February has been a strong month for Dividend Kings, with several companies once again showing they are serious about paying shareholders through higher dividends. Walmart (WMT) remains a top-rated pick for 2026, continuing to stand out among dividend-paying stocks. The backdrop is supportive as well, with the retail sector holding up and consumer spending driving 4.4% economic growth in the third quarter — the fastest pace in two years despite ongoing inflation worries.

On Feb. 18, Walmart's board approved an annual dividend of $0.99 per share for fiscal 2027, a 5% increase from the prior year's $0.94, marking the company's 53rd consecutive year of dividend increases. That keeps Walmart firmly in Dividend King territory, a title reserved for companies with at least 50-straight years of payout growth. The decision followed a solid update, as Walmart reported Q4 fiscal 2026 revenue of $190.7 billion, up 5.6% year-over-year (YOY), with global e-commerce revenue growing 24%.

But with WMT stock already up 13% year-to-date (YTD) — even after a small pullback on softer forward guidance — and options data pointing to a potential move toward $139 by mid-May, does this 5% dividend bump make WMT a compelling buy right now? Or has the rally already priced in the good news? Let’s take a closer look.

Do Walmart’s Numbers Justify a Higher Dividend?

Valued at $980.2 billion by market capitalization, Walmart is the world’s largest retailer, running a global network of supercenters, discount stores, Sam’s Club warehouses and a fast-growing e‑commerce platform that makes money from both first‑party and marketplace sales. Over the past 52 weeks, WMT stock has climbed about 32%, with roughly 13% of that gain coming in 2026.

