year-over-year (YOY) and 19% quarter-over-quarter to $1.407 billion, led by 93% YOY U.S. revenue growth to $1.076 billion. U.S. commercial revenue surged 137% to $507 million while U.S. government revenue grew 66% to $570 million. The company closed 180 deals worth at least $1 million during the period, 84 deals worth at least $5 million, and 61 worth at least $10 million. Total contract value hit a record $4.262 billion, up 138% YOY.

Customer count rose 34% YOY, GAAP operating margin reached 41%, and adjusted operating margin was 57%. GAAP net income came in at $609 million, while adjusted free cash flow was $791 million. Cash, cash equivalents, and short-term U.S. Treasury securities stood at $7.2 billion.

For the full year, revenue rose 56% to $4.475 billion. GAAP net income reached $1.625 billion, operating income totaled $1.414 billion, and adjusted free cash flow was $2.27 billion, showing Palantir is not just a growth story but also increasingly profitable.

Palantir’s Next Leg of Growth

Palantir’s recent LG CNS partnership builds on a late-2025 rollout inside an LG affiliate that improved quality management, and is now being scaled across LG Group as a full AI transformation project. Palantir and LG CNS are also setting up a dedicated Forward Deployed Engineering team to find and deliver high-value use cases in manufacturing, energy, electronics, logistics, and other areas, which effectively opens a door into one of the world’s largest industrial networks.

The Rackspace (RXT) partnership tackles a different problem — moving Palantir’s Foundry and AIP from trial runs into live, day-to-day use. Rackspace is handling operations, data migration, hosting, security, and compliance so enterprises can get Palantir-based AI into production in weeks or months instead of months or years. That is especially important in regulated sectors, where data rules and controls often slow things down. The push is backed by Rackspace’s Private Cloud and U.K. Sovereign data centers, with 30 Palantir-trained engineers already on board, and a plan to grow that team to more than 250 within a year.

Then there is Airbus (EADSY). Palantir recently extended an Airbus partnership that has already been in place for more than a decade through a new multi-year deal around the Skywise platform. Skywise helps with aircraft design, production efficiency, safety, sustainability, supply-chain management, and airline operations, with more than 50,000 users working with Skywise daily. This kind of partnership renewal matters because it shows Palantir is not just winning new customers, but keeping large clients tied into core systems for long periods.

Wall Street’s Odds on Palantir

Palantir’s next earnings release is set for May 4. Analysts expect EPS of $0.22 for the March quarter and $0.24 for the June quarter, compared with $0.04 and $0.13 respectively in the prior-year periods. For full-year fiscal 2026, the Street is looking for EPS of $1.02, followed by $1.52 in fiscal 2027. That works out to estimated YOY growth of 62% and 49%, respectively.

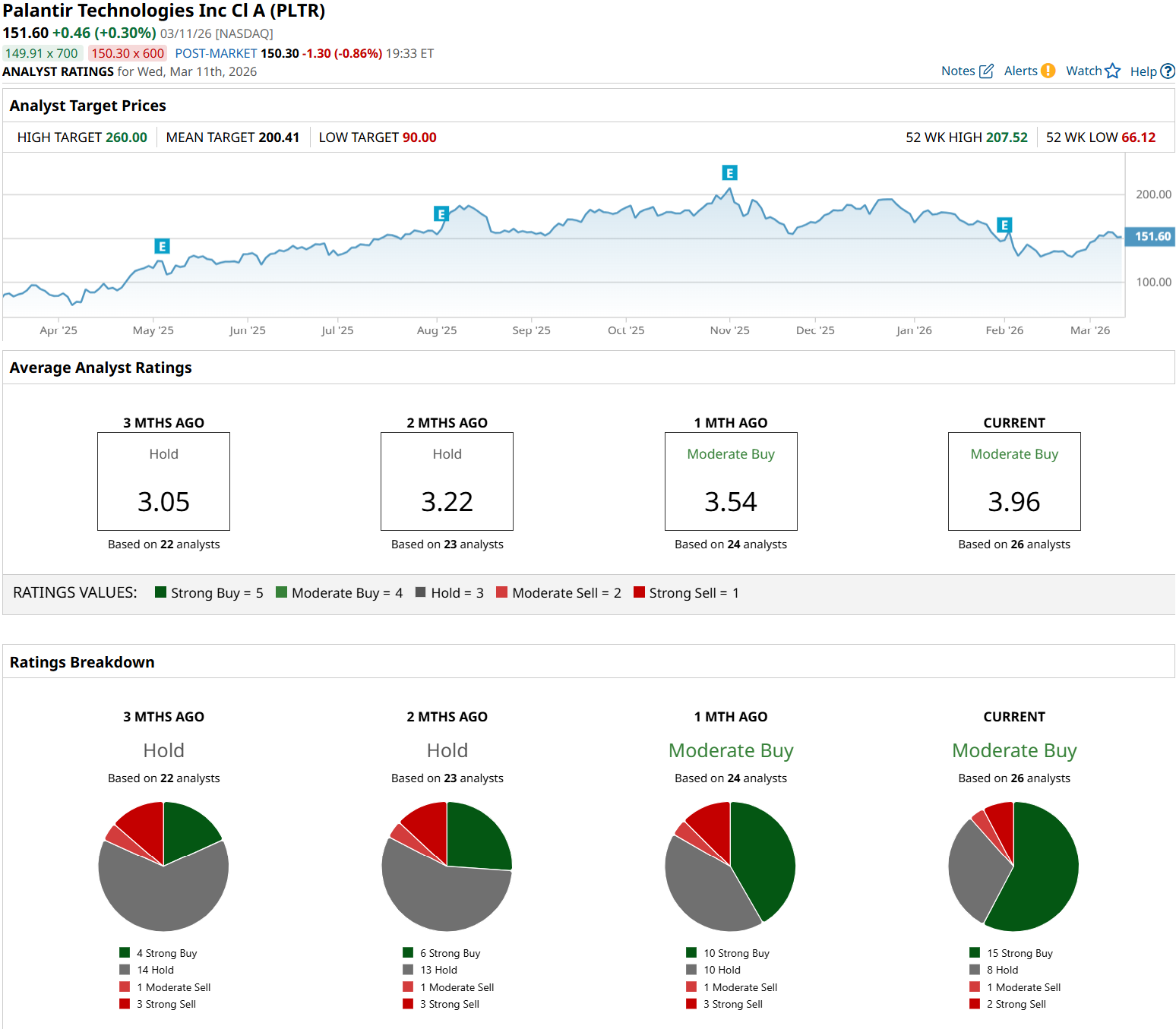

That helps explain why Bank of America remains firmly positive on PLTR stock. The firm reiterated a “Buy” rating and set a $255 price target, arguing that Palantir still has “material further upside” as new use cases scale and margins continue to improve.

Across the Street, the tone is similar. Based on 26 analysts surveyed, the stock has a consensus “Moderate Buy” rating. The average target of $200.41 points to roughly 33% potential upside from current levels.

Conclusion

At this point, PLTR stock looks less like a pure sports-betting play and more like a hyper-expensive AI infrastructure stock that just picked up an intriguing new vertical in prediction markets. The Polymarket deal reinforces the core thesis that Palantir’s software wins in high-stakes, high-scrutiny environments, but it is not big enough yet to move the financial needle on its own.

With Palantir stock up hard over the past year, trading at nosebleed multiples, and the Street already baking in aggressive earnings growth, the risk‑reward here leans more toward “hold if you own it and nibble on pullbacks” than “back up the truck.” Over the next 12 to 18 months, the most likely path is higher, but with plenty of volatility and very little room for execution errors.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Walmart v.s Costco: Which Is the Better Dividend Stock in 2026?

- Is Carvana Stock a Buy on New Stock Split Announcement?

- Palantir Is Now a Sports Betting Stock. Does That Make PLTR a Buy Here?

- Tesla’s China-Made EV Sales Just Nearly Doubled. Should You Buy TSLA Stock Now in Hopes of an Auto Business Rebound?