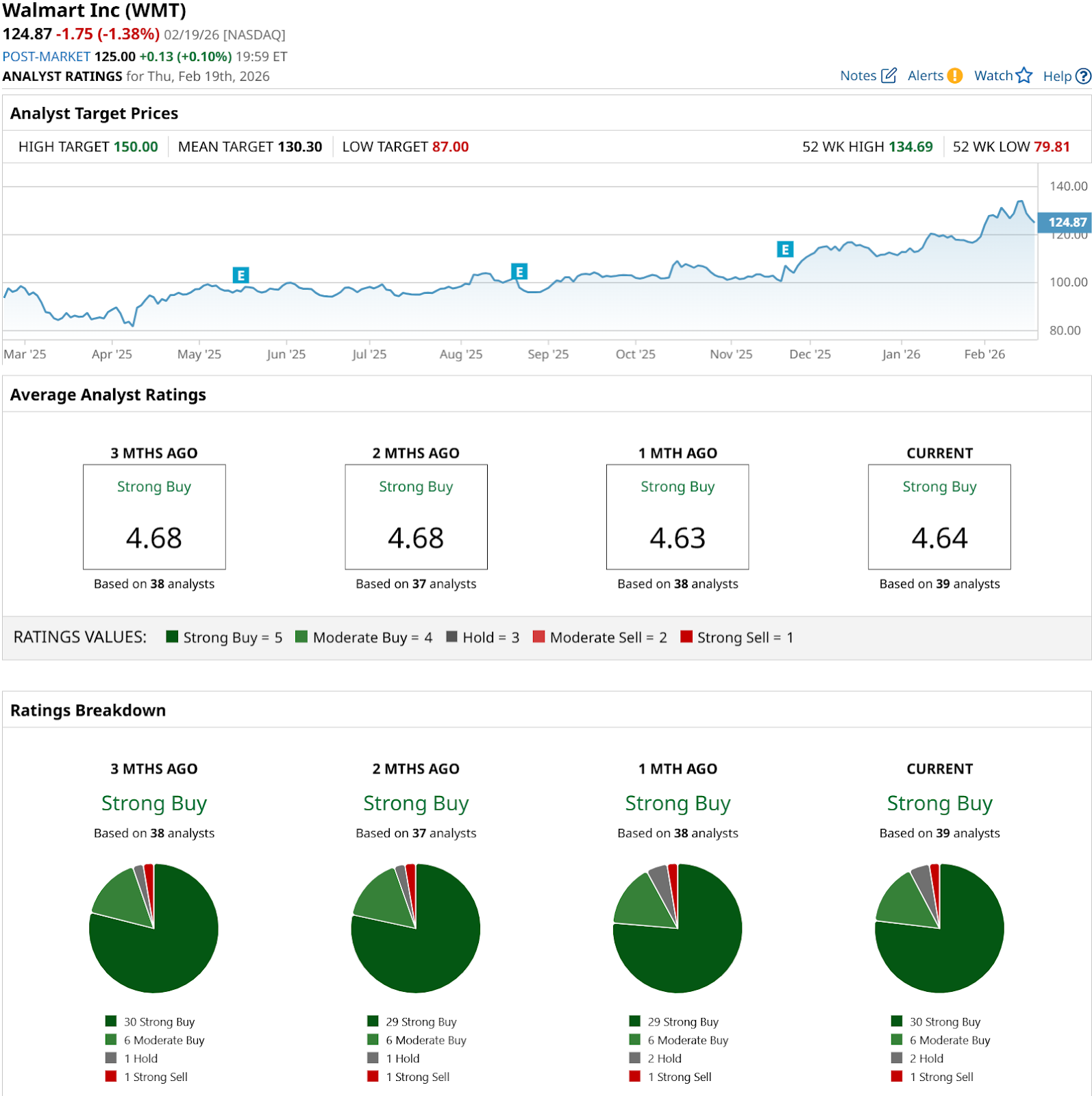

What's more, the forward price‑to‑earnings (P/E) ratio of 43.85 times — versus a P/E of about 16.7 times for the broader consumer staples sector — shows that investors are paying a clear premium for Walmart’s stability and growth profile.

On the income side, Walmart just raised its annual dividend roughly 5% to $0.99 per share, extending a 53‑year streak of increases and keeping its payout ratio at a conservative 35.43%. WMT shares yield about 0.75% on an annual dividend of roughly $0.2475 per quarter. That's well below the consumer staples sector average near 2%, so this is clearly a dividend‑growth story and not a high‑yield one.

In Q4 fiscal 2026 (Q4 calendar-year 2025), Walmart delivered $190.7 billion in revenue, up 5.6% YOY and essentially in line with expectations, while adjusted EPS of $0.74 and adjusted EBITDA of $12.45 billion modestly beat estimates. Operating margin held at 4.6%, free cash flow margin was a steady 3.2%, and same‑store sales rose 4.6% YOY, highlighting a business that is steadily delivering reliable, high‑volume growth at scale.

The Structural Growth Engines Powering Walmart

Walmart’s growth story is increasingly tied to AI-driven shopping. The October 2025 partnership with OpenAI plugs Walmart directly into ChatGPT, allowing customers to chat, get suggestions, and check out in one flow, turning product search into a simple conversation instead of a long search-and-filter process. Walmart's own Sparky shopping agent builds on that by learning customer preferences and tailoring recommendations at scale, helping lift digital engagement, conversion, and basket size.

At the same time, Walmart Marketplace is moving into higher-end territory with its Premium Musical Instrument Shop, a curated online store featuring brands like Fender, Boss, Zildjian, Ernie Ball, Roland, and more. This expansion into professional-grade gear adds more specialized, higher-ticket products while still leaning on Walmart’s convenience and trusted platform to attract both creators and everyday shoppers.

A third growth driver is the deepening AI collaboration with Alphabet's (GOOGL) Google. By feeding Walmart and Sam’s Club inventory into Gemini through the Universal Commerce Protocol, customers can find relevant products directly inside AI-led conversations, receive personalized bundles based on linked accounts and past purchases, and get fast delivery on locally curated items, tightening the link between discovery, intent, and purchase.

What Wall Street Sees Next for WMT Stock

Consensus is calling for Q1 fiscal 2027 EPS of $0.65 versus $0.61 a year ago, implying 7% YOY growth. For the full fiscal year, analysts expect $2.86 in EPS, up 8% YOY from $2.64. That outlook sits next to management’s own guidance, which pegs Q1 revenue at about $164 billion and EPS at $0.61. Management's adjusted EPS guidance for the full fiscal year comes in at $2.64.

Tigress Financial recently raised its price target on Walmart to $135 while reiterating a “Buy” rating, highlighting strong digital growth, solid execution, and a growing mix of higher‑margin businesses — especially advertising, fulfillment, and membership — as key drivers of future returns. JPMorgan analyst Christopher Horvers, who keeps an “Overweight” rating with a $137 target, noted that WMT stock has already run and that earnings may give shares a pause. Still, the analyst laid out a bull case for a 6% enterprise margin and $4 in EPS over the next two to three years, built on further margin expansion and the same higher‑margin growth areas.

Stepping back, 39 analysts tracked by Barchart have a “Strong Buy” consensus rating on WMT stock. The average price target of $130.55 implies roughly 4% potential upside from current levels.

Conclusion

All told, Walmart's recent dividend hike strengthens an already solid case for owning WMT stock, but it does not magically turn the stock into a bargain. Investors are paying a premium multiple for dependable mid‑single‑digit growth, world‑class scale and some genuinely interesting AI‑driven optionality, not for a fat yield. For long‑term, conservative investors who want a durable compounder with a rising payout, WMT still looks buyable on pullbacks rather than screamingly cheap at today’s levels. Over the next year or so, the path of least resistance is probably modestly higher, tracking earnings growth and dividend increases more than multiple expansion.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart